Muzinich Weekly Market Comment: Animal spirits

Insight

July 13, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

Despite renewed geopolitical tensions and higher energy prices, investors have remained remarkably resilient. With markets looking through near-term risks and focusing instead on resilient growth, AI-driven demand and a higher-for-longer interest rate backdrop, are animal spirits beginning to reassert themselves?

Markets returned to the frustrating dynamic that dominated much of the second quarter: Middle East tensions. The fragile peace process and negotiations toward a permanent US-Iran settlement came under pressure as both sides exchanged physical and verbal fire. By late Thursday, however, investors began to unwind worst-case all-out-war scenarios after the US reaffirmed its commitment to a diplomatic solution, with officials describing the discussions as “technical talks”. Even so, the skirmishes underscored the fragility of the interim agreement signed by Tehran and Washington in June.1

Commodity prices still ended the week higher, with the Bloomberg Commodity Index (BCOM) up more than 2.5% and energy prices nearly 5% higher, reflecting greater uncertainty and a larger risk premium to energy supply. The US Treasury’s decision to revoke the waiver allowing global sales of Iranian oil posed the biggest challenge yet to last month’s interim peace agreement. This was compounded by a decline in Persian Gulf oil exports, now at 71% of normal levels, down from a June peak of 83% just before the flare-up. Flows through the Strait of Hormuz are running at 42% of normal on a seven-day moving average,2 with the daily vessel count falling from 21 on Sunday (5 July) to 7 on Friday (10 July).3

Financial markets moved accordingly, with asset classes and regions most exposed to higher energy prices underperforming. Commodity-linked currencies, including the Norwegian krone and Brazilian real, outperformed, while Europe lagged in both fixed income and equities given its status as a net energy importer. In corporate credit, high yield outperformed investment grade. The main outlier was Japanese government bonds, where long-end yields fell 17 basis points (bps). The catalyst was this week’s 30-year auction, which attracted the strongest demand since 2019. The bid-to-cover ratio rose to 4.55 from a 12-month average of 3.41, as investors were drawn to the first-ever 4% coupon on a Japanese Government Bond (JGB).4 Finance Minister Satsuki Katayama’s comments that the government wants to encourage pension funds to increase allocations to domestic financial assets added further support to the long end of the JGB curve.5

Moving away from the Middle East noise, we searched for some meaningful market signals and developments that could have potentially gone under the radar. In Europe, the European Central Bank’s (ECB's) 10–11 June meeting minutes showed the Governing Council leaning toward another 25bps hike, likely in September. Several members characterized the recent inflation impulse as more of an oil shock than a broad-based energy shock. Indirect effects were increasingly evident, although some policymakers argued the baseline projections already incorporated substantial second-round effects and further suggested scepticism that the full impact would ultimately materialize.6 Notably, the meeting predated the most recent round of US–Iran peace talks, the subsequent decline in oil prices and June's softer euro-area inflation report. The Overnight Index Swap (OIS) market prices a 73% probability of a September hike.7

Meanwhile, on the political front, France's Marine Le Pen has been cleared to stand in the 2027 presidential election – albeit under an electronic-tag condition that she has contested – and she has confirmed she will run.8 In the UK, Andy Burnham looks set to become the next Labour leader and prime minister, with his bid now backed by 322 of Labour’s 403 MPs. As the only declared candidate, he sits just one endorsement short of the 323 that would make it mathematically impossible for a challenger to enter the race.9

In the US, the minutes of the June 16–17 Federal Open Market Committee (FOMC) meeting – the first chaired by Kevin Warsh – struck a tone of growing concern over inflation, even as worries over the labour market eased somewhat. Participants generally judged that upside risks to price stability remained elevated, while downside risks to achieving maximum employment had moderated a little. The committee walked through several scenarios for how the economy might evolve. In one –featuring moderating inflation – most participants expected the Federal Reserve (Fed) would "maintain or eventually lower the target range for the federal funds rate". In another – where inflation stays elevated on strong AI-driven demand, high energy prices and tariffs – most judged that "some policy firming would likely be warranted”.10 The OIS is currently pricing a 96% probability of a 25bps rate hike in October, with around 44bps of cumulative tightening expected over the cycle and the policy rate peaking in April 2027. 7

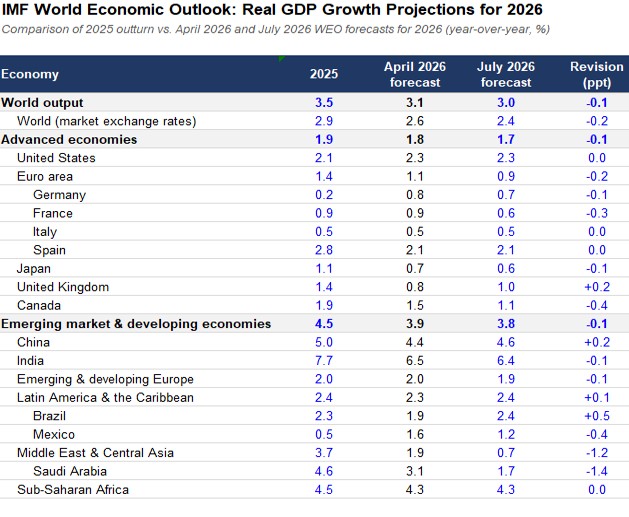

Finally, the International Monetary Fund (IMF) released its World Economic Outlook update, striking a notably more sanguine tone than its downbeat April report (see Chart of the Week). Its verdict points to the global economy having, so far, weathered the energy supply shock better than feared. Global growth is now pencilled in at 3.0% for 2026 and 3.4% for 2027, down from 3.5% in 2025, but only marginally below the April projection. The modest slowdown reflects the Middle East conflict, partly offset by AI-driven momentum in the global technology cycle. Even energy-importing economies in Europe and Asia held up better than feared, leaning on oil and gas inventories to avoid shortages, while the AI boom kept hardware exporters such as Korea and China growing well above forecast. The US, a net energy exporter, is expected to grow faster this year than in 2025, at 2.3%, while Brazil's forecast received the largest upgrade, to 2.4%. Risks are more balanced than in April, with renewed Middle East conflict as the standout threat, alongside a possible correction in technology-driven expectations.11

Aside from the economics, what was also notable last week was how resilient sentiment remained, with the VIX hardly budging and closing the week with a 15 handle, a level that suggests little concern. Could investors simply be playing the July seasonality card? You would have to go back to 2014 to find the last negative July for the S&P 500, and back to 2015 for US high yield. The historical reasoning behind July's seasonality includes front-running optimism ahead of Q2 earnings (which kick off in mid-July), quarter-end and half-year rebalancing inflows, or even the unwinding of "sell in May" positioning. In 2026, perhaps it is simply the surprising resilience of the global economy in response to an oil supply shock of a scale not seen since the OPEC shocks of the 1970s that is galvanizing animal spirits.

Chart of the week: GDP resilience

Source: International Monetary Fund, “World Economic Outlook (WEO) Update: Global Economy in Crosscurrents of War and Technology,” July 2026. Muzinich views and opinions are subject to change. For illustrative purposes only, not to be construed as investment advice or an invitation to engage in any investment activity.

Source: International Monetary Fund, “World Economic Outlook (WEO) Update: Global Economy in Crosscurrents of War and Technology,” July 2026. Muzinich views and opinions are subject to change. For illustrative purposes only, not to be construed as investment advice or an invitation to engage in any investment activity.

References

All sources are Bloomberg unless otherwise stated.

Past performance is not a reliable indicator of current or future results.

References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of July 10, 2026, and may change without notice. All data figures are from Bloomberg, as of July 10, 2026, unless otherwise stated.

--------

Important information

Muzinich & Co., “Muzinich” and/or the “Firm” referenced herein is defined as Muzinich & Co. Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Any forward-looking information or statements expressed in the above may prove to be incorrect. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Muzinich gives no undertaking that it shall update any of the information, data and opinions contained in the above.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

United Arab Emirates (UAE): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the UAE. It is intended solely for Professional Investors and should not be relied upon by any other person. This material has not been reviewed or approved by the UAE Securities and Commodities Authority, the UAE Central Bank or any other relevant authority. Nothing contained herein constitutes investment, legal, tax or other professional advice. Recipients should make their own independent assessment where appropriate.

Abu Dhabi Global Market (ADGM): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the ADGM. It is intended solely for Professional Clients (as defined by the Financial Services Regulatory Authority) and should not be relied upon by any other person. This material has not been reviewed or approved by the Financial Services Regulatory Authority or any other relevant authority in the UAE.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom.2026-07-13-18954

By clicking "Submit", I am (i) signing up to receive the Opinion Pieces from the "Opinions" page of the Muzinich & Co website, (ii) representing that the above information is true and accurate and (iii) agreeing to join the Muzinich & Co mailing list. I understand that Muzinich & Co will not add retail investors or individuals with personal email addresses to its mailing list and represent that I am not a retail investor. By providing my personal and professional information I am consenting to its use and disclosure in accordance with the Muzinich & Co. Privacy Policy. I understand that I may withdraw my consent and unsubscribe from receiving future communications by clicking "Unsubscribe" from the emails that are sent to me from Muzinich & Co.