The evolution of private credit: Understanding direct and parallel lending

Insight

June 4, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

Private credit is no longer one-size-fits-all. Understanding different lending models can help investors evaluate opportunities and balance risk and return, say Kirsten Bode and Gianpaolo Pellegrini.

Private credit has become an increasingly important part of European capital markets since the global financial crisis. As regulation has reshaped bank lending, private lenders have established themselves as a meaningful source of financing. Yet the market continues to evolve. Alongside direct lending, parallel lending is emerging and broadening the ways capital reaches businesses.

While both approaches seek to provide financing solutions alongside attractive risk-adjusted returns, they operate differently and offer distinct characteristics for borrowers and investors.

Direct lending: flexibility with disciplined underwriting

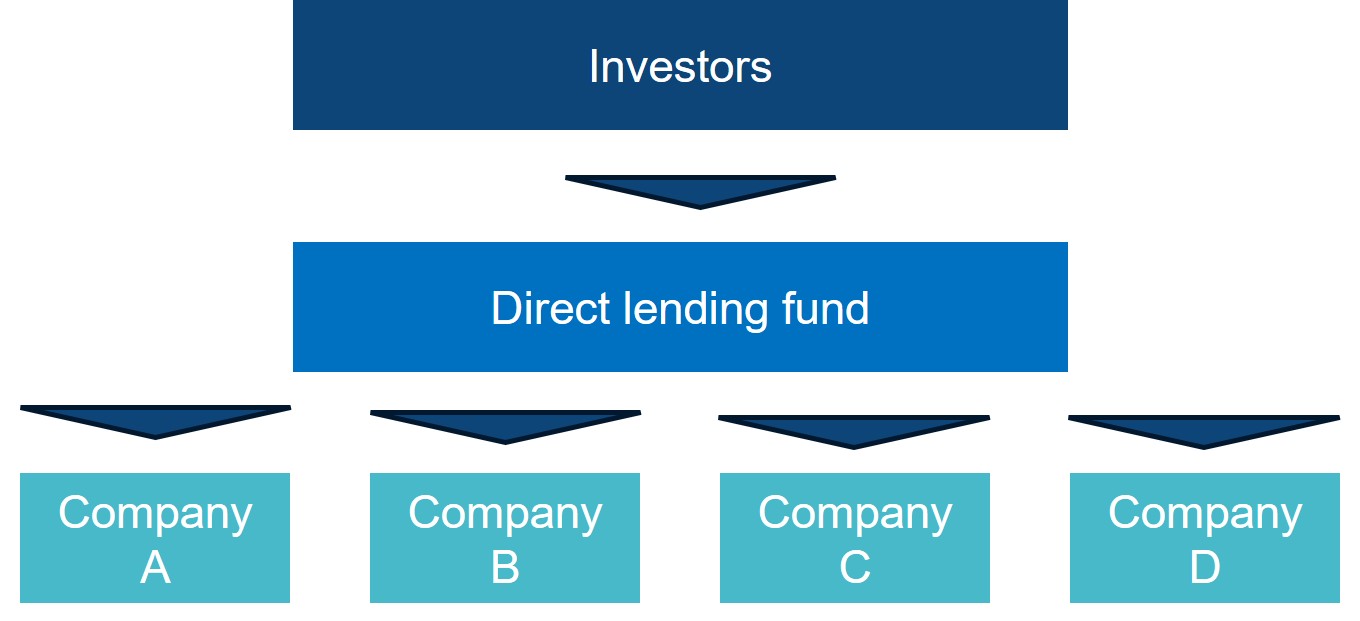

Direct lending remains the most established form of private credit. Under this model, private credit managers provide financing directly to companies, typically without a traditional bank acting as intermediary. It has become particularly relevant in Europe’s mid-market and lower middle-market segments, where financing needs often sit outside standard bank lending frameworks.

The growth of direct lending has been driven by several factors. Following the global financial crisis, banks faced higher capital requirements and more stringent regulation, reducing their appetite for certain types of corporate lending. Private lenders stepped in to fill this financing gap, providing businesses with access to capital for acquisitions, refinancing, leveraged buyouts, shareholder reorganisations and growth initiatives. In many cases, direct lenders can offer greater certainty of execution, faster decision-making and more customised financing solutions than traditional bank loan markets.

Direct lending transactions tend to be structured as senior secured unitranche facilities, combining senior and subordinated debt in a single instrument. This provides borrowers with a simpler capital structure while allowing lenders to negotiate covenant packages, reporting requirements and security protections directly with management teams and sponsors. The direct relationship between lender and borrower is a defining characteristic of the asset class and can facilitate greater transparency and ongoing engagement throughout the life of the investment.

Risk profiles vary significantly across the market. While larger-cap direct lending has attracted substantial inflows in recent years, resulting in increased competition and, in some cases, weaker lender protections, the lower middle market offers a broader and more differentiated opportunity set. Europe is home to hundreds of thousands of lower middle-market companies, many of which are market leaders within niche industries, yet remain underserved by larger lenders and struggle to access bank financing because of the regulatory pull back in lending.

Direct lending

Source: Muzinich & Co as of 31st May 2026, For illustrative purposes only.

Source: Muzinich & Co as of 31st May 2026, For illustrative purposes only.

Transactions in this segment are typically structured with leverage levels of approximately 3.5 –4.5x, supported by meaningful equity cushions from sponsors and more conservative capital structures. Combined with stronger covenant protections, closer lender engagement and extensive due diligence, this can contribute to a more defensive risk profile. The lower middle market is generally less intermediated than larger segments of the market, with fewer broadly marketed auction processes and a greater reliance on direct relationships. This can provide lenders with enhanced access to management teams, stronger negotiating positions and the ability to be more selective in deploying capital.

For investors, direct lending returns are primarily driven by contractual income and floating-rate exposure, with an illiquidity premium providing additional compensation relative to public markets. However, outcomes remain highly dependent on manager quality, underwriting discipline and portfolio construction. Successful managers are those able to source proprietary opportunities, maintain rigorous credit standards and actively monitor borrowers throughout the investment lifecycle.

Parallel lending: combining private and bank capital

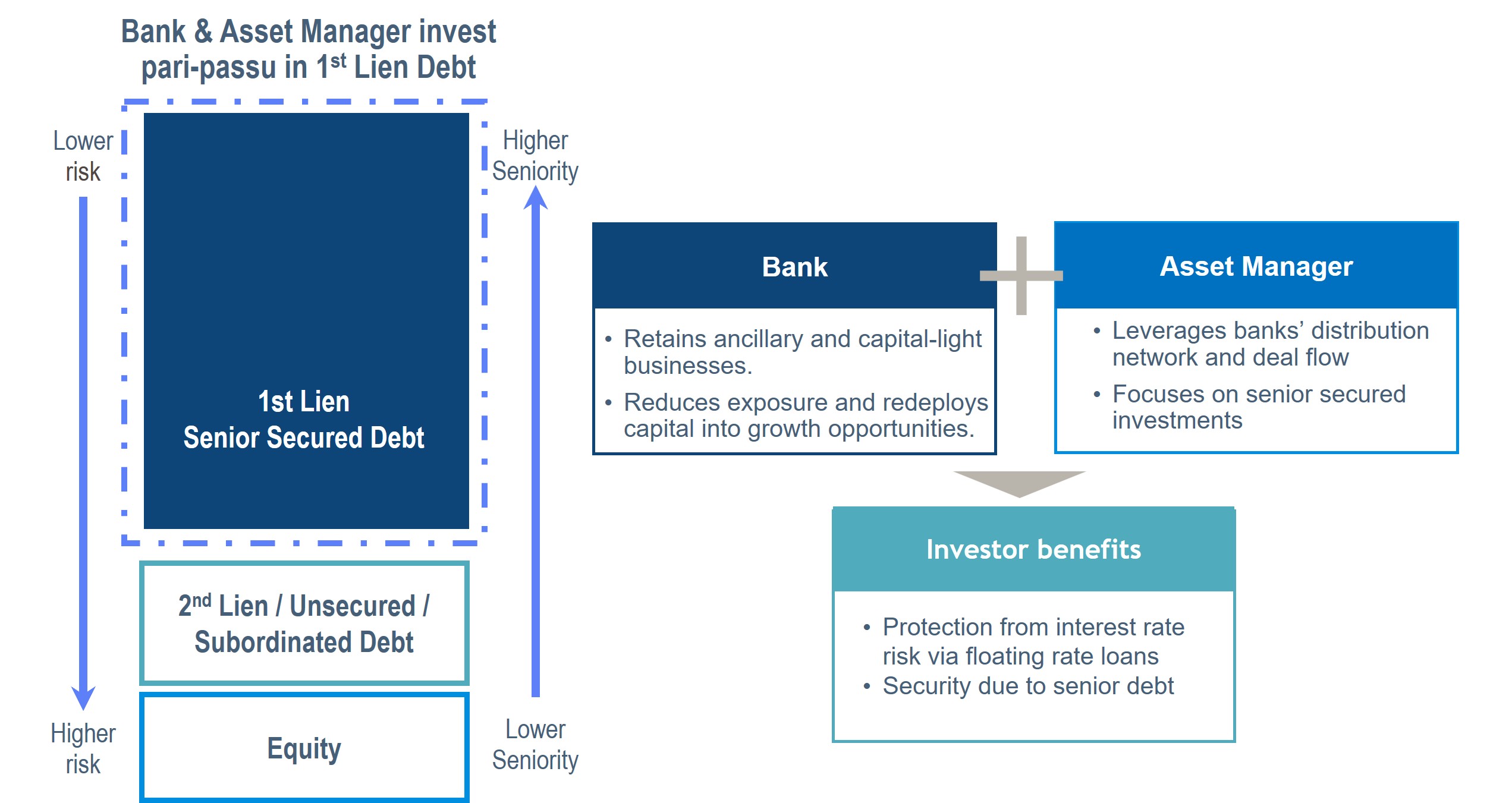

As private credit evolves, parallel lending is emerging as a complementary model that seeks to combine the strengths of traditional banking relationships with the flexibility and long-term capital provided by private lenders.

Rather than replacing banks, private lenders work alongside them, participating in the same financing under aligned economic terms and security structures. Banks continue to provide origination capabilities, via long-standing client relationships and local market expertise, while private lenders (especially if they are also locally based) contribute additional lending capacity and long-term investment capital. In practice, this allows borrowers to access larger pools of financing while maintaining continuity with their existing banking partners.

Parallel lending has developed in response to the reality that banks remain central to corporate lending in Europe. However, while banks continue to originate and service loans, regulatory capital constraints can limit the amount of risk they are willing to retain on their balance sheets. Parallel lending enables banks to continue supporting clients while sharing exposure with private capital providers.

For investors, parallel lending seeks to offer a distinct risk-return profile. Transactions are generally focused on companies with lower leverage levels, typically around 3.0–3.5x EBITDA, which may provide additional downside resilience through larger equity cushions and lower debt burdens. Structures also tend to be more bank-oriented, often incorporating scheduled amortisation and conservative documentation standards. Interest payments are typically fully cash-pay, with no payment-in-kind or toggle features, supporting a more predictable income stream.

A defining characteristic of parallel lending portfolios is their granularity. By partnering with multiple banks across different markets and jurisdictions, managers can build portfolios with exposure to well over 100 borrowers across a broad range of sectors and geographies. Rather than relying on a relatively concentrated portfolio of larger transactions, risk is spread across a diversified pool of companies. This diversification can reduce idiosyncratic borrower risk, mitigate the impact of individual credit events and contribute to more stable portfolio outcomes over time.

The collaborative nature of the model also introduces additional layers of underwriting and monitoring. Both banks and private lenders conduct credit analysis, creating multiple perspectives on borrower quality and risk. However, the trade-off is that decision-making can become more complex where multiple lending parties are involved, and investors may have less direct control over negotiations and restructuring outcomes than in directly originated transactions.

For many investors, parallel lending can therefore represent a lower-risk entry point into private credit, combining conservative leverage levels, diversified portfolio construction and the benefits of established banking relationships while still capturing the attractive income characteristics associated with private market lending.

How parallel lending works

Source: Muzinich & Co as of 31st May 2026, For illustrative purposes only.

Complementary approaches

The distinction between direct and parallel lending is less about which model is better and more about understanding the financing need each is designed to address.

Direct lending remains effective where flexibility, speed of execution and bespoke structuring are priorities, particularly in the lower middle market where lenders can benefit from stronger protections and less competitive dynamics. Parallel lending offers a collaborative approach that combines bank and private capital, with lower leverage levels, greater diversification and a potentially more defensive risk profile.

As private credit continues to mature, we believe these approaches are increasingly likely to coexist, expanding opportunities for investors and reinforcing private capital's role as a permanent part of the European lending landscape.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of June 2026 and may change without notice.

--------

Important information

Muzinich and/or Muzinich & Co. referenced herein is defined as Muzinich & Co., Inc. and its affiliates. Muzinich views and opinions. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall.

Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only.

This discussion material contains forward-looking statements, which give current expectations of future activities and future performance. Any or all forward-looking statements in this material may turn out to be incorrect. They can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Although the assumptions underlying the forward-looking statements contained herein are believed to be reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurances that the forward-looking statements included in this discussion material will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Further, no person undertakes any obligation to revise such forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

United Arab Emirates (UAE): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the UAE. It is intended solely for Professional Investors and should not be relied upon by any other person. This material has not been reviewed or approved by the UAE Securities and Commodities Authority, the UAE Central Bank or any other relevant authority. Nothing contained herein constitutes investment, legal, tax or other professional advice. Recipients should make their own independent assessment where appropriate.

Abu Dhabi Global Market (ADGM): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the ADGM. It is intended solely for Professional Clients (as defined by the Financial Services Regulatory Authority) and should not be relied upon by any other person. This material has not been reviewed or approved by the Financial Services Regulatory Authority or any other relevant authority in the UAE.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-06-01-18603

By clicking "Submit", I am (i) signing up to receive the Opinion Pieces from the "Opinions" page of the Muzinich & Co website, (ii) representing that the above information is true and accurate and (iii) agreeing to join the Muzinich & Co mailing list. I understand that Muzinich & Co will not add retail investors or individuals with personal email addresses to its mailing list and represent that I am not a retail investor. By providing my personal and professional information I am consenting to its use and disclosure in accordance with the Muzinich & Co. Privacy Policy. I understand that I may withdraw my consent and unsubscribe from receiving future communications by clicking "Unsubscribe" from the emails that are sent to me from Muzinich & Co.