Muzinich Weekly Market Comment: Holding the line - central banks face an inflationary test

Insight

June 15, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

With two central bank meetings and the fate of the Strait of Hormuz negotiations looming over markets, this is a week where patience will be tested and where the distinction between a policy inflection and a policy hold may matter a great deal.

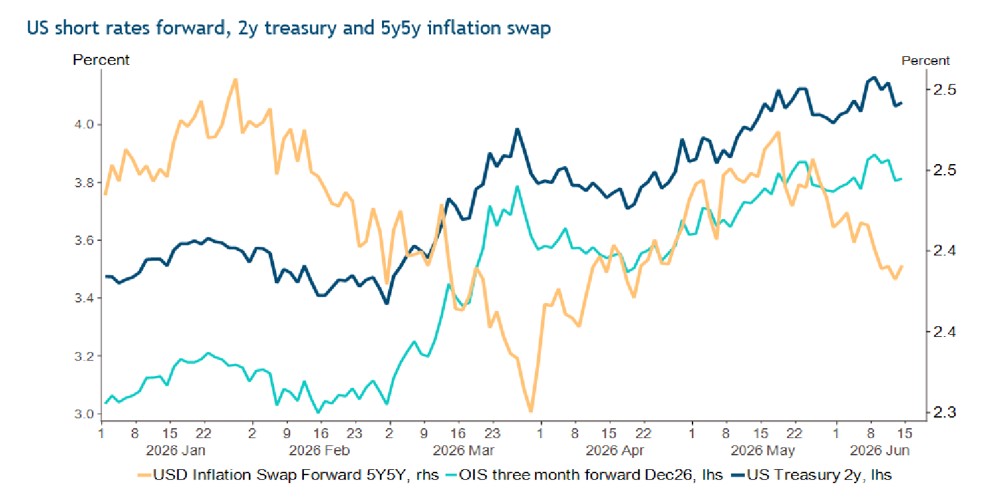

As the Federal Reserve (Fed) meets on June 17-18, markets may become increasingly sensitive to domestic inflationary pressures. With the Consumer Price Index (CPI) and Producer Price Index (PPI) data for May now in hand, analysts estimate the Personal Consumption Expenditures (PCE) index rose 0.5% month-on-month in May, with core PCE up 0.3% over the same period.1 We believe the Federal Open Market Committee (FOMC) will remove any reference to an easing bias from its statement while expressing concern over the trajectory of core inflation. Kevin Warsh will chair the meeting for the first time, and we would expect him to build consensus around such a modification. With uncertainty remaining elevated regarding the reopening of the Strait of Hormuz, the FOMC may opt for a balanced risk assessment, acknowledging the continued improvement in the US labour market while remaining vigilant on inflation. Our baseline is that the Fed remains patient, holding policy rates steady and awaiting further developments in energy markets. US market rates have risen since March, with 2-year Treasury yields moving from 3.4% to 4.1%. Markets have widely priced in a 25 basis points (bps) hike from the Fed before year-end; we view this repricing of the short end of the curve as an opportunity to gain exposure and capture carry in short-dated credit. (See Chart of the Week.)

The 25bps rate hike by the European Central Bank (ECB) last week was well telegraphed and broadly anticipated, with market pricing moving little on the announcement. At the press conference, President Lagarde pushed back against the concept of an “insurance hike,” signalling that a “one and done” scenario is not the baseline,2 with markets currently pricing in two further hikes this year.3 Our baseline is that one additional hike appears justified given the duration of the conflict, the time required to normalize oil markets once the Strait reopens, and the broadening indirect effects of elevated oil prices on the euro area economy. Whether a hike comes in July or September will depend on the evolution of diplomatic negotiations and would be of limited significance unless it were to signal a shift toward a more severe ECB scenario. The resilience of the ECB staff’s GDP forecasts – produced despite anticipated rate hikes and higher-for-longer oil prices – is notable. In our view, the objective appears to be to focus market attention on the inflationary impact of oil prices and the case for further monetary policy action, consistent with our expectation that the ECB will maintain a hawkish posture and keep market rates elevated without necessarily delivering a prolonged sequence of hikes. The next significant reassessment of ECB policy is likely to come at the Sintra conference at the end of June.

The Bank of England (BoE) meets the day after the Fed, and we expect policy rates to remain on hold. Economic data have softened since the last meeting, and the prospect of an imminent US-Iran agreement – including a reopening of the Strait of Hormuz – should reinforce the Monetary Policy Committee’s (MPC) wait-and-see posture. Unlike the ECB, the BoE has been operating in restrictive territory, affording the MPC greater scope for patience; however, the March meeting communication prompted a sharper market reaction than anticipated, with the April meeting serving to recalibrate the tone. Against a backdrop of unresolved geopolitical tensions, recent macro developments do not appear to create immediate pressure to act. Real yields have risen meaningfully in the UK gilt market, partly reflecting geopolitical risk spillover, suggesting that financial conditions have tightened sufficiently to support a hold at this juncture.

Data released this past week offered a rare note of encouragement. US consumer confidence improved in June, with the University of Michigan sentiment index rising from 44.8 to 48.9 – the first monthly gain since January – while one-year and five-year inflation expectations both eased.4 Whether the improvement translates into stronger retail sales remains to be seen, with the data due in the week ahead. In Europe, the UK May Consumer Price Index (CPI) is expected to rebound modestly following the downside surprise in April, while employment data will be closely watched as a key input to the forward rate path. The June ZEW survey in Germany, due Tuesday, will be monitored for signs the improvement in business conditions signalled by recent Purchasing Managers’ Index (PMI) data is being sustained.

Beyond central bank decisions, any acceleration in the diplomatic resolution of the US-Iran conflict will remain a key driver of broader market sentiment. Credit markets were well supported into the end of last week, with a slowdown in new issuance helping to absorb the heavy primary activity of preceding weeks. Investor demand is expected to remain constructive, underpinned by coupon and redemption flows providing a steady source of reinvestment.

Chart of the Week: US short rates moved higher

Markets are now expecting a US policy rate hike before year end, despite stable medium-term inflation expectations.

Source: Macrobond, Bloomberg, as of June 11, 2026. Muzinich views and opinions are subject to change. For illustrative purposes only, not to be construed as investment advice or an invitation to engage in any investment activity.

Past performance is not a reliable indicator of current or future results.

References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

References

1. Oxford Economics, "US PCE Nowcast – Headline inflation will creep above 4%," June 12, 2026

2. ING Think economic and financial analysis, "Lagarde keeps the door open for further ECB rate hikes," June 11, 2026

3. Morningstar, "European Central Bank Raises Interest Rates and Lifts Inflation Forecasts," June 11, 2026

4. FXStreet, "University of Michigan Consumer Sentiment Index rises to 48.9 in June," June 12, 2026

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of June 5, 2026, and may change without notice. All data figures are from Bloomberg, as of June 12, 2026, unless otherwise stated.

--------

Important information

Muzinich & Co., “Muzinich” and/or the “Firm” referenced herein is defined as Muzinich & Co. Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Any forward-looking information or statements expressed in the above may prove to be incorrect. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Muzinich gives no undertaking that it shall update any of the information, data and opinions contained in the above.

United Arab Emirates (UAE): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the UAE. It is intended solely for Professional Investors and should not be relied upon by any other person. This material has not been reviewed or approved by the UAE Securities and Commodities Authority, the UAE Central Bank or any other relevant authority. Nothing contained herein constitutes investment, legal, tax or other professional advice. Recipients should make their own independent assessment where appropriate.

Abu Dhabi Global Market (ADGM): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the ADGM. It is intended solely for Professional Clients (as defined by the Financial Services Regulatory Authority) and should not be relied upon by any other person. This material has not been reviewed or approved by the Financial Services Regulatory Authority or any other relevant authority in the UAE.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-05-18-18512

By clicking "Submit", I am (i) signing up to receive the Opinion Pieces from the "Opinions" page of the Muzinich & Co website, (ii) representing that the above information is true and accurate and (iii) agreeing to join the Muzinich & Co mailing list. I understand that Muzinich & Co will not add retail investors or individuals with personal email addresses to its mailing list and represent that I am not a retail investor. By providing my personal and professional information I am consenting to its use and disclosure in accordance with the Muzinich & Co. Privacy Policy. I understand that I may withdraw my consent and unsubscribe from receiving future communications by clicking "Unsubscribe" from the emails that are sent to me from Muzinich & Co.