EM monthly - The politics of credit

EM Monthly

June 12, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

Political headlines can be noisy, but institutional strength remains one of the most important drivers of sovereign creditworthiness. From Hungary and Colombia to Romania and Indonesia, political developments in 2026 are reshaping investment opportunities across emerging markets, with implications not only for sovereign bonds but also for the corporate issuers operating within them argues Warren Hyland.

Political headlines can move markets, but institutional strength remains one of the most important drivers of sovereign creditworthiness. For emerging market investors, understanding how political change influences governance, policymaking and reform is often key to identifying both risks and opportunities. Several developments in 2026 provide a timely reminder of why politics still matters for credit.

Institutions drive sovereign credit

"The most terrifying words in the English language are: I'm from the government and I'm here to help." — Ronald Reagan1

Reagan's quip endures because it captures something real - governments frequently disappoint. Yet for a sovereign credit analyst, the quality of a country's institutions is not merely relevant, it is foundational.

When analysing a sovereign’s creditworthiness and its long-term sustainability, five core pillars are commonly evaluated: institutional, economic, external, fiscal and monetary strengths. In our opinion institutional strength is frequently overlooked despite being arguably the most consequential driver of long-term credit wellbeing. It reflects the effectiveness, stability and predictability of public policymaking, the independence and resilience of political institutions and the degree of transparency, accountability and governance embedded within decision-making frameworks.

Sovereign credit analysis can best be characterised as a slow-moving discipline. Deterioration and improvement typically play out over decades. The worst-case outcome - default - carries humanitarian costs so severe that it is avoided at almost any price, with international bodies and regional institutions invariably stepping in to provide support before that threshold is reached.

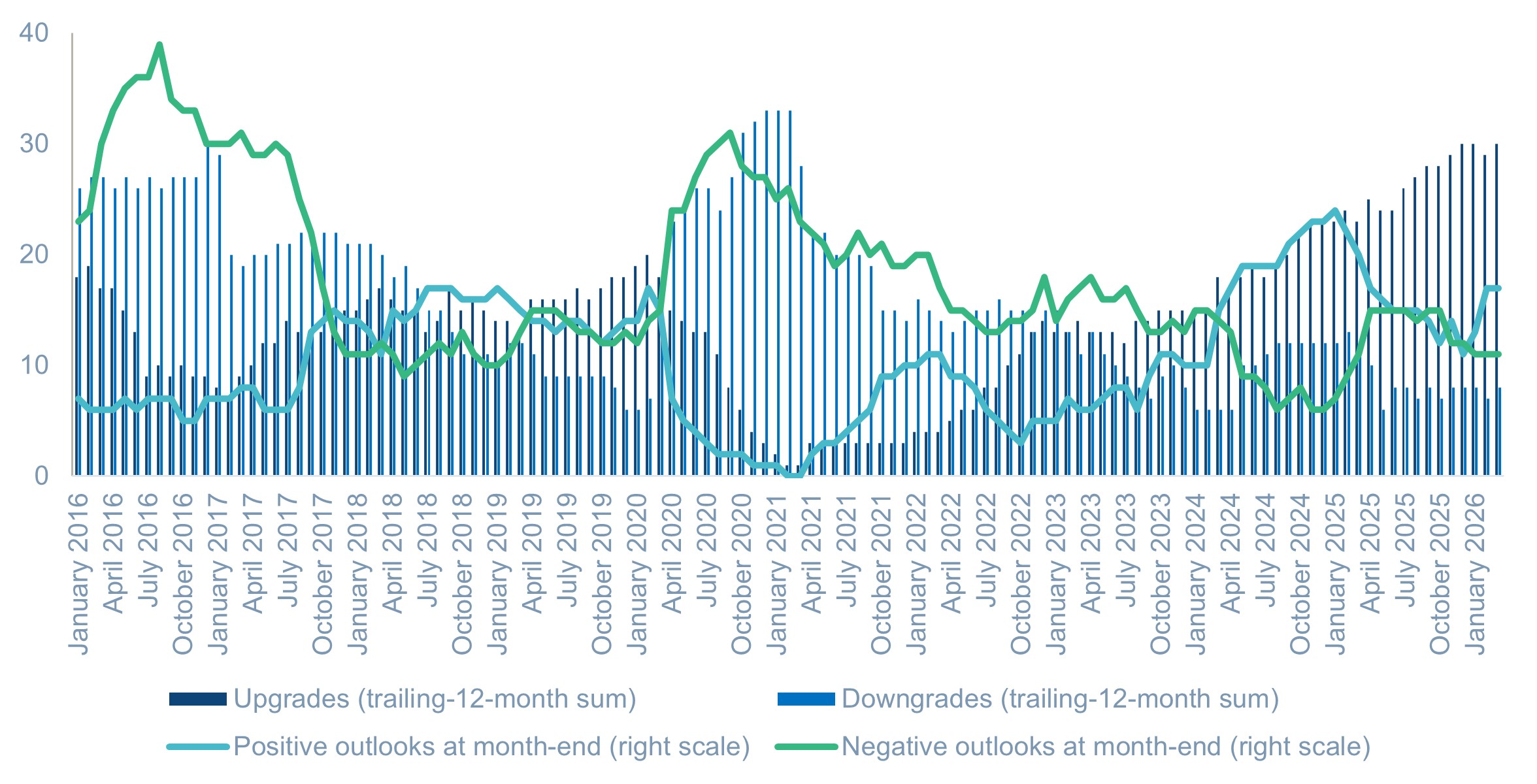

S&P Global currently maintains ratings on 142 sovereign governments, and its latest assessment presents a constructive backdrop for the asset class. Sovereign credit fundamentals have been on a broadly improving trajectory since the start of 2024. Over the past twelve months, ratings upgrades have substantially outpaced downgrades by a margin of 30 to 8, underscoring the breadth of the improvement across emerging and developed markets alike. The outlook distribution is similarly supportive, with 17 sovereigns carrying a positive outlook compared with 11 on a negative outlook, suggesting the balance of rating risk remains tilted toward further upgrades.2

Figure 1 - Sovereign foreign currency ratings – upgrades, downgrades and outlooks

Source; S&P Global, as of 2nd February 2026. Global sovereign rating trends 2026: geopolitical risks could destabilise credit quality dynamics. For illustrative purposes only.

Source; S&P Global, as of 2nd February 2026. Global sovereign rating trends 2026: geopolitical risks could destabilise credit quality dynamics. For illustrative purposes only.

When politics becomes a market catalyst

From a credit ratings perspective, sovereigns are typically grouped into three categories - investment grade, high yield and distressed - each with materially different implications for funding costs, market access and, most importantly, sensitivity to political developments. As sovereigns move down this credit spectrum, the dynamics become increasingly acute. The urgency and magnitude of market reactions intensify, while the transmission from political developments to pricing becomes progressively more immediate and pronounced.

At the same time, funding conditions deteriorate in a non-linear fashion, i.e., liquidity becomes scarcer as the pool of willing investors narrows. In parallel, the pressure for policy adjustment and reform typically rises as weaker credit profiles amplify the consequences of policy missteps. In effect, the transition from investment grade to high yield to distressed is not just a downgrade in credit quality, but a step-change response to political and institutional developments reflected in how investors price risk and allocate capital.

From our 2026 outlook, the emerging markets team identified two key political developments with cross-strategy implications.

Hungary’s return to Europe

The first is the end of 16 years of Fidesz-led governance under Viktor Orbán. A period characterised by persistent rule-of-law concerns and increasingly autocratic tendencies. The outcome, however, exceeded even our expectations. In Hungary's April 2026 election, the centrist, pro-EU Tisza party led by Péter Magyar secured a decisive victory, winning 141 out of 199 parliamentary seats – an outright constitutional supermajority.3

The most immediate and consequential near-term implication is the potential unlocking of approximately €17 -18bn in suspended EU funding, withheld since 2022 under rule-of-law conditionality.4 This comprises around €10bn under the Recovery and Resilience Facility and €7bn in cohesion funds, together equivalent to roughly 9% of GDP.4 A further €16-17bn in EU SAFE defence-related loans remains in the pipeline, though disbursement is contingent on progress against 27 outstanding "super milestones" covering judicial independence, anti-corruption safeguards, and broader rule-of-law reform.5

The new government has already signalled a meaningful recalibration in its EU posture, including commitments to lift Hungary's veto on the €90bn EU loan package for Ukraine and to withdraw opposition to further Russia sanctions. We expect material inflows from Brussels to resume in late 2026 to early 2027.

Over the medium term, euro adoption is realisable, and we consider it a structural theme for strategies. Accession to the eurozone featured in Tisza's February manifesto, and the newly secured constitutional majority makes the legal pathway materially more feasible. Incoming Finance Minister András Kármán has indicated Hungary could potentially meet the Maastricht criteria by 2030, a timeline underpinned by notably strong public support, with approximately 72% of Hungarians in favour.6

Latin America's market-friendly turn

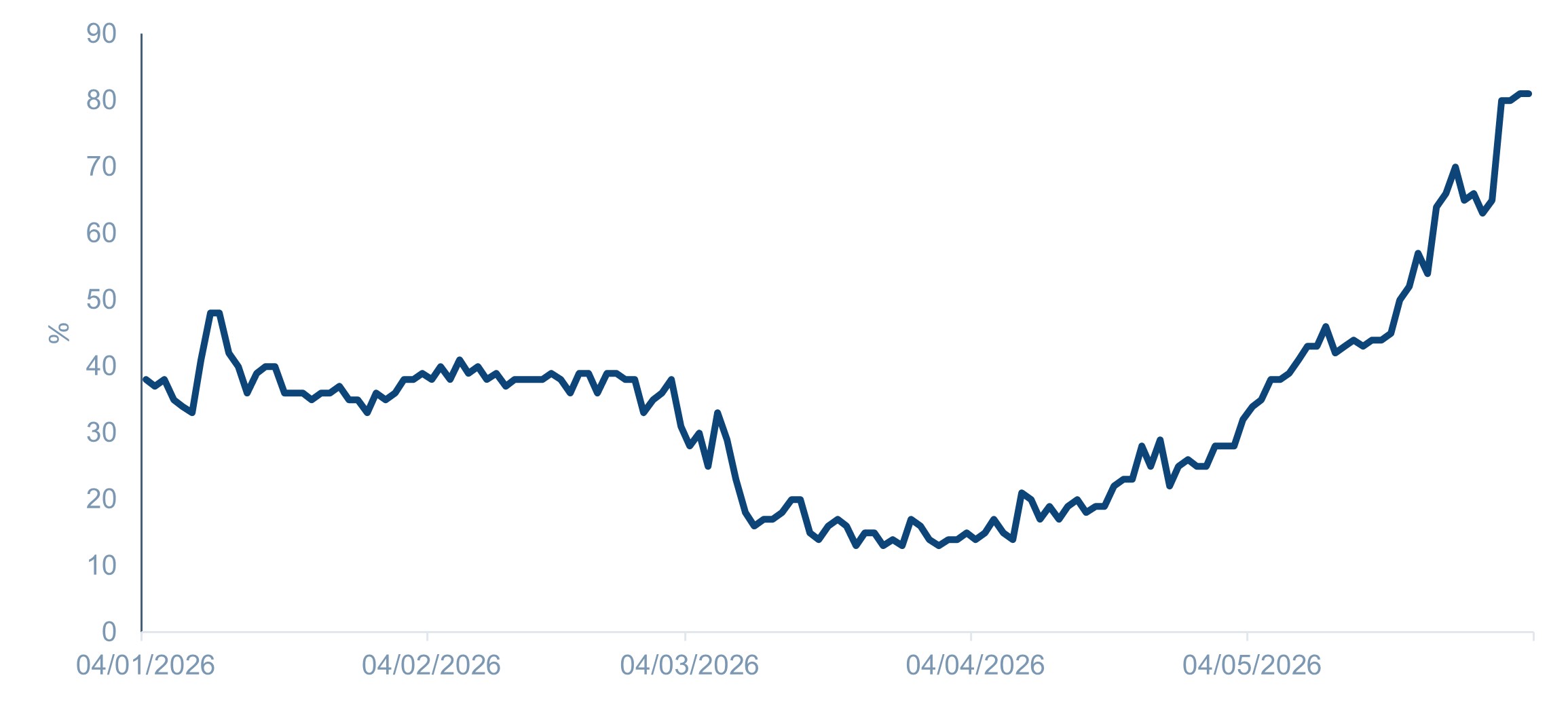

Our second theme was Latin America's continued rightward shift in 2026 - a discernible political realignment toward market-friendly, orthodox, right-of-centre governance. The trend, established in Argentina, Ecuador and Chile, has now extended to Colombia, and did so in striking fashion. Most opinion polls had pointed to a first-round victory for Iván Cepeda, yet with all ballots counted, right-wing outsider Abelardo de la Espriella secured 43.74% of the vote against Cepeda's 40.90%, while centre-right candidate Paloma Valencia finished a distant third on 6.9%.7 A runoff is set for June 21st, with prediction markets currently pricing an 81% probability that de la Espriella will prevail (Figure 2).

Figure 2 – Predictions for Colombia’s de la Espriella to win presidential election

Source: Bloomberg, Colombia Polymarket predication market, as of 3rd June 2026. For illustrative purposes only.

Source: Bloomberg, Colombia Polymarket predication market, as of 3rd June 2026. For illustrative purposes only.

The implications for the sovereign are significant. Under the Petro administration, Colombia was downgraded twice by S&P Global, from BB+ to BB-, as persistently large fiscal deficits and their associated consequences eroded creditworthiness.8 De la Estrella’s platform represents a sharp break from that trajectory campaigning for roughly 3% of GDP in fiscal consolidation over four years, with a heavy focused on expenditure cuts, deregulation of oil & gas and construction and IMF engagement.9

The regional rightward shift may also extend to Peru, where the presidential runoff on June 7th pitted right-wing Keiko Fujimori against left-wing Roberto Sánchez. The race is competitive, and at time of publishing Fujimori led with 50.2% to Sánchez’s 49.7% with 92% of ballots counted.10

Romania: uncertainty versus valuation

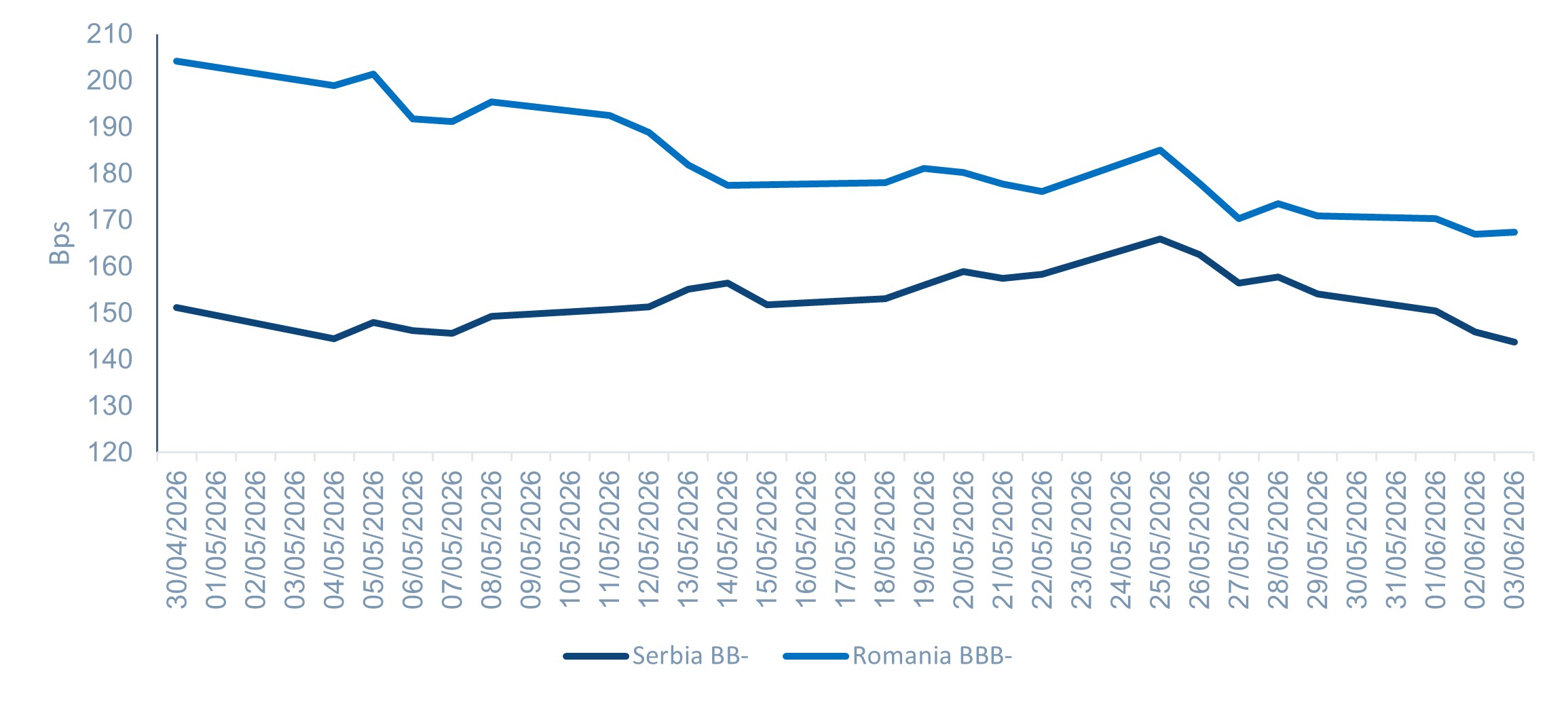

As for what has surprised us so far in 2026 , the Romanian parliament passing a no-confidence vote on 5th May 2026, toppling the PNL-led government after the PSD withdrew from the coalition, the seventh such vote since 2009, (maybe we shouldn't have been surprised).11 Indeed, history offered a reassuring precedent that in all six prior episodes, early elections were averted and a new coalition emerged, typically within 8 to 71 days.12

The key question is what coalition comes next. In a PNL- led coalition scenario, where 2026 fiscal commitments are largely maintained, we would expect rating agencies to keep Romania's rating unchanged. By contrast, a PSD-led government implying meaningful fiscal loosening raises the risk of a downgrade in 2027. That said, current market pricing for Romanian sovereign risk appears to have already fully discounted this outcome, the downgrade scenario, in our view. On that basis, we maintain our existing positioning, seeing limited incremental downside and recognising that any positive surprise on the political front could represent a catalyst for spread compression (Figure 3).

Figure 3: Romania and Serbian BB-BBB 5 year Z spread

Source: Bloomberg, as of 3rd June 2026. Romania BBB-: Romania Sovereign (BCLASS), Republic of Serbia Sovereign (BCLASS). For illustrative purposes only.

Source: Bloomberg, as of 3rd June 2026. Romania BBB-: Romania Sovereign (BCLASS), Republic of Serbia Sovereign (BCLASS). For illustrative purposes only.

Indonesia: a governance warning sign

As for what has disappointed us so far in 2026, it has been Indonesia’s gradual erosion of institutional credibility under President Prabowo Subianto. Investor concerns are increasingly centred not on traditional macroeconomic metrics, but on the quality of policymaking, predictability and governance. In particular, the administration’s rhetoric around economic self-sufficiency, state-directed pricing and a more interventionist role for the state has raised questions about the future policy framework.

The most significant development has been President Prabowo’s proposal to centralise control over Indonesia’s key commodity exports - including palm oil, coal and ferro-alloys - through a new state entity, Danantara Sumberdaya Indonesia (DSI).13 For markets, the concern is less the immediate economic impact than the signal it sends regarding the direction of travel for economic governance and state involvement in resource allocation.

These concerns are compounded by the growing risk that Indonesia could be downgraded by MSCI from Emerging to Frontier Market status. We believe Indonesia’s equity market continues to suffer from relatively low institutional participation, concentrated ownership structures and limited liquidity.

Fiscal pressures are also beginning to build. Elevated oil prices make the government's ability to maintain fuel price caps, while keeping the fiscal deficit within its long-standing 3% of GDP, increasingly challenging. Although fiscal metrics remain broadly manageable, the margin for policy flexibility has narrowed.

Overall, the direction of travel is negative. Indonesia remains some distance from a sovereign downgrade, and a ratings action would likely require clearer evidence of fiscal slippage, sustained capital outflows, or a material deterioration in macroeconomic fundamentals. However, institutional indicators, which are often leading rather than lagging measures of credit quality, are moving in the wrong direction. We have reduced exposure across our EM strategies accordingly.

Politics matters because institutions matter

The events of 2026 reinforce a simple but often overlooked point: politics matters because institutions matter.

Whether it is Hungary's potential reintegration with the European Union, Colombia's evolving fiscal trajectory, Romania's political uncertainty or Indonesia's institutional challenges, the common thread is the role of governance in shaping long-term credit outcomes. Markets may focus on elections and headlines, but investors ultimately assess whether political developments strengthen or weaken the institutional foundations that support sustainable growth and creditworthiness.

For emerging market debt investors, understanding these dynamics remains essential. Sovereign credit trends frequently influence broader financing conditions, investor sentiment and capital flows, creating ripple effects across domestic corporate bond markets. In many cases, the same institutional improvements that support sovereign spreads can also enhance the outlook for fundamentally strong corporate issuers.

As a result, political analysis is an important component of identifying opportunities across the wider EM credit universe. For investors in EM corporates, a deep understanding of sovereign and institutional developments can provide valuable context for assessing risk, identifying mispriced opportunities and navigating an increasingly complex global environment.

EM look back – May

Past performance is not a reliable indicator of current or future results.

Market Data

Credit

Past performance is not a reliable indicator of current or future results.

Past performance is not a reliable indicator of current or future results.

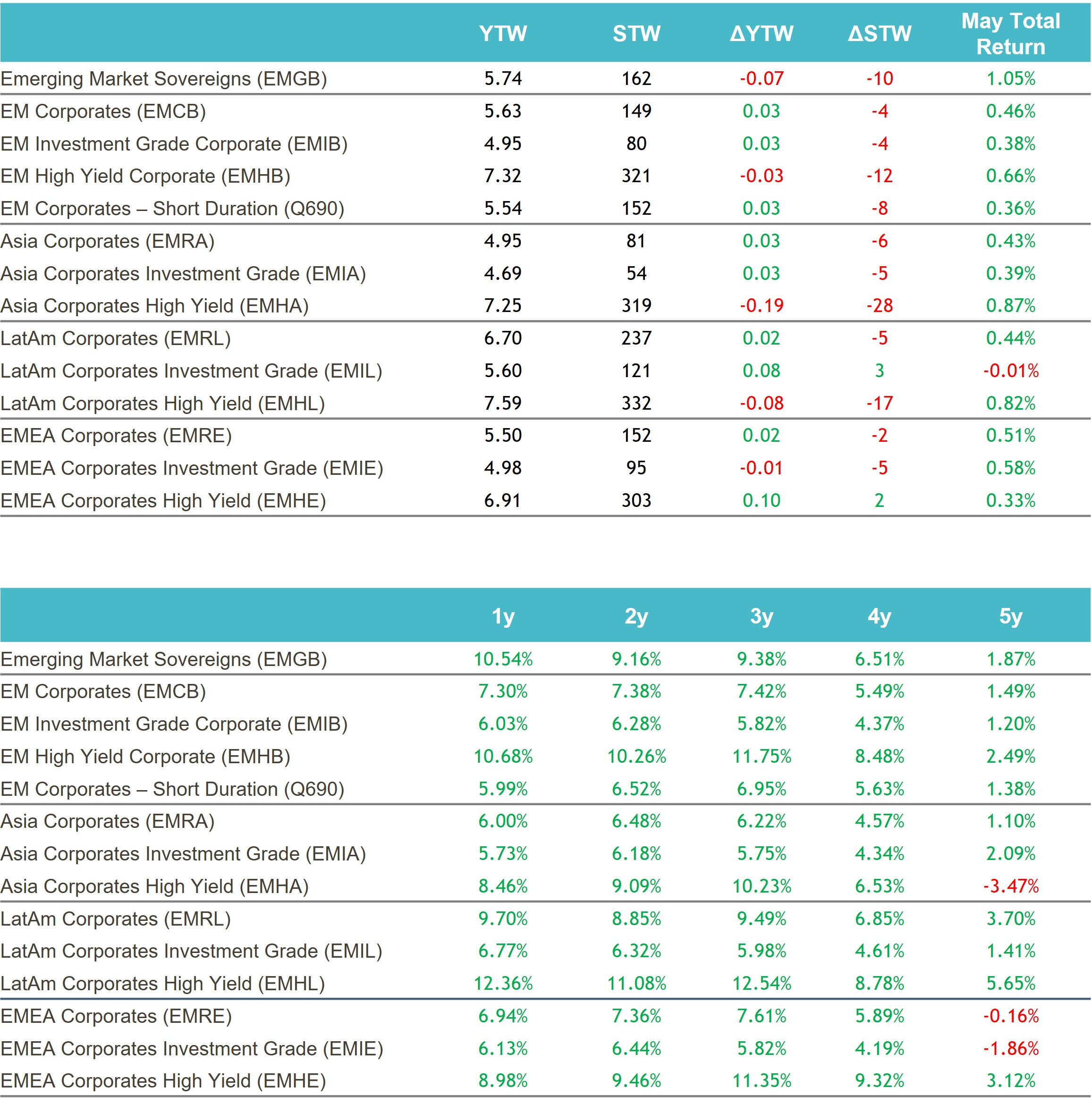

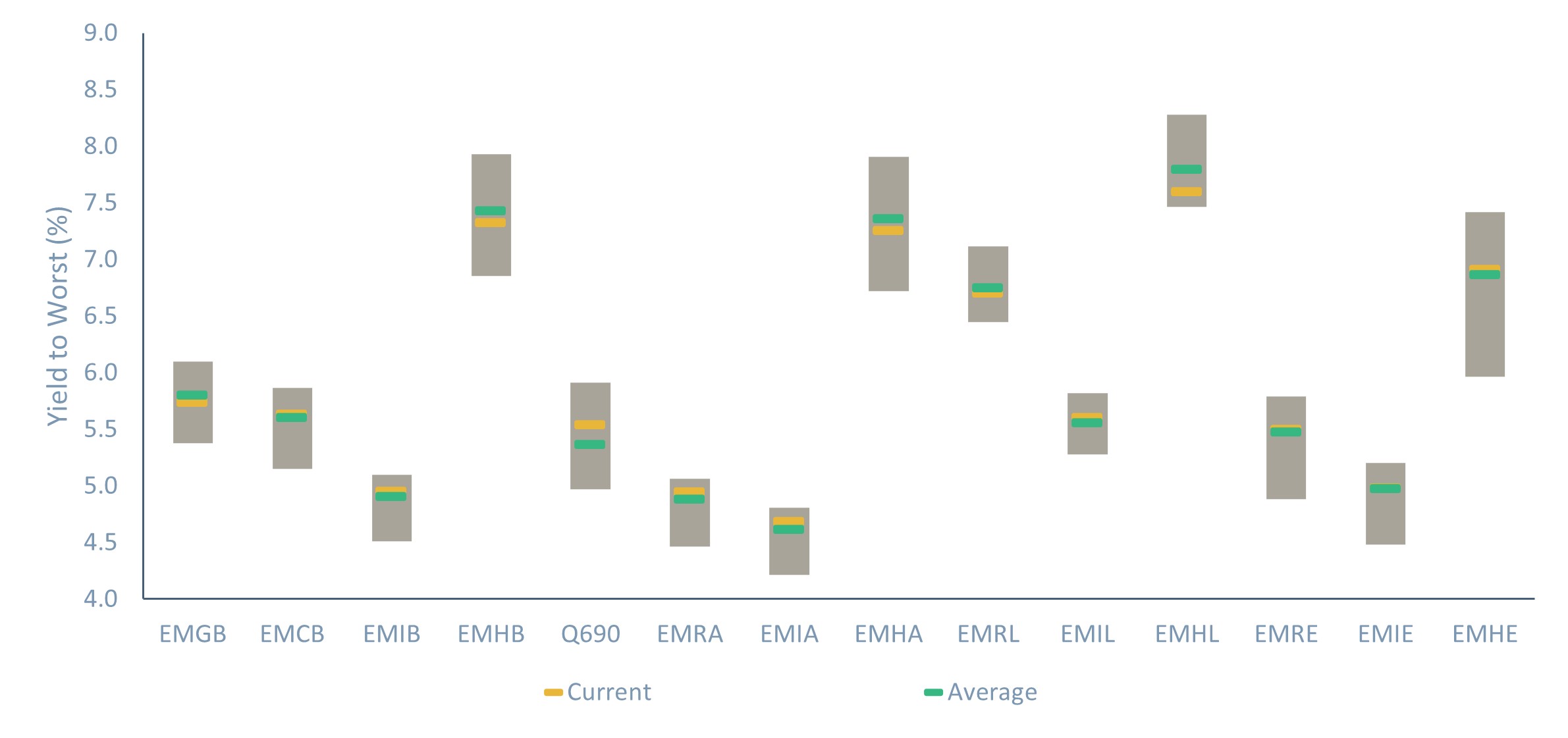

Source: ICE data platform. as of 31st May 2026. EMGB - ICE BofA Emerging Markets External Sovereign Index EMCB - ICE BofA Emerging Markets Corporate Plus Index, EMIB - ICE BofA High Grade Emerging Markets Corporate Plus Index, EMHB - ICE BofA High Yield Emerging Markets Corporate Plus Index, Q690 - ICE BofA Custom Emerging Markets Short Duration Index, EMRA - ICE BofA Asia Emerging Markets Corporate Plus Index, EMIA - ICE BofA High Grade Asia Emerging Markets Corporate Plus Index, EMHA - ICE BofA High Yield Asia Emerging Markets Corporate Plus Index , EMRL - ICE BofA Latin America Emerging Markets Corporate Plus Index, EMIL - The ICE BofA High Grade Latin America Emerging Markets Corporate Index, EMHL - ICE BofA High Yield Latin America Emerging Markets Corporate Plus, EMRE - ICE BofA EMEA Emerging Markets Corporate Plus Index, EMIE - ICE BofA High Grade EMEA Emerging Markets Corporate Plus Index, EMHE - ICE BofA High Yield EMEA Emerging Markets Corporate Plus Index,. Index performance is for illustrative purposes only. You cannot invest directly in the index. Indices selected provide best proxy for highlighting performance of emerging market corporate bonds. For illustrative purposes only.

Yield to Worst

Source: ICE data platform. as of 31st May 2026. EMGB - ICE BofA Emerging Markets External Sovereign Index EMCB - ICE BofA Emerging Markets Corporate Plus Index, EMIB - ICE BofA High Grade Emerging Markets Corporate Plus Index, EMHB - ICE BofA High Yield Emerging Markets Corporate Plus Index, Q690 - ICE BofA Custom Emerging Markets Short Duration Index, EMRA - ICE BofA Asia Emerging Markets Corporate Plus Index, EMIA - ICE BofA High Grade Asia Emerging Markets Corporate Plus Index, EMHA - ICE BofA High Yield Asia Emerging Markets Corporate Plus Index , EMRL - ICE BofA Latin America Emerging Markets Corporate Plus Index, EMIL - The ICE BofA High Grade Latin America Emerging Markets Corporate Index, EMHL - ICE BofA High Yield Latin America Emerging Markets Corporate Plus, EMRE - ICE BofA EMEA Emerging Markets Corporate Plus Index, EMIE - ICE BofA High Grade EMEA Emerging Markets Corporate Plus Index, EMHE - ICE BofA High Yield EMEA Emerging Markets Corporate Plus Index,. Index performance is for illustrative purposes only. You cannot invest directly in the index. Indices selected provide best proxy for highlighting performance of emerging market corporate bonds. For illustrative purposes only.

Source: ICE data platform. as of 31st May 2026. EMGB - ICE BofA Emerging Markets External Sovereign Index EMCB - ICE BofA Emerging Markets Corporate Plus Index, EMIB - ICE BofA High Grade Emerging Markets Corporate Plus Index, EMHB - ICE BofA High Yield Emerging Markets Corporate Plus Index, Q690 - ICE BofA Custom Emerging Markets Short Duration Index, EMRA - ICE BofA Asia Emerging Markets Corporate Plus Index, EMIA - ICE BofA High Grade Asia Emerging Markets Corporate Plus Index, EMHA - ICE BofA High Yield Asia Emerging Markets Corporate Plus Index , EMRL - ICE BofA Latin America Emerging Markets Corporate Plus Index, EMIL - The ICE BofA High Grade Latin America Emerging Markets Corporate Index, EMHL - ICE BofA High Yield Latin America Emerging Markets Corporate Plus, EMRE - ICE BofA EMEA Emerging Markets Corporate Plus Index, EMIE - ICE BofA High Grade EMEA Emerging Markets Corporate Plus Index, EMHE - ICE BofA High Yield EMEA Emerging Markets Corporate Plus Index,. Index performance is for illustrative purposes only. You cannot invest directly in the index. Indices selected provide best proxy for highlighting performance of emerging market corporate bonds. For illustrative purposes only.

References

1. Ronald Reagan Presidential Library and Museum, as of 12th August 1986. The Present’s News Conference.

2. S&P Global, as of 2nd February 2026. Global sovereign rating trends 2026: geopolitical risks could destabilise credit quality dynamics.

3. BBC News, as of 9th May 2026 “I will serve - not rule over Hungary, says new PM”

4. CEPS EU, as of 24th April 2026. Orban’s defeat opens the door to EU funds and to smarter rule of law conditionality.

5. Hungarian Helsinki Committee, as of 18th January 2026. Missed opportunities; suspended union funds for Hungary.

6. Reuters, as of 12th May 2016. Hungary PM Magya targets new economic model, gives key ministers veto over legislation. 7. AS/COA, as of 4th June 2026. Poll Tracker: Colombia’s 2026 presidential election.

8. S&P Global, as of 8th April 2026. Colombia Long-Term foreign currency rating lowered to ‘BB-‘ from ‘BB’ to fiscal imbalances; outlook stable.

9. Bloomberg, as of 2nd June 2026. The market is readjusting its bets and sees a victory for De la Espriella in Colombia as more likely.

10. Bloomberg, as of 8th June 2026. “Peru vote too close to call as Fujimori’s lead narrows”.

11. Reuters, as of 5th May 2026. Romanian government collapses after no-confidence vote.

12.Coalition governments in Western Europe, Oxford University Press, as of 4th June 2026

13. Reuters, as of 2nd June 2026. Indonesian business groups call for clarity about new commodity export rules.

All sources are Bloomberg unless otherwise stated.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of June 2026 and may change without notice.

--------

Index descriptions

EMGB - ICE BofA Emerging Markets External Sovereign Index tracks the performance of US dollar and euro denominated emerging markets sovereign debt publicly issued in the major domestic and eurobond markets. Qualifying securities must have risk exposure to countries other than members of the FX-G10, all Western European countries and territories of the US and Western European countries.

EMCB - ICE BofA Emerging Markets Corporate Plus Index tracks the performance of the US dollar and euro denominated emerging markets non-sovereign debt publicly issued in the major domestic and eurobond markets. Qualifying issuers must have risk exposure to countries other than members of the FX G10, all Western European countries, and territories of the US and Western European countries.

EMIB - ICE BofA High Grade Emerging Markets Corporate Plus Index is a subset of the ICE BofA ML Emerging Markets Corporate Plus Index (EMCB) including all securities rated AAA through BBB3, inclusive.

EMHB - ICE BofA High Yield Emerging Markets Corporate Plus Index is a subset of the ICE BofA ML Emerging Markets Corporate Plus Index (EMCB) including all securities rated BB1 or lower.

Q690 - ICE BofA Custom Emerging Markets Short Duration Index tracks the performance of short-term US dollar and euro denominated emerging markets non-sovereign debt publicly issued in the major domestic and eurobond markets.

EMRA - ICE BofA Asia Emerging Markets Corporate Plus Index is the subset of the ICE BofAML Emerging Markets Corporate Plus Index, which includes only securities issued by countries associated with the region of Asia, excluding Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan, and Uzbekistan.

EMHA – The ICE BofA High Yield Asia Emerging Markets Corporate Plus Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BB1 and lower with a country of risk within the Asia region.

EMIA - The ICE BofA High Grade Asia Emerging Markets Corporate Plus Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BBB3 and higher with a country of risk within the Asia region.

EMRL - ICE BofA Latin America Emerging Markets Corporate Plus Index is a subset of The ICE BofA Emerging Markets Corporate Plus Index including all securities issued by countries associated with the geographical region of Latin America.

EMIL - The ICE BofA High Grade Latin America Emerging Markets Corporate Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BBB3 and higher with a country of risk within the Latin America region.

EMHL - ICE BofA High Yield Latin America Emerging Markets Corporate Plus is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated sub-investment grade based on the average of Moody's, S&P and Fitch, and with a country of risk associated with the geographical region of Latin America.

EMRE - ICE BofA EMEA Emerging Markets Corporate Plus Index is a subset of The ICE BofA Emerging Markets Corporate Plus Index including all securities issued by countries associated with the geographical region of Europe, the Middle East and Africa including Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan and Uzbekistan.

EMIE - ICE BofA High Grade EMEA Emerging Markets Corporate Plus Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BBB3 and higher with a country of risk within the Europe, Middle East and Africa regions.

EMHE - ICE BofA High Yield EMEA Emerging Markets Corporate Plus Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BBB3 and higher with a country of risk within the Europe, Middle East and Africa regions.

The MSCI EM Index is a free-float weighted equity index that captures large and mid cap representation across emerging market countries. The index covers approximately 85% of the free float-adjusted market capitalisation in each country.

LDMP - ICE BofA Local Debt Markets Plus Index is designed to track the performance of emerging markets sovereign debt publicly issued and denominated in the issuer's own currency.

J0A0 - The ICE BofA ML US Cash Pay High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt, currently in a coupon paying period that is publicly issued in the US domestic market.

J0A1 – The ICE BofA BB US Cash Pay High Yield Index is a subset of the ICE BofA US Cash Pay High Yield Index (J0A0) including all securities rated BB1 through BB3, inclusive.

C0C0A0 - The ICE BofA ML US Corporate Index tracks the performance of US dollar denominated investment grade corporate debt publicly issued in the US domestic market.

HE00 - The ICE BofA ML Euro High Yield Index tracks the performance of EUR dominated below investment grade corporate debt publicly issued in the euro domestic or eurobond markets.

ER00 – The ICE BofA ML Euro Corporate Index tracks the performance of EUR denominated investment grade corporate debt publicly issued in the eurobond or Euro member domestic markets.

ICE BofA High Yield Emerging Markets Corporate Plus India Issuers Index (EINH) - is a subset of ICE BofA Emerging Markets Corporate Plus Index

ADHY - ICE BofA Asian Dollar High Yield Index tracks the performance of sub-investment grade U.S. dollar denominated sovereign, quasi-government, corporate, securitized and collateralized debt publicly issued in the U.S. domestic and eurobond markets by Asian issuers.

ICE BofA BB Asian Dollar High Yield Index (ACH1) ICE BofA BB Asian Dollar High Yield Index is a subset of ICE BofA Asian Dollar High Yield Corporate Index including all securities rated BB1 through BB3, inclusive.

ADIG - ICE BofA Asian Dollar Investment Grade Index tracks the performance of investment grade U.S. dollar denominated sovereign, quasi-government, corporate, securitized and collateralized debt publicly issued in the U.S. domestic and eurobond markets by Asian issuers. Qualifying securities have a country of risk classified as an Emerging Markets country that is part of the Asia/Pacific Region.

CEMBI Broad Div. Index - The JP Morgan CEMBI Broad Diversified Index (CEMBIB Div) is a benchmark that tracks the performance of US dollar-denominated, fixed and floating-rate debt instruments issued by emerging market corporate entities.

JESG CEMBI Broad Div. Index - The JP Morgan ESG CEMBI Broad Diversified Custom Maturity Index tracks liquid, US Dollar denominated emerging market fixed and floating-rate debt instruments issued by corporates.

EM3B – ICE BofA BB Emerging Markets Corporate Plus Index is a subset of the ICE BofA Emerging Markets Corporate Plus Index including ass securities rated BB1 through BB3, inclusive.

EMCS – ICE BofA Emerging Markets Corporate Plus Consumer Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities of Consumer Cyclical and Consumer Non-Cyclical issuers.

EMEN – ICE BofA Emerging Market Corporate Plus Energy Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities of Energy issuers.

EMRB – ICE BofA Emerging Market Corporate plus Real Estate, Building & Hotels Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities of Real Easte, Building & Construction, or Hotels.

EMCG – ICE BofA Emerging Markets Corporate Plus Capital Goods Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities of Capital Goods Issuers.

EMSD – ICE BofA Emerging Markets Diversified Corporate Index tracks the performance of USD dollar denominated emerging markets corporate senior and secured debt publicly issued in the US domestic and eurobond markets.

EMTM – ICE BofA Emerging Markets Corporate Plus Media & Telecommunications Index is a subset of ICE BofA Emerging Markets Corporate Plus index including all securities of media and telecommunications issuers.

EM2B – ICE BofA BBB Emerging Markets Corporate Plus Index is a subset of the ICE BofA Emerging Market Corporate Plus index including all securities rated BBB1 through BBB3, inclusive.

EMUT – the ICE BofA Emerging Markets Corporate Plus Utility Index is a subset of the ICE BofA Emerging Markets Corporate Plus Index including all securities of Utility issuers.

EMPB – ICE BofA Public Sector Issuers Emerging Markets Corporate Plus Index is a subset of The BofA Emerging Markets Corporate Plus Index including all quasi-government securities as well as debt of corporate issuers deemed to be government owned or controlled.

ACIG – ICE BofA Asian Dollar Investment Grade Corporate Index tracks the performance of investment grade US dollar denominated securities issued by Asian corporate issuers in the US domestic and eurobonds market. Qualyfying securities have a country of risk associated with Bangladesh, Bhutan, Cambodia, China, John Kong, India, Indonesia, Laos, Macau, Malaysia, Mongolia, Myanmar, Nepal, Pakistan, Papua New Guinea, Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Thailand and Vietnam.

EMAB – Ice BofA Automotive & Basic Industry Emerging Markets Corporate Plus Index is a subset of the ICE BofA Emerging Markets Corporate Plus Index.

EMHE - The ICE BofA High Yield EMEA Emerging Markets Corporate Plus Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BBB3 and higher with a country of risk within the Europe, Middle East and Africa regions.

EMNS – The ICE BofA Non-Financial Emerging Markets Corporate Plus Index is a subset of the ICE BofA Emerging Markets Corporate Plus Index excluding all financial securities as well as debt of corporate issuers designated as government owned or controlled by ICE BofA emerging markets credit research.

EM1B – the ICE BofA AAA-A Emerging Markets Corporate Plus Index is a subset of the ICE BofA Emerging Market Corporate Plus Index including all securities rated AAA through A3, inclusive.

including all securities with India as the country of risk that are rated sub-investment grade based on average of Moody's, S&P and Fitch

ADOL -The ICE BofA Asian Dollar Index tracks the performance of U.S. dollar denominated sovereign, quasi-government, corporate, securitized and collateralized debt publicly issued in the U.S. domestic and eurobond markets by Asian issuers.

ICE BofA China Corporate Index (CN0C) ICE BofA China Corporate Index tracks the performance of CNY denominated corporate debt issued in the Chinese domestic bond market. Qualifying securities must have at least one year remaining term to final maturity, at least 18 months to final maturity at point of issuance, a fixed coupon schedule and a minimum amount outstanding of CNY 500 million. Callable perpetual securities qualify provided they are at least one year from the first call date. Fixed-to-floating rate securities also qualify provided they are callable within the fixed rate period and are at least one year from the last call prior to the date the bond transitions from a fixed to a floating rate security. Contingent capital securities (“cocos”) are excluded, but capital securities where conversion can be mandated by a regulatory authority, but which have no specified trigger, are included. Other hybrid capital securities, such as those issues that potentially convert into preference shares, those with both cumulative and non-cumulative coupon deferral provisions, and those with alternative coupon satisfaction mechanisms, are also included in the index. Securities in legal default are excluded from the Index.

ICE BofA Investment Grade Emerging Markets Corporate Plus China Issuers Index (ECNI) ICE BofA Investment Grade Emerging Markets Corporate Plus China Issuers Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities with China as the country of risk that are rated investment grade based on average of Moody's, S&P and Fitch. EMFN – EM Corporate Plus Financial is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities of financial issuers.

EMIE - The ICE BofA High Grade EMEA Emerging Markets Corporate Plus Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BBB3 and higher with a country of risk within the Europe, Middle East and Africa regions.

EM4B – ICE BofA B & Lower Emerging Markets Corporate Plus Index is a subset of the ICE BofA Emerging Markets Corporate Plus Index.

EMRT – ICE BofA Emerging Markets Corporate Plus Transportation Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities of Transportation issuers other than airlines or railroads.

GSFCI - The Goldman Sachs Financial Conditions Index is a measure that assesses the overall financial conditions in the economy, taking into account various factors such as interest rates, credit spreads, and equity prices.

ICE BofA B Asian Dollar High Yield Index (ACH2) ICE BofA B Asian Dollar High Yield Index is a subset of ICE BofA Asian Dollar High Yield Corporate Index including all securities rated B1 through B3, inclusive.

ICE BofA Single-B US Cash Pay High Yield Index (J0A2) ICE BofA Single-B US Cash Pay High Yield Index is a subset of ICE BofA US Cash Pay High Yield Index including all securities rated B1 through B3, inclusive.

You cannot invest directly in an index, which also does not take into account trading commissions or costs. Additionally, indices do not include reinvestment of dividends, and the volatility of indices may be materially different over time.

-------

Important information

Muzinich and/or Muzinich & Co. referenced herein is defined as Muzinich & Co., Inc. and its affiliates. Muzinich views and opinions. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall.

Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only.

This discussion material contains forward-looking statements, which give current expectations of future activities and future performance. Any or all forward-looking statements in this material may turn out to be incorrect. They can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Although the assumptions underlying the forward-looking statements contained herein are believed to be reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurances that the forward-looking statements included in this discussion material will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Further, no person undertakes any obligation to revise such forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

United Arab Emirates (UAE): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the UAE. It is intended solely for Professional Investors and should not be relied upon by any other person. This material has not been reviewed or approved by the UAE Securities and Commodities Authority, the UAE Central Bank or any other relevant authority. Nothing contained herein constitutes investment, legal, tax or other professional advice. Recipients should make their own independent assessment where appropriate.

Abu Dhabi Global Market (ADGM): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the ADGM. It is intended solely for Professional Clients (as defined by the Financial Services Regulatory Authority) and should not be relied upon by any other person. This material has not been reviewed or approved by the Financial Services Regulatory Authority or any other relevant authority in the UAE.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-06-09-18688

By clicking "Submit", I am (i) signing up to receive the Opinion Pieces from the "Opinions" page of the Muzinich & Co website, (ii) representing that the above information is true and accurate and (iii) agreeing to join the Muzinich & Co mailing list. I understand that Muzinich & Co will not add retail investors or individuals with personal email addresses to its mailing list and represent that I am not a retail investor. By providing my personal and professional information I am consenting to its use and disclosure in accordance with the Muzinich & Co. Privacy Policy. I understand that I may withdraw my consent and unsubscribe from receiving future communications by clicking "Unsubscribe" from the emails that are sent to me from Muzinich & Co.