Muzinich Weekly Market Comment: Thank you, Powell – a steady hand in unsteady times

Insight

May 18, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

As markets grapple with rising geopolitical tensions, persistent inflation and renewed uncertainty over the path of US interest rates, Jerome Powell exits the Federal Reserve after steering the global economy through one of the most volatile periods in modern history. This week’s market moves suggest his successor, Kevin Warsh, inherits a far more complicated inflation backdrop than many investors had anticipated.

Investors moved into risk-off mode this week as sentiment deteriorated across most markets. The VIX – our preferred gauge of uncertainty – trended steadily higher, marking its first week-on-week increase since late March. Political uncertainty intensified on several fronts, while incoming economic data suggested the Iran conflict is beginning to exert a measurable impact on inflation.

Government bonds had nowhere to hide, with yields rising across the entire maturity curve. US Treasurys underperformed at the front end as investors reassessed the direction of the Federal Reserve’s (Fed’s) next policy move. The debate has shifted – no longer a question of when the Fed cuts, but whether it hikes. Overnight interest rate swaps reflect the scale of this repricing, now embedding a 65% probability of tightening before year-end, and fully discounting an additional 25 basis points (bps) of hikes by Q1 2027.1

The Senate confirmed Kevin Warsh as the 17th Chair of the Federal Reserve by a 54–45 vote, drawing the curtain on Jerome Powell’s eight-year tenure.2 With a steady hand during an unsteady period, Powell navigated a once-in-a-century pandemic and the worst inflation in four decades, while upholding the central bank’s independence, raising rates 15 times and cutting them 11 times along the way. Few Fed chairs have been tested so severely; yet he leaves the institution as strong as he found it.

Warsh has inherited the position at a moment of considerable complexity, and China's latest pricing data may have been among the first things to land on his desk Monday morning. While President Trump's two-day summit with Xi Jinping in Beijing was declared "historic" by the Chinese leader, it produced warm words and a pledge to meet again in the autumn but fell short of any concrete deals or tangible breakthroughs.3

Beneath the diplomatic theatre, however, it was the economic data that carried the more lasting signal for the new Fed Chair. Chinese producer prices surged 2.8% year-on-year (YoY) in April, the fastest pace since the pandemic and a sharp acceleration from just 0.5% the prior month, as the Iran conflict drove energy and input costs higher across Chinese industry.4 The implications for the Fed Chair are that China, which has acted as a powerful disinflationary force on the global economy for a number of years, may be reversing that role. The world's factory is no longer exporting deflation. April’s US import prices report bear this out, surging to 1.9% month-on-month, driven by petroleum, but also with broad-based strength across non-fuel goods. Excess demand for AI hardware continued to push capital goods prices higher, and YoY gains in prices of imports from China turned positive for the first time since late 2022.5

The inflationary impact of the Middle East conflict was equally visible in domestic price data, which printed above consensus across the board. The Consumer Price Index rose 3.8% YoY, with gasoline prices surging almost 28% over the past two months alone.6 The pressure was not confined to energy; grocery prices, rents and airfares all posted significant increases, reflecting the broader pass-through of higher energy costs into the wider economy. Producer prices reinforced the picture, with input costs rising 1.4% in April, above an already upwardly revised prior reading of 0.7%, a signal that manufacturing inflation pressures remain firmly in motion. 7

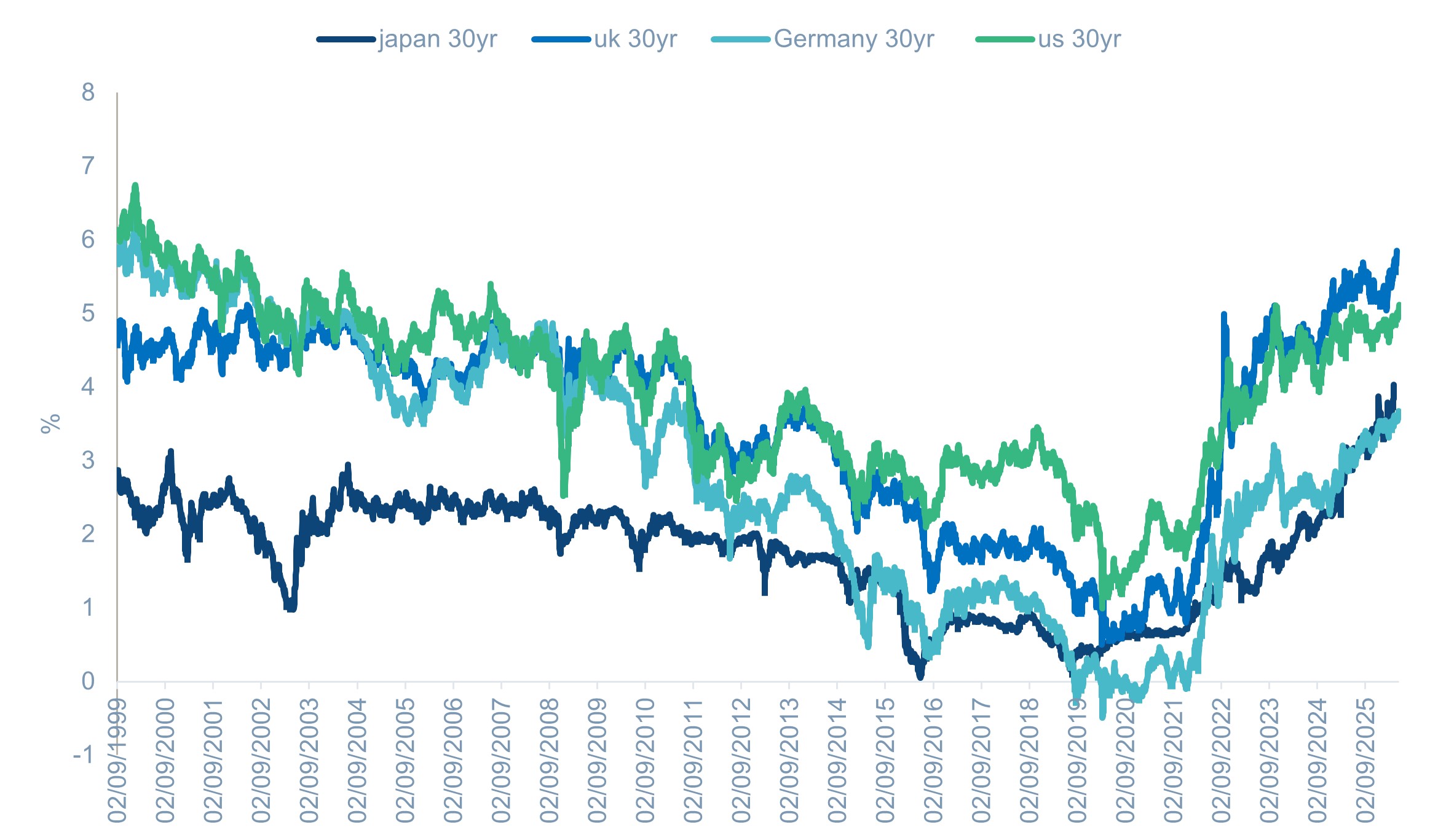

Across Europe, concerns over elevated energy costs pushed government bond yields higher, with UK gilts underperforming their European peers. Thirty-year gilt yields rose to levels not seen in a quarter of a century (see Chart of the Week). However, the energy price shock was only part of the story for the UK. Gilts are now facing an additional headwind from the domestic political front, after Labour's sweeping defeat to Reform UK in local elections deepened concerns about Keir Starmer's standing with voters and triggered an open contest for his leadership. Prediction markets currently price a 66% probability that Starmer will be replaced as Labour leader before the end of September,8 with Andy Burnham the current favourite to succeed him. Burnham's emergence as frontrunner has not been without its own complications; remarks he made last year suggesting the country was "in hock" to bond markets – which he has since insisted were taken out of context – nonetheless unsettled investors and added a further layer of uncertainty to an already unloved gilt market. 9

However, the unenviable distinction of the week’s worst-performing government bond market belonged to Japan, where the 30-year Japanese Government Bond (JGB) yield breached 4% for the first time since the bond’s debut in 1999. As elsewhere, yields were driven higher by growing concerns that rising energy prices may prove less than transitory. In Japan, however, reports that the government is considering a supplementary budget reignited longstanding concerns over fiscal discipline, compounding pressure on an already strained market.10 For a nation carrying one of the largest gross debt burdens in the developed world, rising yields are not merely a market inconvenience, they pose a direct threat to the sustainability of its public finances.

Chart of the Week: 30-yr government bond yields

Source: Bloomberg as of May 15, 2026. For illustrative purposes only.

Past performance is not a reliable indicator of current or future results.

References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

References

1. Bloomberg, as of May 15, 2016

2. Wall Street Journal, “Kevin Warsh Is Confirmed as Fed Chair in 54-45 Senate Vote,” May 13, 2026

3. Bloomberg, “Bolder Xi Moves to Corner Trump With ‘New Relationship’ Talk,” May 15, 2026

4. Bloomberg, “China’s Factory Inflation Hits Post-Covid High Amid War Shocks,” May 10, 2026

5. Bloomberg, “US INSIGHT: Import Prices Tip Goods-Inflation Risk From Abroad,” May 14, 2026

6. Bloomberg, “US Inflation Accelerates as Gas, Rent and Food Prices Climb,” May 12, 2026

7. Bloomberg, “US REACT: PPI at 6% Signals Higher Costs, But Cooler Core PCE,” May 13, 2026

8. Bloomberg, as of May 15, 2026

9. Bloomberg, “Gilts Slump as Investors Brace for Burnham Challenge to Starmer,” May 15, 2026

10. Bloomberg, “Japan Yields Rise to Record Highs on Global Inflation Fears,” May 15, 2026

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of 8th May 2026 and may change without notice.

--------

Important information

Muzinich & Co., “Muzinich” and/or the “Firm” referenced herein is defined as Muzinich & Co. Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Any forward-looking information or statements expressed in the above may prove to be incorrect. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Muzinich gives no undertaking that it shall update any of the information, data and opinions contained in the above.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

In the United Arab Emirates (UAE) (excluding the Dubai International Financial Centre (DIFC) and the Abu Dhabi Global Market (ADGM): This document, and the information contained herein, does not constitute, and is not intended to constitute, a public offer of securities in the United Arab Emirates (“UAE”) and accordingly should not be construed as such. The Units are only being offered to a limited number of exempt Professional Investors in the UAE who fall under one of the following categories: federal or local governments, government institutions and agencies, or companies wholly owned by any of them. The Units have not been approved by or licensed or registered with the UAE Central Bank, the SCA, the Dubai Financial Services Authority, the Financial Services Regulatory Authority or any other relevant licensing authorities or governmental agencies in the UAE (the “Authorities”). The Authorities assume no liability for any investment that the named addressee makes as a Professional Investor. The document is for the use of the named addressee only and should not be given or shown to any other person (other than employees, agents or consultants in connection with the addressee’s consideration thereof).

In the United Arab Emirates (UAE) (including the Dubai International Financial Centre and the Abu Dhabi Global Market): This information does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe for or purchase, any securities or investment products in the UAE and accordingly should not be construed as such. Furthermore, this information is being made available on the basis that the recipient is an entity fully regulated by the ADGM Financial Services Regulatory Authority (FSRA), and acknowledges and understands that the entities and securities to which it may relate have not been approved, licensed by or registered with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority, the Financial Services Regulatory Authority or any other relevant licensing authority or governmental agency in the UAE. The content of this report has not been approved by or filed with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority or the Financial Services Regulatory Authority.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-05-18-18512