Muzinich Weekly Market Comment: NOT GFC 2.0

Insight

March 23, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

It was another turbulent week for financial markets, with geopolitical developments continuing to overshadow earnings and economic data. However, we did gain our first read on how central banks view the impact of the conflict on their economies, with eleven policy meetings held over the course of the week.

Government bond curves have aggressively bear-flattened year to date, as investors price in lingering fears from the last major event shock – Covid-19 – when central banks prioritized anchoring inflation expectations, even at the expense of growth. This dynamic has pushed short-end yields sharply higher. Year to date, the 2-year Treasury is up 44 basis points (bps), the 2-year Gilt 90bps, and the 2-year Bund around 52bps. By contrast, 30-year yields are only slightly higher over the same period. The overnight index swap markets now price the Federal Open Market Committee (FOMC) on hold through 2026, while both the European Central Bank (ECB) and the Bank of England (BoE) are expected to deliver three 25bps hikes. This marks a stark reversal from the start of the year, when markets anticipated roughly two 25bps cuts from both the FOMC and the BoE, and no change in ECB policy.1

In corporate credit, markets have remained orderly. All sub-asset classes are slightly negative year to date except emerging market high yield, which is benefiting from geographic diversification, a large energy sector and underweight investor positioning.

The US dollar depreciated against G10 currencies this week as narrowing interest rate differentials moved against it. Elsewhere, the trends observed in the first two weeks of the conflict extended into a third; equity markets closed lower for a third consecutive week, and energy prices continued to climb. Brent crude is now up around 80% year to date, with European gas prices rising by more than 100%.

The question on everyone’s mind this week is simple: how bad can it get? The uncomfortable answer is Global Financial Crisis (GFC) 2.0. While that may sound dramatic, there are clear parallels that should not be ignored.

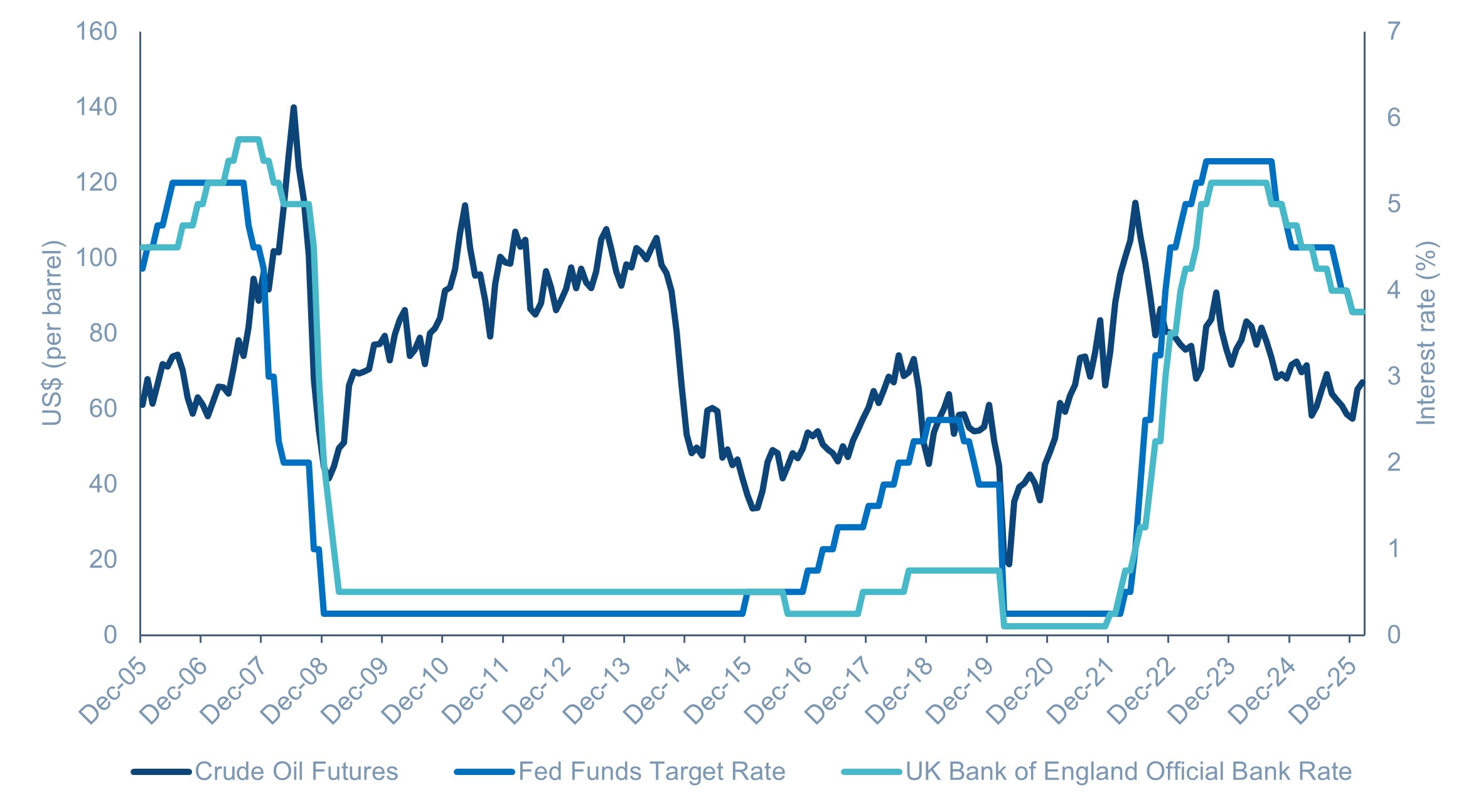

Firstly, oil prices surged to around US$145 per barrel in 2008, driven by a near-perfect storm of supply constraints and strong demand. Rapid growth in emerging markets, particularly China and India, led to a sharp increase in global energy consumption. At the same time, non-OPEC supply was weakening, with declines in key regions such as the North Sea and Mexico’s Cantarell field. This tightening of supply was further compounded by geopolitical disruptions in Venezuela, which cut off sales to ExxonMobil, while Iraq experienced sabotage attacks on export pipelines. Under our bearish scenario for the outlook of oil prices, we project that prices could reach similar levels to those seen in 2008.2

The next area of similarity lies in central bank policy. In 2008, both the Federal Reserve (Fed) and the BoE had begun loosening policy but paused for an extended period from the second to the fourth quarter of 2008. Policymakers found themselves caught between a rock and a hard place of rising inflation expectations, driven largely by surging oil prices and an economic slowdown, “Stagflation” became a widely used term. See Chart of the Week.

Fast forward to this past week’s policy meetings, and the comparison is somewhat striking. Across eleven meetings, nine central banks held rates steady, delivering a consistent message; they stand ready to act if inflation expectations fail to remain anchored. The two outliers were the Reserve Bank of Australia (RBA), which raised its policy rate by 25bps to 4.10%, its second consecutive hike this year.3 The decision reflected heightened upside risks to inflation from the energy price shock linked to the Iran conflict, alongside a tighter-than-expected labour market.4 Meanwhile, Brazil’s central bank (BCB), widely regarded as one of the smartest policymakers during the Covid-era inflation shock, cut rates by 25bps to 14.75%. Notably, policy in Brazil still remains highly restrictive: the ex-ante real rate declined only marginally, to 10.3% from 10.6%, still more than double the BCB’s estimated neutral rate of around 5%.5

As for the BoE and the FOMC, both faced increasingly concerning activity data. The Bank of England’s Monetary Policy Committee had January growth figures in front of them, which came in unexpectedly flat (0.0% month-on-month), suggesting that activity may have been stalling even before the recent geopolitical tensions.6 Meanwhile, the FOMC was presented with a super weak February nonfarm payrolls report, which showed employment contracting by 92,000 and the unemployment rate rising to 4.4%, its highest level in nearly five years.

Against this backdrop, the BoE voted unanimously to leave rates unchanged at 3.75%, its first decision without dissent in four and a half years. Governor Andrew Bailey warned that policy must “respond to the risk of a more persistent effect on UK CPI inflation,” adding, “Whatever happens, our job is to ensure inflation returns to its 2% target”.7 Meanwhile, the FOMC also left its policy rate unchanged at 3.50%–3.75%, with one dissent from Governor Stephen Miran in favour of a cut. The key takeaway from Chair Powell’s press conference was that it remains too early to assess the impact of rising oil prices on the US economy, and his comments further reinforced the view that the committee is still some distance from resuming rate cuts. “The thing that’s really important that we see this year is progress on inflation,” Powell said. “If we don’t see that progress, then you won’t see rate cuts.” 8

The next comparison with 2008 is valuations. Corporate credit spreads, then as now, were at cycle lows, with investment grade spreads below 90bps and high yield below 250bps in the US before the conflict began.9 Equity market valuations also appear stretched. In June 2007, the Shiller CAPE, an indicator that provides stable measure of market valuation than traditional P/E ratios, stood at 27.4. Today, the reading is significantly higher at around 38.3.10 Further concerning is the growing concentration in equity market returns and profits. Since the launch of ChatGPT in 2022, approximately 65–75% of S&P 500 returns and profits have been driven by just 42 companies linked to generative AI.11 At the same time, concentration has never been higher with US equities now representing 75% of the MSCI world index.12

For a crisis to unfold, a tipping point – a Minsky moment – is required. In 2008, that trigger was the subprime MBS (Mortgage-Backed Securities) market. Today, a more contentious question is whether private credit could play a similar role. The asset class does have some uncomfortable parallels. Like MBS and CDOs (Collateralized Debt Obligations), private credit remains fairly opaque, with valuations based on internal models rather than market pricing. At the same time, default rates are rising; Fitch recorded 9.2% in 2025, with forecasts suggesting they could climb further.13 Distress is also being masked through payment-in-kind structures, echoing how credit deterioration was obscured pre-2008. Meanwhile, managers have begun restricting and gating redemptions amid concerns over liquidity, recalling the early signs of strain seen in 2007, while banks remain indirectly exposed through financing lines, raising the risk of broader systemic spillovers.

There are, however, important mitigating factors that differentiate today from 2008, particularly the stronger position of household, corporate and bank balance sheets. Banks are far better capitalized following post-Dodd-Frank reforms. The current policy environment also remains supportive, with the US administration modestly easing financial regulation, and governments globally continuing to provide economic support through fiscal spending.

As a result, it is highly unlikely that the current conflict will trigger a debt-driven deleveraging crisis of the kind seen in 1929 or 2008. This underpins our base case of an event-driven correction. However, the risk remains that, should the conflict persist longer than expected, it could evolve into an economic crisis and downturn.

Chart of the Week: FOMC and MPC paused loosening policy rates in 2008

Source: Bloomberg, as of 23rd March 2026. For illustrative purposes only.

All sources are Bloomberg unless otherwise stated.

Past performance is not a reliable indicator of current or future results.

References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

References

1. Bloomberg, as of March 20, 2026

2. Muzinich Weekly Market Comment: “Energy Shock,” March 16, 2026

3. Reserve Bank of Australia, as of 17th March 2026.

4. Bloomberg, “AUSTRALIA REACT: Oil Spike, Capacity Strain Drive March Hike,” March 17, 2026

5. Bloomberg, “BRAZIL REACT: Timid Cut Is Reasonable War-Time Compromise,” March 19, 2026

6. The Guardian, as of 13th March 2026. “UK economy unexpectedly flatlined in January, official figures show”

7. Bloomberg, “BoE ‘Ready to Act’ on Inflation After 9-0 Vote to Hold Rates, “March 19, 2026

8. Bloomberg, “Powell Says Too Soon to Judge War as Prices Keep Fed on Hold,” March 19, 2026

9. Bloomberg, as of March 20, 2026

10. Bloomberg, as of March 20, 2026

11. J.P. Morgan, Eye on the Market: Outlook 2026, “Smothering Heights,” January 1, 2026

12. MSCI Developed Market Indexes, as of March 19, 2026

13. Reuters, “US private credit defaults hit record 9.2% in 2025, Fitch says,” March 6, 2026

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of March 2026 and may change without notice.

--------

Important Information

Muzinich & Co., “Muzinich” and/or the “Firm” referenced herein is defined as Muzinich & Co. Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Any forward-looking information or statements expressed in the above may prove to be incorrect. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Muzinich gives no undertaking that it shall update any of the information, data and opinions contained in the above.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom.