Muzinich Weekly Market Comment: On the starting blocks

Insight

May 5, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

As conflict-driven energy shocks ripple through economies, the world’s leading central banks remain on the starting blocks – poised but cautious, holding rates steady as they await clearer signals. Credit markets, by contrast, have already sprung into motion, proving resilient and closely tracking their usual seasonal patterns.

The US and Israel launched joint military strikes on Iran on 28th February 2026, meaning the 60-day threshold under the War Powers Resolution of 1973 has now passed. While this does not automatically bring military action to a halt, it does mean the President is legally required either to obtain Congressional authorization or to terminate the use of US armed forces in those hostilities.1 The administration has also moved well beyond the eight-week timeframe it had repeatedly cited as its objective.

As matters stand, the stalemate is deepening, with US and Iranian leaders each seemingly waiting for the other to blink first, even as the political and financial costs rise in the US and the economic fallout spreads globally. Against this volatile backdrop, it was a fascinating week for investors as ten central banks under our watch held policy meetings, including the “Big Four”: the Bank of England (BoE), Bank of Japan (BoJ), European Central Bank (ECB) and the Federal Reserve (Fed).

In Asia, the BoJ left policy unchanged at 0.75% for a third consecutive meeting, with the decision passing by a 6–3 vote, the first split since Kazuo Ueda took office. For fiscal year 2026, the BoJ sharply cut its GDP forecast to 0.5% from 1.0%, while raising its core Consumer Price Index (CPI) projection to 2.8%. The revisions reflect higher oil prices and their impact in squeezing corporate profits and household incomes. Governor Ueda said confidence in the central bank’s forecasts had “declined quite significantly,” leaving the door open to an extended pause, while cautioning that energy-driven cost pressures could still push underlying inflation above the 2% target.2

In Europe, the UK Monetary Policy Committee (MPC) left the Bank Rate unchanged at 3.75% at its April meeting. The vote split was 8–1. The Committee’s collective guidance was unchanged, stating that it “stands ready to act as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term”.3

The MPC outlined three scenarios. In Scenario 1, energy prices follow futures curves and there are no second-round effects; inflation peaks at 3.6% in Q4 2026 (March’s reading was 3.3%), before easing back toward target. Scenario 2 assumes modest second-round effects; inflation peaks at 3.7% in 2026 but is then projected to return to 2% over the two-to three-year horizon. Scenario 3 assumes energy prices remain elevated for a prolonged period; inflation peaks at 6.2% in Q1 2027 and stays above target throughout the forecast period. Governor Andrew Bailey appeared to hedge between the first two scenarios, saying the Committee placed “most weight on Scenario B, albeit with slightly reduced second-round effects”.3

The ECB followed suit, leaving its deposit rate unchanged at 2%, where it has sat since June 2025, signalling that June would be the appropriate moment to assess the conflict's impact on the eurozone, coinciding with the quarterly update to its economic projections. "We made an informed decision on the basis of yet insufficient information," President Lagarde said, acknowledging that the Governing Council had debated not only the hold but also, "at length, and in depth", a decision to possibly hike, concluding that officials have yet to see convincing evidence in the data warranting a tightening of policy. The surge in oil and natural gas costs has certainly not, as of yet, triggered second-round pricing effects, according to Lagarde, though she conceded the euro-area economy is "certainly moving away" from the ECB's baseline scenario.4 The ECB is also having to balance deteriorating growth. Data published shortly before the rate announcement showed eurozone GDP grew by a weaker-than-expected 0.1% in the first quarter, fuelling stagflation fears, though Lagarde was quick to push back, commenting: "We don't apply stagflation – that flashy term – to the circumstances that we have".4

In the US, the Fed’s policy committee, the FOMC, left the policy rate unchanged at 3.50%–3.75%, in line with expectations. However, the decision was marked by an unusually high four dissents, the most since 1992, underscoring growing divisions within the committee. Governor Stephen Miran again dissented in favour of a rate cut, while three regional Fed presidents supported holding rates steady but objected to retaining the easing bias in the statement. The dispute centred on a single word: “additional”. The current statement refers to “the extent and timing of additional adjustments to the target range for the federal funds rate”, and by keeping that wording, the committee implicitly suggests that the next move is more likely to be a cut than a hike. The three dissenting presidents wanted the term removed, which would have shifted the Fed to a more symmetrical stance in which the next move could just as easily be a hike as a cut. At the post-meeting press conference, Chair Powell acknowledged that the centre of the committee is “moving toward a more neutral place” but said the majority did not believe this meeting was the right moment to make that change, given the elevated uncertainty stemming from the Iran war.5

Overall, of the ten central banks meeting this week, nine left policy unchanged. The outlier was Brazil, which cut rates by 25 basis points – a move entirely understandable given the need to unwind an extraordinarily tight monetary stance, with ex-ante real rates still running close to 10%. Even so, the accompanying guidance struck a cautious tone.6

And that caution was the common thread running through every policy meeting this week. Uncertainty over the Iran conflict – its duration, its trajectory and its ultimate impact on growth and inflation through elevated energy prices – has not yet generated sufficient underlying data for policymakers to draw firm conclusions.

In our view, Alan Greenspan best summarizes the mood: "Uncertainty is not just an important feature of the monetary policy landscape; it is the defining characteristic of that landscape - risk management often involves taking out insurance against adverse outcomes".7 Sometimes waiting and preserving flexibility is the safer course. This week, ten central banks said precisely that.

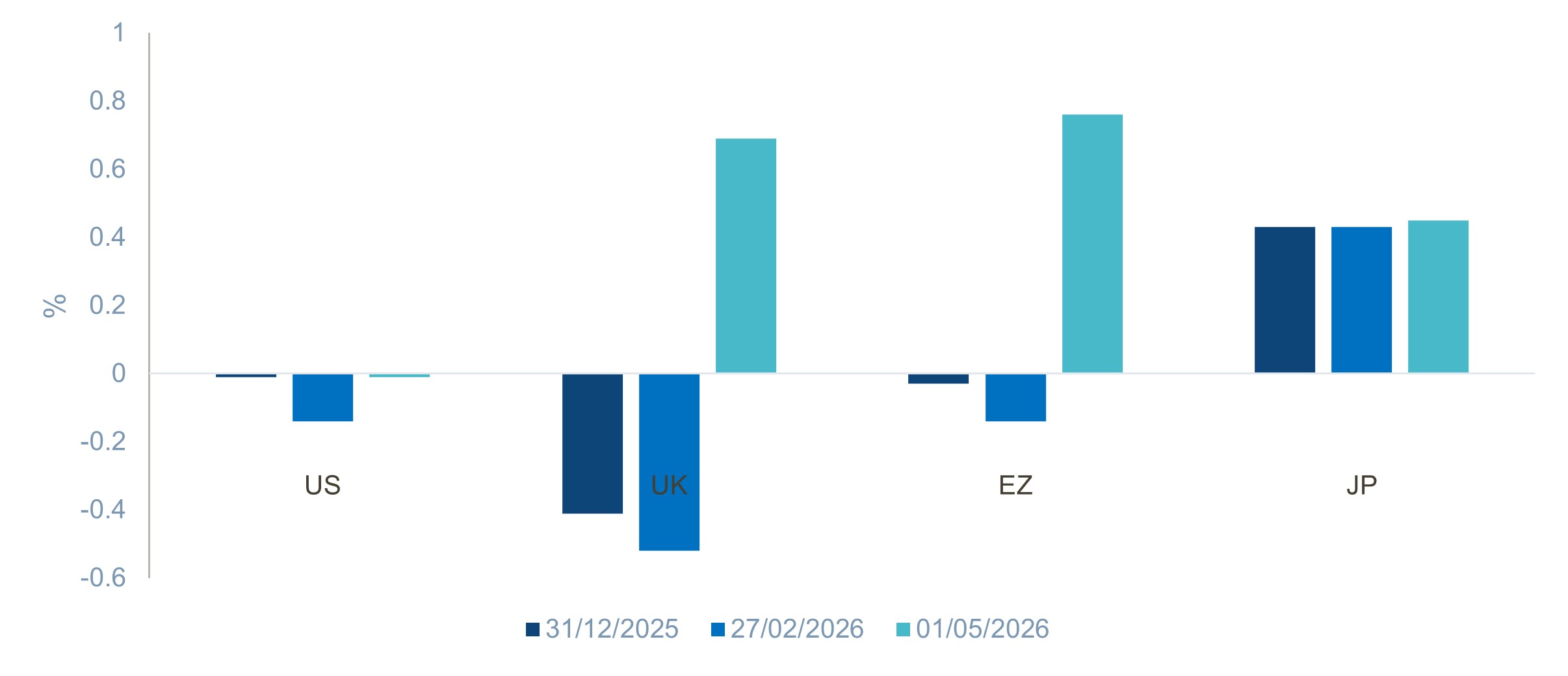

Policymakers now have the luxury of a six-week pause before their next scheduled meetings in June; a window they appear confident will be sufficient to assess the full economic impact of the conflict. In the meantime, they have deliberately set aside any directional bias on rates, poised at the starting blocks, data in hand, ready to act. The question is whether European investors have already jumped the gun – or indeed – whether the central banks themselves have missed the starter's pistol entirely, as investors are now pricing in a significant tightening cycle for both the BoE and ECB (see Chart of the Week). This stands in stark contrast to US policy expectations, where rates are likely to remain on hold, a transatlantic divergence that carries an uncomfortable historical echo. This last occurred in 2011, in the aftermath of the Global Financial Crisis (GFC), when the ECB raised rates twice while the Fed held at zero, a move now widely regarded as a mistake as the ECB tightened policy into a fragile economic environment.

As for April’s performance, it followed the historically favourable seasonal pattern almost to the letter. Government bond yields rose broadly, with most curves bear flattening; the exception was Japan, where the curve bear steepened, while UK gilts were the notable underperformer, again in line with seasonal tendencies. In credit markets, total returns were positive, with high yield outperforming and EM high yield taking the top spot, entirely consistent with historical patterns. Elsewhere, the dollar weakened, commodity prices advanced and equity markets rallied strongly, with the Bloomberg World Large & Mid Cap Index ending the month up more than 8%, all broadly in keeping with seasonal norms.

Here’s hoping the notorious May seasonals fail to live up to their reputation. What does seem clear is that, with central banks not due to make their next policy announcements until June, geopolitics and shifting signals from the US administration are likely to be the dominant market drivers in the month ahead.

Chart of the Week: Have investors jumped the gun, or have central banks missed the starter pistol in Europe?

OIS policy pricing YE 2026

Source: Bloomberg as of May 1, 2026. For illustrative purposes only.

All sources are Bloomberg unless otherwise stated.

Past performance is not a reliable indicator of current or future results.

References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of 1st May 2026 and may change without notice.

References

1. Bloomberg, “Hegseth Battles Democrats Over Iran War at 60-Day Mark,” April 30, 2026

2. Bloomberg, “BOJ REACT: Hawkish Dissenters vs. Takaichi? Hold Now, June Hike,” April 28, 2026

3. Bloomberg, “BOJ REACT: Energy Shock Too Big to Ignore—Tightening Ahead,” April 30, 2026

4. Bloomberg, “Lagarde Signals ECB to Consider June Hike After Latest Hold,” April 30, 2026

5. Bloomberg, “US REACT” Three FOMC Hawks Overshadow Powell’s Last Stand,” April 29. 2026

6. Bloomberg, “BRAZIL REACT: Cautious BCB Cut Flags Risks to Easing Outlook,” April 30, 2026

7. The Federal Reserve Board, “Monetary Policy under Uncertainty,“ remarks by Chairman Alan Greenspan at a symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming, August 29, 2003

--------

Important information

Muzinich & Co., “Muzinich” and/or the “Firm” referenced herein is defined as Muzinich & Co. Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Any forward-looking information or statements expressed in the above may prove to be incorrect. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Muzinich gives no undertaking that it shall update any of the information, data and opinions contained in the above.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

In the United Arab Emirates (UAE) (excluding the Dubai International Financial Centre (DIFC) and the Abu Dhabi Global Market (ADGM): This document, and the information contained herein, does not constitute, and is not intended to constitute, a public offer of securities in the United Arab Emirates (“UAE”) and accordingly should not be construed as such. The Units are only being offered to a limited number of exempt Professional Investors in the UAE who fall under one of the following categories: federal or local governments, government institutions and agencies, or companies wholly owned by any of them. The Units have not been approved by or licensed or registered with the UAE Central Bank, the SCA, the Dubai Financial Services Authority, the Financial Services Regulatory Authority or any other relevant licensing authorities or governmental agencies in the UAE (the “Authorities”). The Authorities assume no liability for any investment that the named addressee makes as a Professional Investor. The document is for the use of the named addressee only and should not be given or shown to any other person (other than employees, agents or consultants in connection with the addressee’s consideration thereof).

In the United Arab Emirates (UAE) (including the Dubai International Financial Centre and the Abu Dhabi Global Market): This information does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe for or purchase, any securities or investment products in the UAE and accordingly should not be construed as such. Furthermore, this information is being made available on the basis that the recipient is an entity fully regulated by the ADGM Financial Services Regulatory Authority (FSRA), and acknowledges and understands that the entities and securities to which it may relate have not been approved, licensed by or registered with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority, the Financial Services Regulatory Authority or any other relevant licensing authority or governmental agency in the UAE. The content of this report has not been approved by or filed with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority or the Financial Services Regulatory Authority.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-05-05-18410