Rise above the noise

Insight

May 19, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

With yields reset and fiscal dynamics evolving, the fixed income opportunity set is changing. Tatjana Greil-Castro examines why participation, compounding and relative balance-sheet strength support a strategic allocation to corporate credit over sovereign bonds. As investors consider their own pension outcomes, short-dated, actively managed corporate credit can offer a defensive entry point with the potential to outpace inflation.

Fixed income investing is entering a structurally different phase. After more than a decade defined by ultra-low interest rates, quantitative easing and suppressed yields, investors are again able to earn meaningful income from bond markets. Yet the opportunity set is evolving, and traditional assumptions about risk and safety merit reconsideration.

In an environment shaped by fiscal expansion, demographic change and shifting monetary policy, the distinction between government bonds and corporate credit is becoming increasingly important. At the same time, behavioural responses to volatility continue to influence allocation decisions, often to the detriment of long-term outcomes.

Several interrelated dynamics stand out. Time in the market has historically mattered more than attempts at tactical timing in credit investing, while compounding income – rather than price appreciation – has driven most fixed income returns over the long term. Corporate balance sheets may, in many cases, offer a structurally stronger foundation than sovereign issuers.

These considerations suggest corporate credit could be a core allocation in fixed income portfolios.

Time in the market

Periods of heightened uncertainty often encourage investors to delay allocation decisions. While this response may feel prudent, history suggests that in fixed income – particularly credit – remaining on the sidelines can itself become a risk.

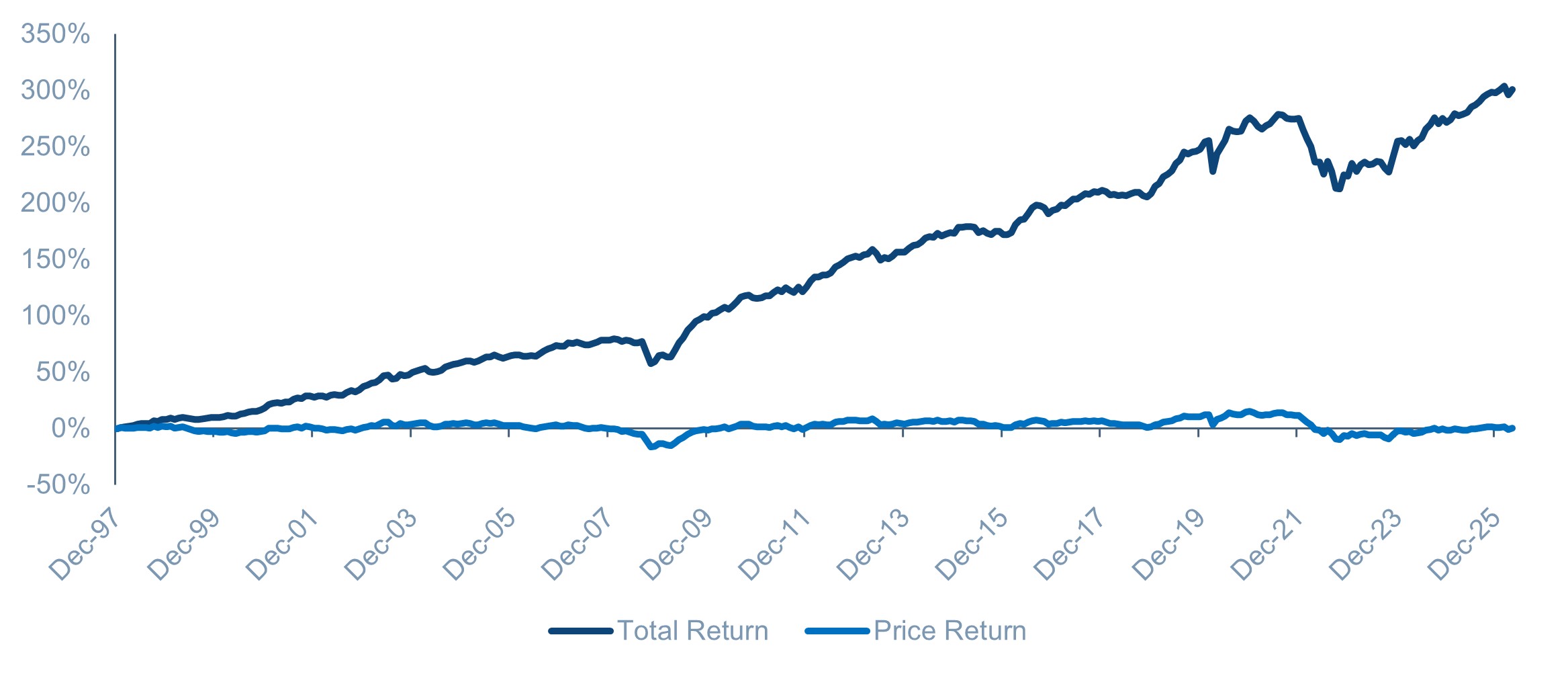

In an increasingly volatile world shaped by rapid geopolitical, economic and policy changes, we believe investors should carefully consider their duration exposure. While global government bond indices typically carry durations of 7–9 years or more, corporate indices are materially lower – c. 6 years for investment grade and 3-4 years for high yield.1 Shorter-dated corporate credit can therefore offer both downside protection and the potential for compelling real-term income. Income-generating assets like corporate credit have historically delivered returns driven primarily by coupon income rather than capital gains (Figure 1). For long-term investors, this distinction is important: credit returns are typically earned through participation rather than precise market timing.

Short-term narratives can make this difficult. Market headlines often amplify perceived risks and obscure underlying fundamentals. In credit markets, this behavioural challenge is particularly evident. When spreads widen, investors hesitate for fear of further deterioration. When spreads tighten, they hesitate again, concerned valuations are less compelling. In both cases, indecision can result in foregone income and missed compounding.

Understanding the structural drivers of credit returns helps address this tension. Unlike equities, where outcomes depend heavily on earnings growth and valuation changes, credit returns are predominantly a function of coupon income and reinvestment. Price volatility tends to be cyclical and often mean-reverting, while income accrues consistently. Even during periods of stress, this income component provides both ballast and a mechanism for recovery through reinvestment at higher yields.

The longer-term evidence reinforces this point. Most of the cumulative returns in global corporate credit since inception have come from income rather than price appreciation (Figure 1). Time in the market has historically mattered far more than attempts at tactical timing.

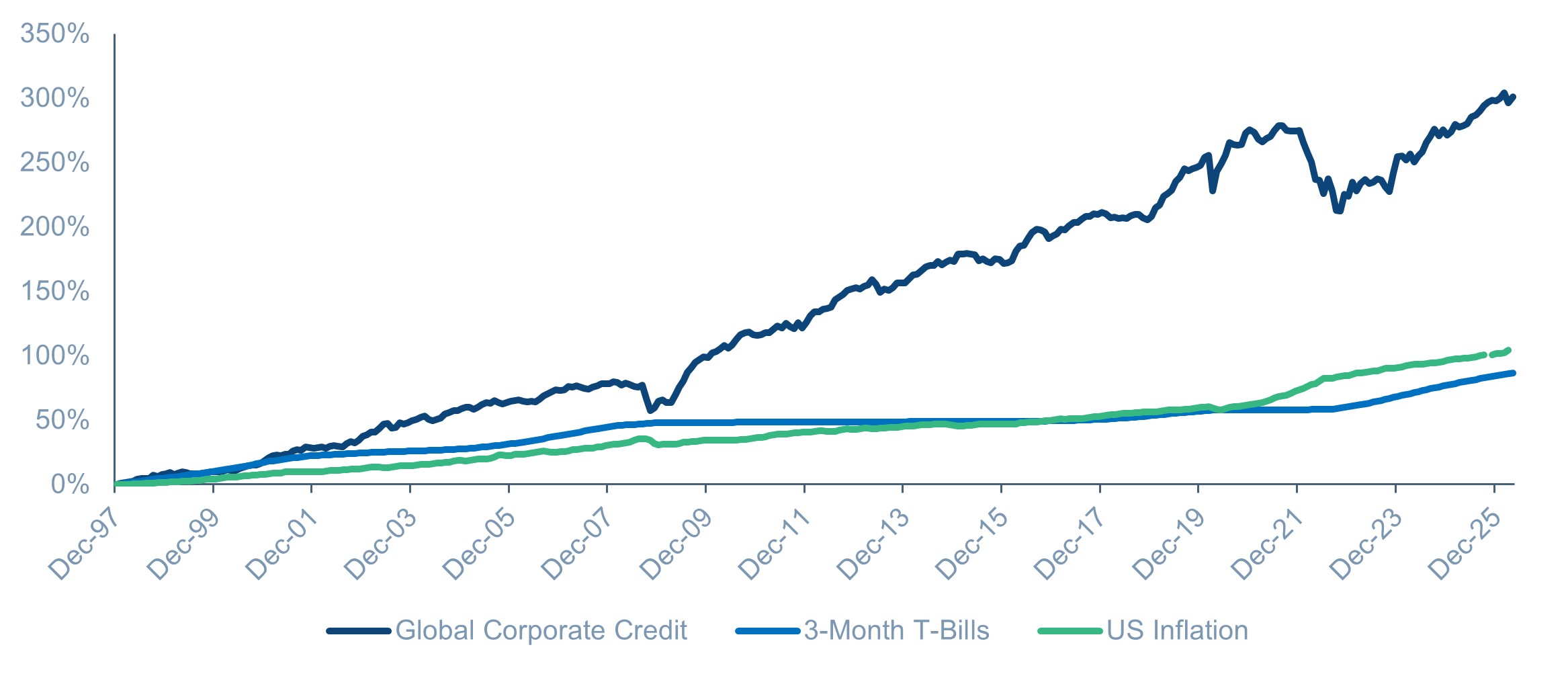

Compounding is a further differentiator. Cash – proxied by three-month Treasury bills – has delivered a negative real return after inflation over the long term (Figure 2). By contrast, global corporate credit has generated returns meaningfully above inflation, largely due to the reinvestment of income. While cash preserves nominal stability, it has struggled to preserve purchasing power. Credit income, compounded over time, has historically provided a more effective means of sustaining real wealth.

Figure 1 – Returns are driven by income, not price appreciation

Past performance is not a reliable indicator of future results.

Source: ICE Index Platform, as of 21st April 2026. ICE BofA Global Corporate & High Yield Index (GI00). Index selected by Muzinich as best available proxy for the respective asset classes. For illustrative purposes only, not to be construed as investment advice. Index performance is for illustrative purposes only. You cannot invest directly in the index.

Figure 2 – Compounding, not cash, beats inflation

Past performance is not a reliable indicator of future results.

Source: Bloomberg and ICE Index Platform, as of 21st April 2026. ICE BofA Global Corporate & High Yield Index (GI00), ICE BofA US 3-Month Treasury Bill index (G0O1) and US CPI Urban Consumers SA (CPI INDX). Indices selected by Muzinich as best available proxies for the respective asset classes. For illustrative purposes only, not to be construed as investment advice. Index performance is for illustrative purposes only. You cannot invest directly in the index.

Re-evaluating sovereign risk

Fixed income can broadly be divided into government bonds and spread products, with corporate credit the largest component of the latter. Government bonds - particularly those issued by developed markets such as the US – are typically viewed as the defensive core of portfolios, supported by their perceived security and liquidity. The US Treasury market, for example, is often described as “risk free,” based on the assumption that a highly rated sovereign can always service its debt.

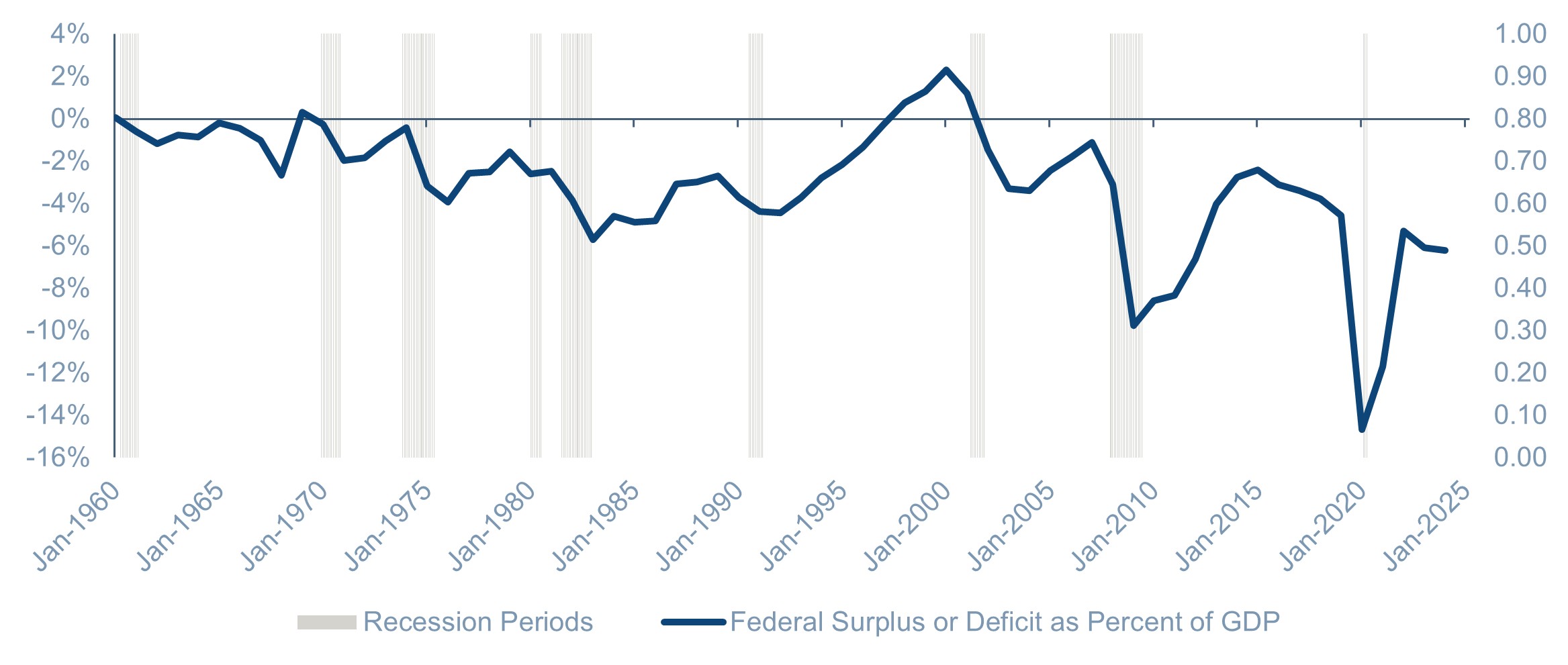

However, it is increasingly valid to question whether these assumptions remain appropriate. In the US, government debt exceeds GDP, spending continues to outpace revenues and the current account deficit highlights reliance on external financing. Federal spending has risen to roughly 20% of GDP,2 while revenues have struggled to keep pace, resulting in a widening primary deficit.

Other economies paint a similar picture of deteriorating fiscal dynamics.3 In the Euro area, while no longer in the depths of debt crises of previous decades, fiscal positions remain stretched. Government debt stands at approximately 88 – 90% of GDP, with deficits around 3%, reflecting a structurally weaker position than pre-COVID norms.4 Moreover, this trend is global: according to the IMF, public debt reached almost 94% of GDP in 2025 and is projected to rise further in the coming years.5

Structural pressures - including defence, healthcare, pensions and demographic trends – are unlikely to ease materially, suggesting deficits will persistent; debt continues to compound and rising interest costs further strain fiscal sustainability.

For investors, risk extends beyond default. Returns depend on inflation, currency stability and the credibility of fiscal policy over time. As markets begin to reassess long-held assumptions around sovereign “risk-free” status, this shift alone can influence valuations and borrowing costs.

Figure 3 – Increasing government deficits

Source: Federal Reserve Bank of St Louis and Bloomberg. Quarterly data as of March 31st, 2025. Most recent data available used. Muzinich views and opinions for illustrative purposes only, not to be construed as investment advice.

Source: Federal Reserve Bank of St Louis and Bloomberg. Quarterly data as of March 31st, 2025. Most recent data available used. Muzinich views and opinions for illustrative purposes only, not to be construed as investment advice.

Against this backdrop, we believe corporate credit offers a compelling alternative.

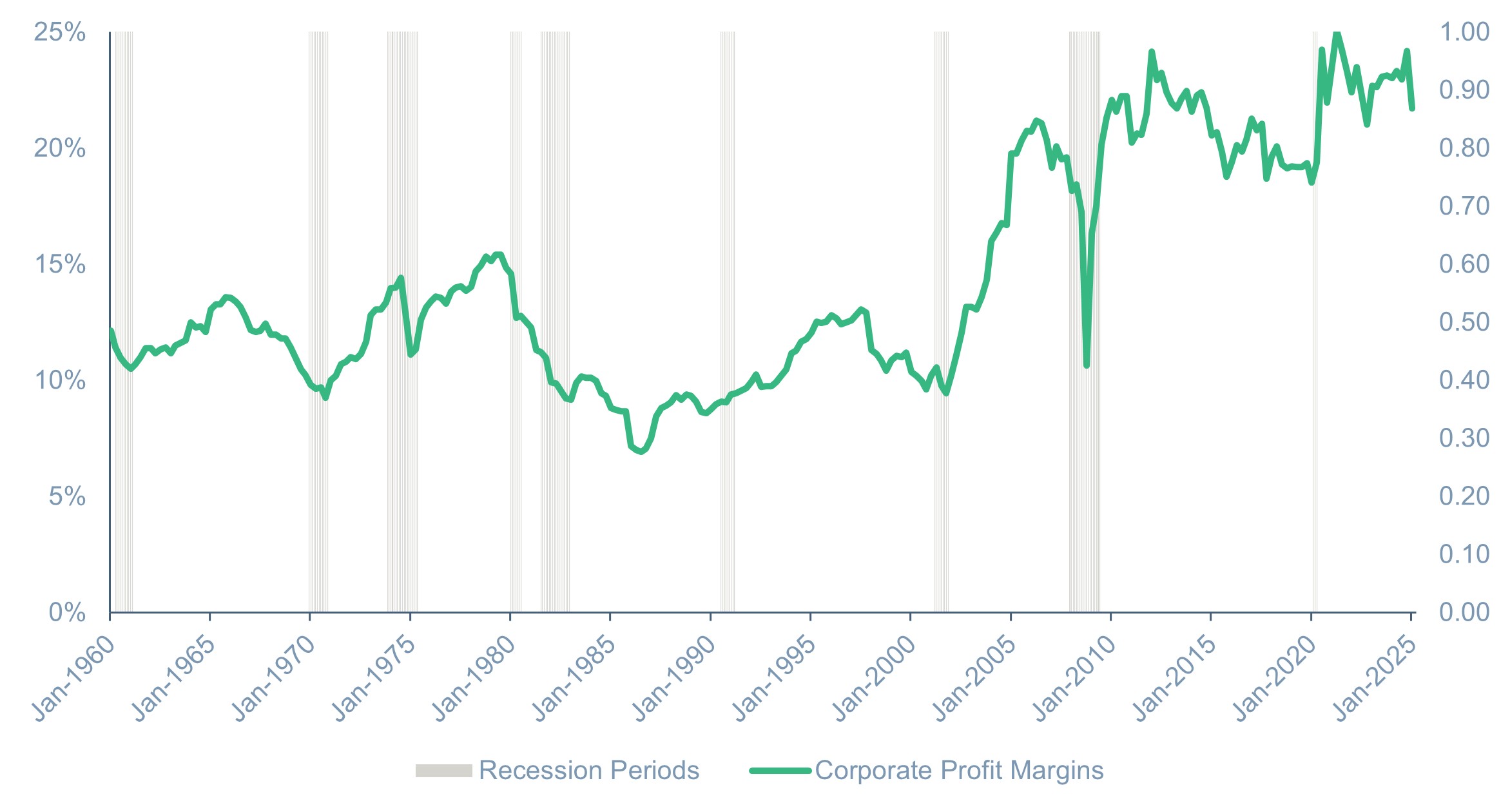

While priced at a spread over government bonds, corporates provide additional return potential. Many corporate issuers demonstrate strong free-cash-flow generation, pricing power and disciplined capital allocation. Although leverage increased during the ultra-low-rate period of the previous decade, much of the corporate sector termed out debt at historically low coupons, reducing near-term refinancing pressure. Corporate management teams also retain flexibility: they can adjust capital expenditure, dividends, asset sales or financing strategies. Sovereigns, constrained by political realities, often have less room to manoeuvre.

From a relative-value perspective, this creates an attractive dynamic. Corporate credit offers a yield premium over sovereign bonds, often alongside stronger balance-sheet discipline and clearer pathways to debt stabilisation. Large global companies with diversified revenues and resilient cash-flow generation may reasonably trade at spreads close to sovereign levels, particularly when leverage and interest-coverage metrics compare favourably with those of developed-market governments. Over time, we believe some corporate debt may trade inside government debt, displaying a negative spread and signifying a fundamental shift in perceived credit quality and value.

In this context, current spreads should not automatically be interpreted as a signal there are less opportunities. Instead, they may reflect fundamental resilience and sustained demand for income-generating assets with strong fundamentals. For investors seeking durable income with disciplined risk exposure, corporate credit may represent a structurally compelling allocation within fixed income.

Figure 4 – Healthy corporate profit margins

Source: Federal Reserve Bank of St Louis and Bloomberg. Quarterly data as of March 31st, 2025. Most recent data available used. Muzinich views and opinions for illustrative purposes only, not to be construed as investment advice.

The credit advantage

The importance of long-term investing extends beyond individual portfolios. In many regions – particularly Europe – demographic pressures and fiscal constraints are increasing the need for greater private participation in capital markets. Ageing populations and slower workforce growth are straining government-funded pension systems, placing more responsibility on private savings to support retirement security.

Yet household participation in capital markets remains relatively low in parts of Europe, reflecting risk aversion, policy structures and a preference for cash savings. The economic reality, however, is clear: long-term wealth accumulation depends on market participation and the power of compounding.

Credit markets play a central role in this framework. Fixed income investments can provide predictable income, diversification and transparent risk structures. While credit investing requires rigorous analysis and diversification, it allows investors to manage uncertainty rather than avoid it. No strategy eliminates risk, but well-constructed portfolios can absorb volatility and recover over time.

Market cycles and shifting narratives are inevitable, but the structural drivers of fixed income returns – income generation and reinvestment – remain consistent. In credit markets, long-term outcomes have historically been driven more by income and compounding than by price appreciation.

At the same time, the traditional hierarchy within fixed income merits reassessment. Government bonds remain important for liquidity and risk management but rising structural deficits and expanding debt burdens challenge the assumption that sovereign balance sheets are inherently stronger than those of well-managed corporations. Many corporate issuers today exhibit disciplined capital allocation, resilient cash flows and operational flexibility.

For investors seeking durable income, real return potential and disciplined risk exposure, corporate credit offers a compelling combination of yield, structural resilience and compounding power.

References

1. ICE Index Platform, as of 21st April 2026. ICE BofA Global High Yield Constrained (HW0C), ICE BofA Global Corporate Index (G0BC).

2. Federal Reserve Bank of St Louis, as of 16th October 2025. Federal Net outlays as a % of gross domestic product. Latest available data used.

3. OECD Statistics, as of 29th July 2025. What is government deficit and why does it matter?

4. Eurostat, as of 22nd January 2026. Government debt at 88.5% of GDP in euro area.

5. IMF, as of April 2026. “Fiscal policy under pressure: high debt, rising risks.”

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of April 2026, and may change without notice.

--------

Index descriptions

GI00 – The ICE BofA Global Corporate & High Yield Index tracks the performance of investment grade and below investment grade corporate debt publicly issued in the major domestic and eurobond markets. Qualifying securities must be rated by either Moody’s, S&P or Fitch, have at least one year remaining term to final maturity, at least 18 months to maturity at point of issuance and a fixed coupon schedule.

US CPI Urban Consumers SA (CPI INDX) – Consumer prices (CPI) are a measure of prices paid by consumers for a market basket of consumer goods and services. The yearly (or monthly) growth rates represents the inflation rate.

ICE BofA US 3-Month Treasury Bill Index (G0O1) ICE BofA US 3-Month Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. At the end of the month that issue is sold and rolled into a newly selected issue. The issue selected at each month-end rebalancing is the outstanding Treasury Bill that matures closest to, but not beyond, three months from the rebalancing date. In order to qualify for inclusion, securities must be auctioned on or before the third business day before the last business day of the month and settle before the following calendar month end.

Important information

Muzinich and/or Muzinich & Co. referenced herein is defined as Muzinich & Co., Inc. and its affiliates. Muzinich views and opinions. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall.

Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only.

This discussion material contains forward-looking statements, which give current expectations of future activities and future performance. Any or all forward-looking statements in this material may turn out to be incorrect. They can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Although the assumptions underlying the forward-looking statements contained herein are believed to be reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurances that the forward-looking statements included in this discussion material will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Further, no person undertakes any obligation to revise such forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

Abu Dhabi Global Market (ADGM): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the ADGM. It is intended solely for Professional Clients (as defined by the Financial Services Regulatory Authority) and should not be relied upon by any other person.

This material has not been reviewed or approved by the Financial Services Regulatory Authority or any other relevant authority in the UAE.

United Arab Emirates (UAE): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the UAE. It is intended solely for Professional Investors and should not be relied upon by any other person.

This material has not been reviewed or approved by the UAE Securities and Commodities Authority, the UAE Central Bank or any other relevant authority.

Nothing contained herein constitutes investment, legal, tax or other professional advice. Recipients should make their own independent assessment where appropriate.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-04-23-18362

By clicking "Submit", I am (i) signing up to receive the Opinion Pieces from the "Opinions" page of the Muzinich & Co website, (ii) representing that the above information is true and accurate and (iii) agreeing to join the Muzinich & Co mailing list. I understand that Muzinich & Co will not add retail investors or individuals with personal email addresses to its mailing list and represent that I am not a retail investor. By providing my personal and professional information I am consenting to its use and disclosure in accordance with the Muzinich & Co. Privacy Policy. I understand that I may withdraw my consent and unsubscribe from receiving future communications by clicking "Unsubscribe" from the emails that are sent to me from Muzinich & Co.