Muzinich weekly market comment: Economic divergence

Insight

May 26, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

As market momentum fades and inflation surprises ease, a growing divergence between the US and Europe is coming into sharper focus. While AI-driven investment continues to support US growth and reinforce expectations for tighter policy, weakening activity across Europe is raising concerns over stagnation and narrowing central bank options.

Trend fatigue set in last week as investors appeared to run out of steam, with momentum behind the latest themes visibly fading. Equity and bond volatility followed suit with the VIX and MOVE indices grinding lower in a mood of collective exhaustion. These conditions gave way to modest price reversals, both outright and on a relative basis across markets.

Government bond markets bull flattened, partially reversing the previous week's bearish steepening, with that week’s underperformers now leading the rally. The 30-year UK gilt yield fell 18 basis points (bps). Corporate credit markets were relatively quiet; European credit modestly outperformed its peers. Currencies were mixed, the dollar edging higher against the euro and Australian dollar but softening against UK sterling and the New Zealand dollar. Commodities fell broadly, with energy off around 5% and metals down roughly 3%. Equity fatigue was most visible in technology-linked indices and regions, with the Dow Jones Industrial outperforming within the US and European equities leading in developed markets.

Politics ended the week in a slightly more constructive mood, with positive developments nudging ahead of the negatives. In the Middle East, President Trump – whose ceasefire period now exceeds the duration of active military operations – said the US is in the "final stages" of a possible draft deal to end the conflict, while Iran's Tasnim news agency reported that Tehran is reviewing a new US draft submitted in response to its 14-point proposal.1 In the UK, Andy Burnham, the Manchester mayor and favourite to succeed as Prime Minister, ruled out changing the government's fiscal rules if he came to power.2 In Japan, Finance Minister Katayama stated that fiscal policy remains proactive rather than expansionary, with the extra budget likely in line with market expectations at around US$19 billion. Katayama also noted that the cancellation of bond sales from the previous annual budget would limit the need for fresh deficit-covering issuance.3

On the economic front, there was even relief on the inflation picture, with both UK and Japanese inflation surprising to the downside. This was a welcome development for the two central banks, whose preferred stance is to wait and see as the Middle East conflict plays out.

In Japan, the key inflation gauge rose at its slowest pace in four years, as government measures continued to ease the cost of living. Japan’s core Consumer Price Index (CPI), excluding fresh food, rose 1.4% year-over-year (YoY) in April, a softer-than-expected print that suggested price momentum was not overheating. The moderation largely reflected base effects from last year, lower school lunch fees, and government subsidies capping gasoline prices.4 In the UK, CPI inflation fell to 2.8% in April from 3.3% in March, coming in below both consensus of 3.1% and the Bank of England’s own projection of 3%. The softer reading is likely a one-off, driven by favourable base effects as last year’s elevated household energy bills dropped out of the annual comparison, and the financial new year service price increases proved less aggressive than in the prior year.5 The overnight interest rate swap market is now fully pricing in the first policy tightening of 25bps in September for both Japan and the UK.6

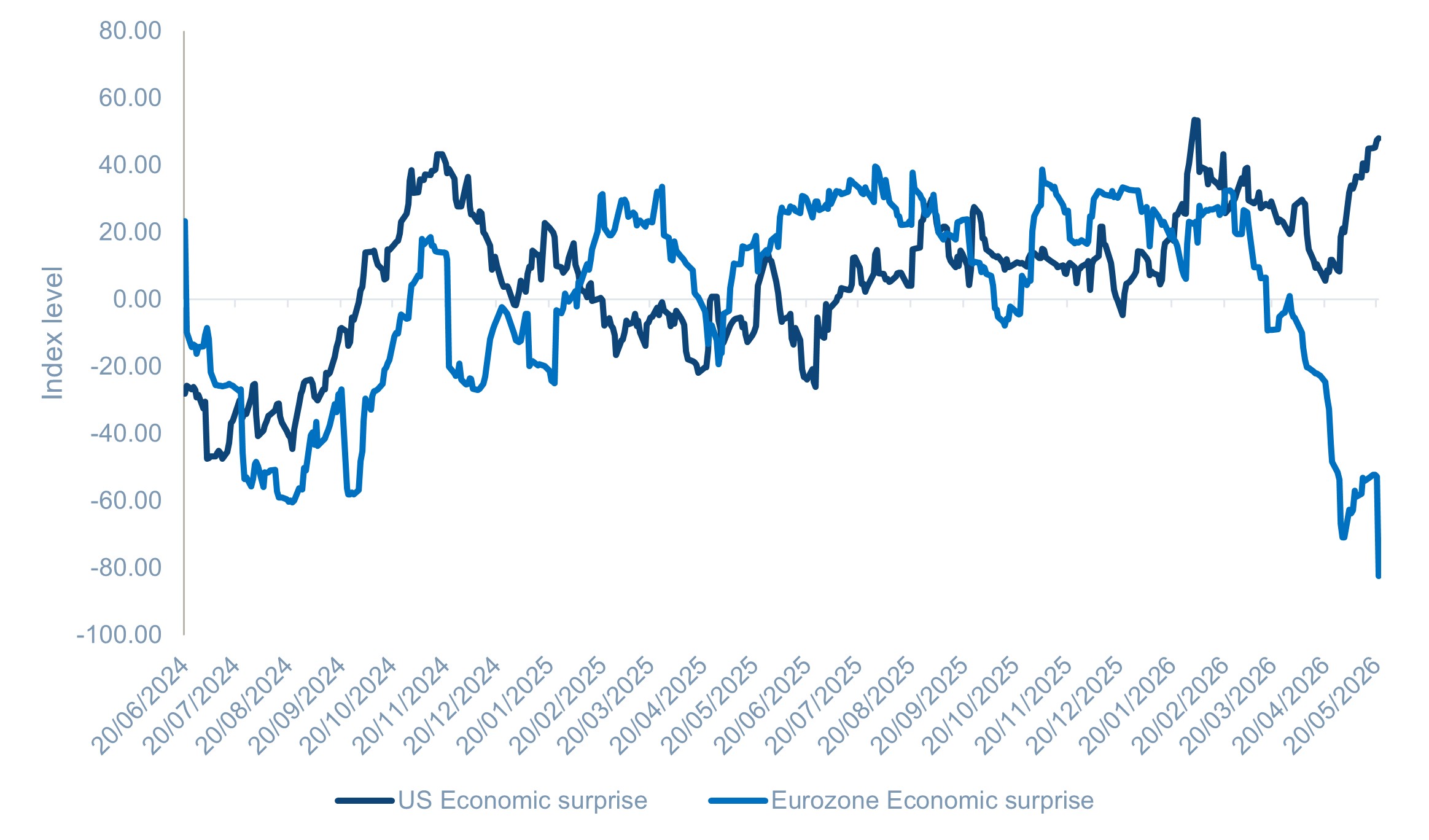

However, if there was one trend that ran uninterrupted through the week, it was Europe’s growing economic divergence from the rest of the world. Nowhere was this more apparent than in comparison with the US, with the two economies moving in nearly opposite directions. To illustrate this point, the Citigroup Economic Surprise Index tells a striking story. The Eurozone currently sits at -82, a level signalling economists have repeatedly overestimated growth and that the economy is losing momentum far more quickly than expected. The US, by contrast, reads +48, a level indicating that economic releases are consistently beating consensus expectations, and suggesting significant positive momentum in economic activity.7 See Chart of the Week.

This week’s Eurozone composite Purchasing Managers' Index (PMI) painted a picture of deterioration, contracting at an accelerated pace and falling short of consensus in a sign of an unexpectedly sharp slowdown in activity. The headline reading dropped to 47.5 from 48.8 in April, below the Bloomberg median forecast of 48.8 The country breakdown was particularly uncomfortable in France, which saw the sharpest deterioration, with its composite figure plunging to 43.5 from 47.6, levels not seen since the Covid-19 pandemic. Germany, the bloc’s largest economy, showed little sign of recovery, edging only marginally higher to 48.6 from 48.4 in April, remaining below the 50 threshold that separates expansion from contraction.8 UK activity data did not offer any comfort; unemployment unexpectedly rose to 5% in the 3 months to March, while monthly payrolls dropped by 100,000 in April.9 Retail sales data also showed consumers pulling back, cutting spending and making fewer car journeys, with sales falling at their fastest pace in nearly a year.10

For the US, the defining difference is AI. Capex spending estimates for this year centre around US$750 billion, equivalent to more than 2% of GDP, and are projected to grow to US$1.6 trillion annually by 2031.11 Spending of this magnitude is fundamentally supportive of broader economic activity, and the positive knock-on effects are already visible in corporate earnings. Excluding the Magnificent 7, the remaining 493 S&P 500 companies reported a blended earnings growth of 17.4% in Q1, the highest rate for this group since Q4 2021.12

This leaves central banks facing a difficult dilemma. In Europe, even though policy rates are close to neutral, concerns are growing over the prospect of mild stagflation as the energy shock simultaneously pushes up prices while weighing on growth. In such an environment, conventional policy tools begin to work against each other. Raising rates to contain inflation risks deepening the slowdown in activity, while cutting rates to support growth could further fuel inflationary pressures.

For US policymakers, the calculus may be more orthodox, as inflationary pressure builds from the energy shock at the same time as the economy runs hot on the positive impulse from AI capex spending. This message came through clearly in the minutes of the April Federal Open Market Committee (FOMC) meeting, which showed officials growing more open to the potential need to raise rates. A majority of participants highlighted that policy firming would likely become appropriate if inflation were to continue running persistently above 2%, with many officials calling for the Federal Reserve to drop its easing bias.13

With policy rates currently at restrictive levels, the FOMC has time on its side to assess whether the energy shock proves transitory, and whether AI delivers the disinflationary productivity gains some expect. Investors, however, have already made up their minds. At the start of the year, two 25bps cuts were priced into the overnight interest rate swap market. That has now swung to one 25bps hike.14

Chart of the Week: Citigroup Economic Surprise Index

Source: Bloomberg, as of May 22, 2026. For illustrative purposes only.

Source: Bloomberg, as of May 22, 2026. For illustrative purposes only.

All sources are Bloomberg unless otherwise stated.

Past performance is not a reliable indicator of current or future results.

References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

References

1. Bloomberg, “Iran Reviewing Trump’s Latest Offer as Clock Ticks on Ceasefire,” May 21, 2026

2. Bloomberg, “Gilt relief rally sense yields to biggest weekly drop since 2024,” May 22, 2026

3. Bloomberg, “Japan’s Extra Budget Not Far From $19 Billion, Katayama Suggest,” May 21, 2026

4. Bloomberg, “JAPAN REACT: CPI Miss Masks Underlying Heat; BOJ Hike Likely,” May 21, 2026

5. Bloomberg, “UK REACT: CPI Miss Buys BOE Time, War Keeps Hike in Play,” May 20, 2026

6. Bloomberg, as of May 22, 2026

7. Bloomberg, Citi Economic Surprise Index - United States (CESIUSD INDEX), Citi Economic Surprise Index – Eurozone (CESIEUR INDEX), as of May 22, 2026

8. Bloomberg, “EURO-AREA REACT: PMI Drops Sharply, May Limit ECB Hiking,” May 21, 2026

9. Bloomberg, “UK REACT: Soft Jobs Data Pour Cold Water on Multiple BOE Hikes,” May 19, 2026

10. Bloomberg, “UK Retail Sales Plunge as Iran War Leads to Fewer Car Trips,” May 22, 2026

11. Goldman Sachs Global Institute, “Tracking Trillions: The Assumptions Shaping the Scale of the AI Build-Out,” April 2026

12. Factset Insight, “Mag 7 and Other 493 S&P 500 Companies Are Reporting Highest Earnings Growth Since 2021,” May 21, 2026

13. Bloomberg, “US REACT: FOMC Minutes Show Wider Bid to Drop Easing Bias,” May 20, 2026

14. Bloomberg, as of May 22, 2026

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of 8th May 2026 and may change without notice.

--------

Important information

Muzinich & Co., “Muzinich” and/or the “Firm” referenced herein is defined as Muzinich & Co. Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Any forward-looking information or statements expressed in the above may prove to be incorrect. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Muzinich gives no undertaking that it shall update any of the information, data and opinions contained in the above.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

In the United Arab Emirates (UAE) (excluding the Dubai International Financial Centre (DIFC) and the Abu Dhabi Global Market (ADGM): This document, and the information contained herein, does not constitute, and is not intended to constitute, a public offer of securities in the United Arab Emirates (“UAE”) and accordingly should not be construed as such. The Units are only being offered to a limited number of exempt Professional Investors in the UAE who fall under one of the following categories: federal or local governments, government institutions and agencies, or companies wholly owned by any of them. The Units have not been approved by or licensed or registered with the UAE Central Bank, the SCA, the Dubai Financial Services Authority, the Financial Services Regulatory Authority or any other relevant licensing authorities or governmental agencies in the UAE (the “Authorities”). The Authorities assume no liability for any investment that the named addressee makes as a Professional Investor. The document is for the use of the named addressee only and should not be given or shown to any other person (other than employees, agents or consultants in connection with the addressee’s consideration thereof).

In the United Arab Emirates (UAE) (including the Dubai International Financial Centre and the Abu Dhabi Global Market): This information does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe for or purchase, any securities or investment products in the UAE and accordingly should not be construed as such. Furthermore, this information is being made available on the basis that the recipient is an entity fully regulated by the ADGM Financial Services Regulatory Authority (FSRA), and acknowledges and understands that the entities and securities to which it may relate have not been approved, licensed by or registered with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority, the Financial Services Regulatory Authority or any other relevant licensing authority or governmental agency in the UAE. The content of this report has not been approved by or filed with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority or the Financial Services Regulatory Authority.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-05-26-18561