Muzinich Weekly Market Comment: Bittersweet

Insight

June 1, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

May delivered strong returns and a renewed appetite for risk, but beneath the optimism lies an increasingly complex reality. While hopes of a US-Iran agreement have eased pressure on energy markets, investors and policymakers must now grapple with the prospect that higher energy prices and tighter supply conditions may prove more persistent than previously assumed.

May delivered more than many had hoped. For the vast majority of investors, net asset values rose in May, sending a quiet wave of confidence into the summer months. This was further demonstrated by our preferred index for market sentiment, the VIX, which closed the month with a 15 handle, suggesting confidence has returned, and investors are comfortable adding risk and reducing cash.

The dominant macro thread running throughout May was the back-and-forth of negotiations between the US and Iran, with a deal appearing tantalizingly close as the month drew to a close. The agreement on the table is a 60-day memorandum of understanding to extend the ceasefire and reopen the Strait of Hormuz (SoH) to unrestricted shipping, which sits on President Trump's desk pending approval at month-end.1

For investors and central banks alike, this is bittersweet news. The reopening of the SoH is a much-needed relief valve for energy markets that have absorbed a severe supply shock. Estimates suggest the global oil market has been running a deficit of approximately 7.5 million barrels per day since March 1st, contributing to a drag on growth while adding an unwelcome upward push to inflation worldwide.2

Yet there is a sour note in the fine print. Where initial speculation had pointed to a 6-month deal, what is currently on the table is just 60 days. US Treasury Secretary Bessent has been clear about the Administration's position: any long-term agreement requires Iran to open the SoH toll-free, surrender its enriched uranium, and end its nuclear programme.1 Optimists will argue that negotiations are closer to achieving those objectives than many believe, and that 60 days is all that is needed. However, the more cautious view is that this window is almost certainly too short to strike a longer-term deal, to restore regional production to full capacity and rebuild inventories. Clearing mines from the Strait, restarting shut-in wells, and repairing structural damage are all processes that will most likely take considerable time.

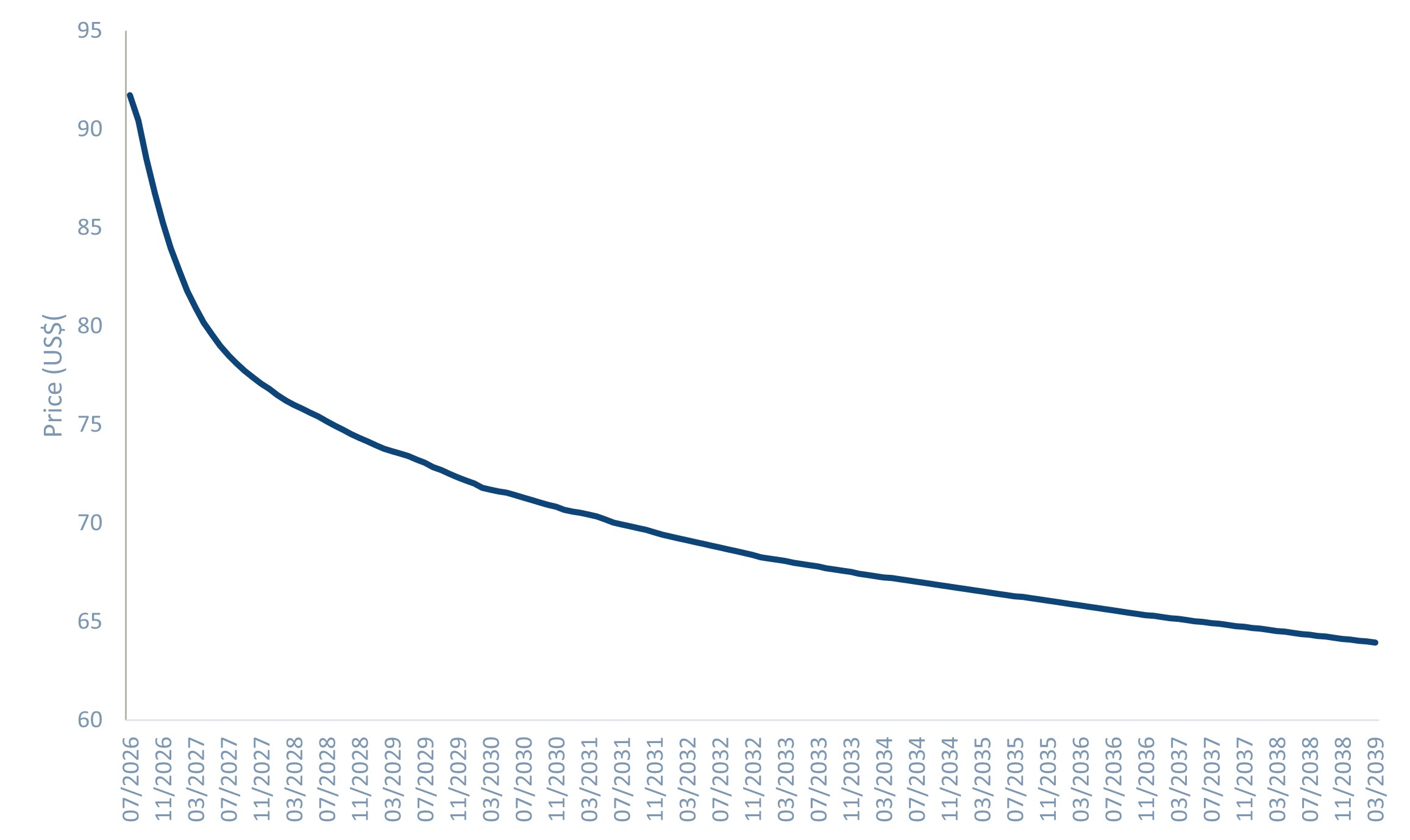

Oil markets share this concern. Although the asset class was the clear underperformer in May – with Brent falling to the low US$90s per barrel, a decline of nearly 20% - the broader pricing structure still reflects a tight supply market. The consensus median forecast for Brent at year-end sits at US$84.50, roughly US$1 below the forward curve,3 and while the oil curve remains in backwardation, Brent does not appear to dip below US$70 until 2031 (see Chart of the Week I).

This leaves central banks and governments facing an increasingly uncomfortable question. Are energy prices still best understood as transitory, or are elevated levels a more persistent feature of the macro landscape? And if the latter is true, what constitutes the appropriate policy mix to achieve inflation and growth objectives in a world where these energy supply shocks have become more structural?

The answer is already taking shape, with two clear adjustments in motion since the start of March. The first is the need for a higher neutral level of policy rates across the globe. For the Bank of Japan (BoJ), which is mid-tightening cycle, little has fundamentally changed, though the energy shock may push the committee to move faster. For the European Central Bank (ECB), which normalized earliest among the major central banks, there is ground to cover. The overnight interest rate swap market prices in two 25 basis points (bps) hikes this year, with a 93% probability that the first lands in June.4 ECB Chief Economist Philip Lane validated the market’s view this week, saying there was no need to correct markets from anticipating a rate hike next month.5

The UK Monetary Policy Committee (MPC) and the US Federal Open Market Committee (FOMC) face less urgent but still real adjustments, as they lagged the ECB, leaving policy rates modestly above neutral; markets priced in one 25bps MPC hike in 2026 to reach neutral, while the FOMC will also need to tighten policy by 25bps to achieve neutrality by the first quarter of 2027.3

The second adjustment unfolding is at the long end of government bond curves, which is caught between two powerful forces of structurally higher inflation expectations pushing yields up, and the near-certain rise in fiscal spending as governments step in to shield households and businesses from the cost-of-living squeeze, even as high energy prices slow growth and erode tax revenues.

Putting the puzzle pieces together, government bond market price action looks rational. The US, German and UK curves have all bear-flattened, reflecting the dual adjustment to higher neutral rates and rising fiscal pressures. Japan stands apart, with its curve bear-steepening as bond vigilantes send a clear signal to the BoJ not to drag its feet on the policy adjustment process.

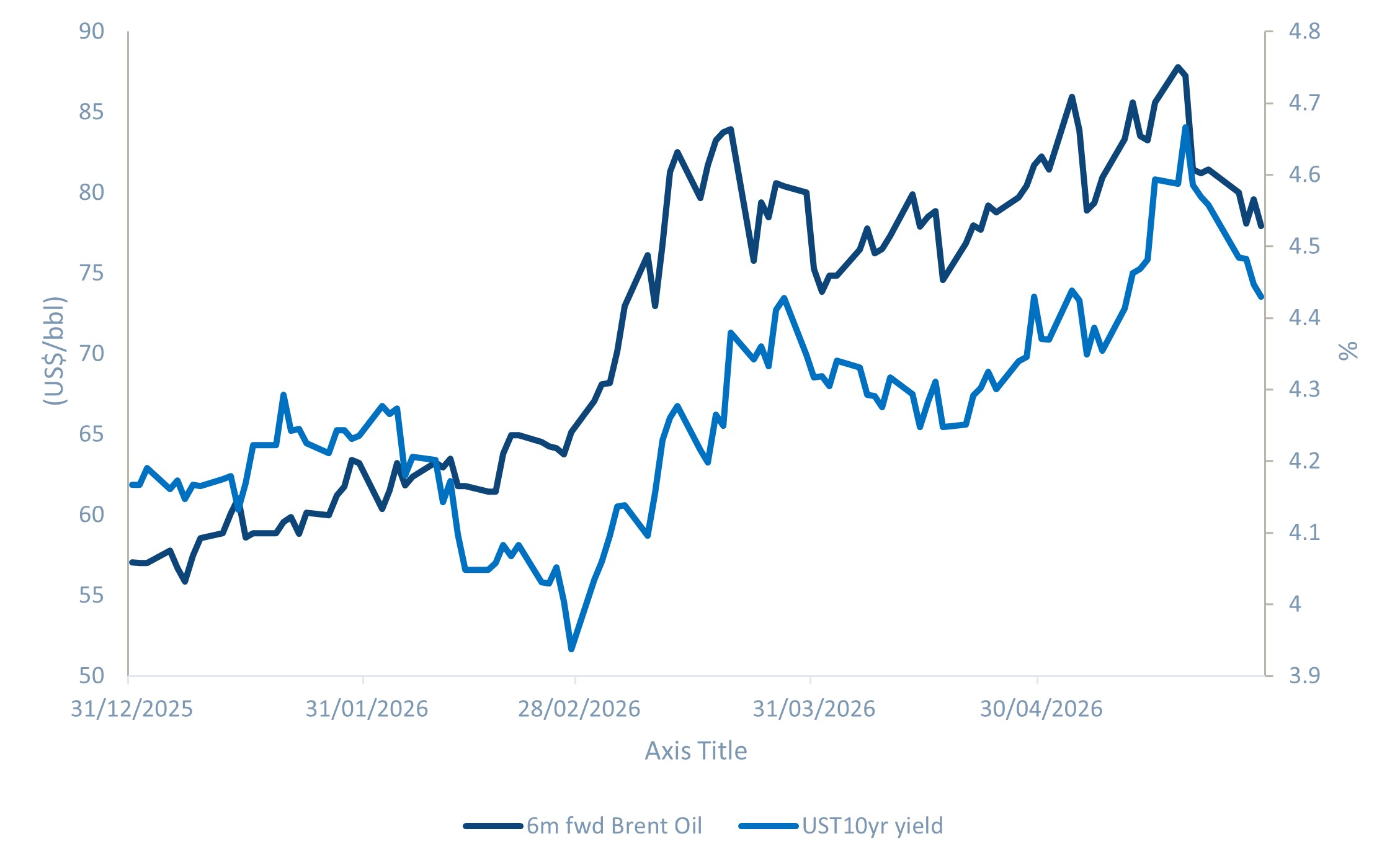

Looking ahead to the rest of 2026, the supply and demand imbalance in energy markets and the evolving path of oil prices are likely to play a dominant role in shaping government yields (see Chart of the Week II). Investors can also take some comfort in the fact that – unlike in 2022 – central banks have not been caught flat-footed with ultra-accommodative policy rates. However, government balance sheets may face greater scrutiny this time around, as there is significantly less room to raise spending or expand fiscal deficits while keeping indebtedness on a sustainable path over the medium term.

Chart of the Week I: Structurally higher energy prices – Brent above 70 until 2031?

Source: Bloomberg as of May 29, 2026. For illustrative purposes only.

Chart of the Week II: Is the Future Direction of UST10 Dependent on Oil?

Source: Bloomberg as of May 29, 2026. For illustrative purposes only.

Source: Bloomberg as of May 29, 2026. For illustrative purposes only.

All sources are Bloomberg unless otherwise stated.

Past performance is not a reliable indicator of current or future results.

References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

References

1. Bloomberg, “Trump Says ‘Final Determination’ on Iran Truce Is Coming Soon,” May 29, 2026

2. Goldman Sachs Research, “Oil Tracker: Visible Stock Draws Accelerate on Lower Exports; Weakening China Imports and

Demand,” May 20, 2026

3. Bloomberg, as of May 29, 2026

4. Bloomberg, as of May 29. 2026

5. Bloomberg, "ECB Set to Lift Its Inflation Outlook in June, Lane Tells Nikkei," May 26, 2026

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of May 29, 2026, and may change without notice. All data figures are from Bloomberg, as of May 29, 2026, unless otherwise stated.

--------

Important information

Muzinich & Co., “Muzinich” and/or the “Firm” referenced herein is defined as Muzinich & Co. Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Any forward-looking information or statements expressed in the above may prove to be incorrect. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Muzinich gives no undertaking that it shall update any of the information, data and opinions contained in the above.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

In the United Arab Emirates (UAE) (excluding the Dubai International Financial Centre (DIFC) and the Abu Dhabi Global Market (ADGM): This document, and the information contained herein, does not constitute, and is not intended to constitute, a public offer of securities in the United Arab Emirates (“UAE”) and accordingly should not be construed as such. The Units are only being offered to a limited number of exempt Professional Investors in the UAE who fall under one of the following categories: federal or local governments, government institutions and agencies, or companies wholly owned by any of them. The Units have not been approved by or licensed or registered with the UAE Central Bank, the SCA, the Dubai Financial Services Authority, the Financial Services Regulatory Authority or any other relevant licensing authorities or governmental agencies in the UAE (the “Authorities”). The Authorities assume no liability for any investment that the named addressee makes as a Professional Investor. The document is for the use of the named addressee only and should not be given or shown to any other person (other than employees, agents or consultants in connection with the addressee’s consideration thereof).

In the United Arab Emirates (UAE) (including the Dubai International Financial Centre and the Abu Dhabi Global Market): This information does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe for or purchase, any securities or investment products in the UAE and accordingly should not be construed as such. Furthermore, this information is being made available on the basis that the recipient is an entity fully regulated by the ADGM Financial Services Regulatory Authority (FSRA), and acknowledges and understands that the entities and securities to which it may relate have not been approved, licensed by or registered with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority, the Financial Services Regulatory Authority or any other relevant licensing authority or governmental agency in the UAE. The content of this report has not been approved by or filed with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority or the Financial Services Regulatory Authority.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-06-01-18591

By clicking "Submit", I am (i) signing up to receive the Opinion Pieces from the "Opinions" page of the Muzinich & Co website, (ii) representing that the above information is true and accurate and (iii) agreeing to join the Muzinich & Co mailing list. I understand that Muzinich & Co will not add retail investors or individuals with personal email addresses to its mailing list and represent that I am not a retail investor. By providing my personal and professional information I am consenting to its use and disclosure in accordance with the Muzinich & Co. Privacy Policy. I understand that I may withdraw my consent and unsubscribe from receiving future communications by clicking "Unsubscribe" from the emails that are sent to me from Muzinich & Co.