Beyond cash: The case for short-duration crossover credit

Insight

June 30, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

As investors seek alternatives to low-yielding cash and rate-sensitive fixed income, short-duration global credit strategies are attracting attention. As investors seek alternatives to low-yielding cash and rate-sensitive fixed income, short-duration global credit strategies are attracting attention.

For much of the past decade, investors have faced a difficult dilemma. Cash and short-dated government bonds have traditionally provided stability and liquidity, but often at the expense of meaningful income. At the other end of the spectrum, investors seeking higher returns have typically needed to accept greater interest rate or credit risk or relinquish liquidity.

Today, many investors are looking for a middle ground - a strategy that can generate attractive income without taking excessive risk, whilst being structured to preserve capital and offer daily liquidity. This has helped drive interest in short-duration global credit strategies that often combine selected investment grade and high yield bonds (i.e. a ‘crossover’ approach) while maintaining an overall investment grade profile.

Seeking income through a broader opportunity set

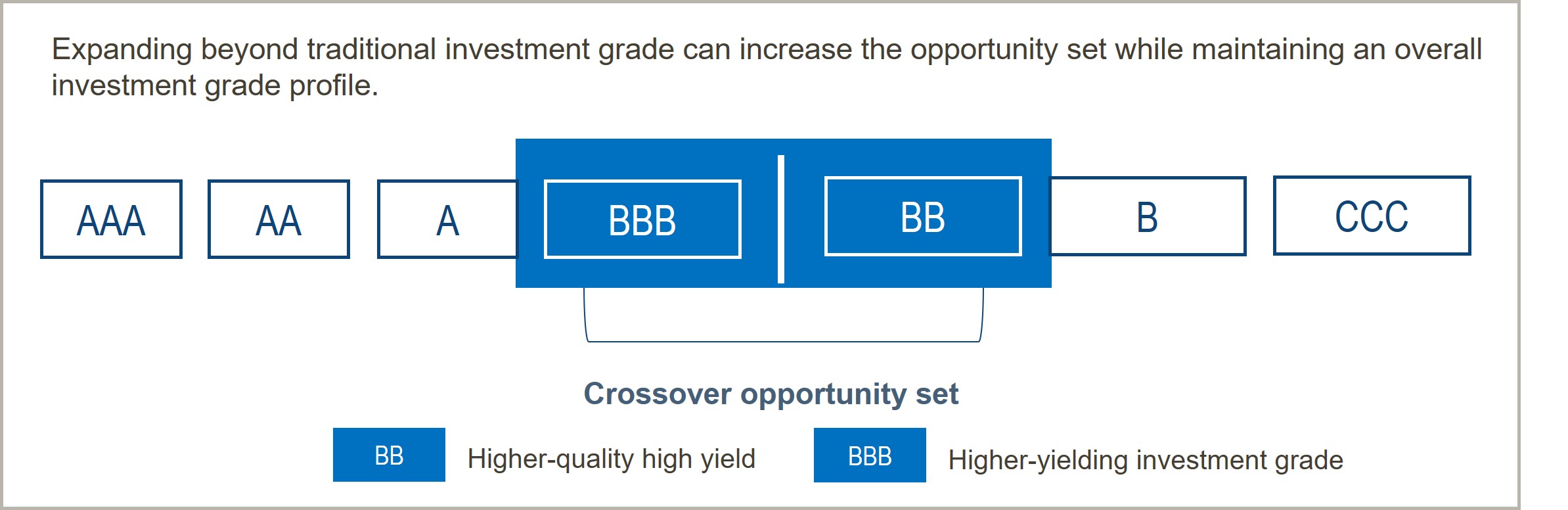

A crossover strategy has the flexibility to invest across investment grade and high yield credit but will often maintain an average investment grade rating. This gives managers the flexibility to identify the best risk-adjusted opportunities across the rating spectrum, particularly in the BBB-BB part of the market. Here instruments can often be mis-priced if they are split-rated for example, or transitioning between investment grade and high yield markets. For investors seeking enhanced yields but with an eye on credit risk, this part of the market offers access to the higher yielding parts of investment grade, and the highest quality parts of high yield.

A moderate allocation to short duration high yield bonds in an investment grade portfolio we believe can enhance returns over time, whilst the average investment grade rating and short duration profile constrains the overall risk profile of the portfolio.

A global mandate further expands the opportunity set, allowing managers to exploit relative value opportunities across regions while enhancing diversification.

Multiple return drivers and an element of predictability

Short-duration portfolios have several structural benefits that can suit more conservative investors and to help enhance returns. First, yield can be taken as a good guide for likely performance, since when bonds are repaid at maturity, investors will typically have received the annualised yield at which they bought the bond.

Returns could be enhanced further if the portfolio is managed efficiently to capture accelerated returns from ‘roll-down’. As bonds approach maturity, their yield typically falls as repayment risk by the issuer declines. Falling yields are typically accompanied by enhanced returns during this period, with lower returns seen as bonds near maturity.

A short duration manager can therefore enhance returns by aiming to hold bonds as they roll down their yield curve, before rotating into new opportunities once the most attractive returns have been achieved.

A shorter duration profile can also help reduce sensitivity to interest rate and credit spread movements, helping shelter investors from volatility in broader markets. This gives short duration strategies the opportunity to offer steadier returns, particularly in a higher yield environment.

Short maturities offer another advantage during periods of market volatility. As bonds mature, capital is returned and can be reinvested into new opportunities. This potentially allows portfolios to take advantage of market dislocations more quickly than longer-duration strategies, as cash is reinvested into higher-yielding opportunities during periods of market weakness.

None of this eliminates risk entirely. Credit investing always carries the possibility of price declines and unexpected market volatility. However, rigorous credit analysis, diversification and a strategy that is structured to help preserve capital and generate steady returns can help mitigate these risks.

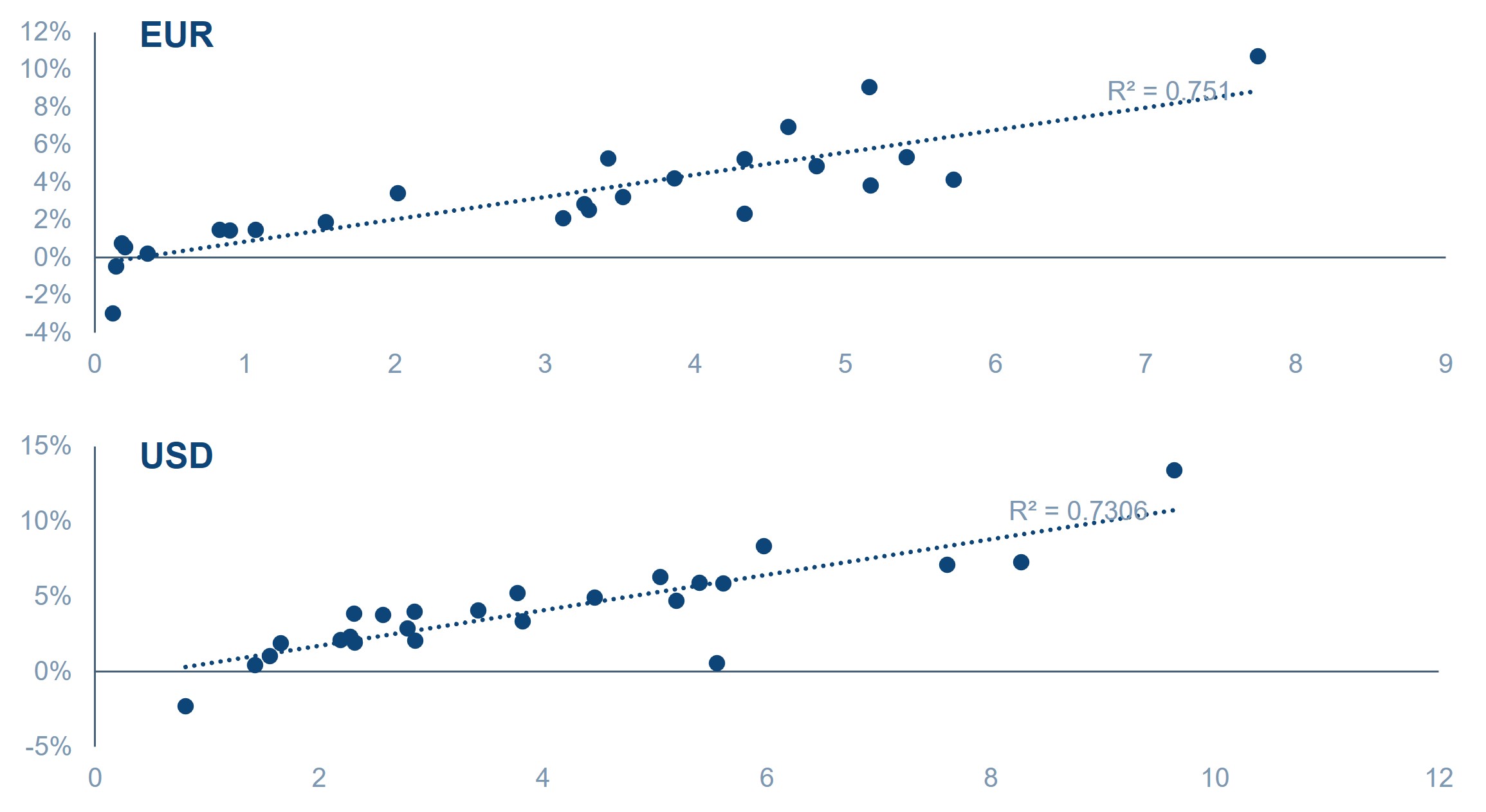

Fig. 1: Starting yield - a strong predictor of subsequent returns

Past performance is not a reliable indicator of current or future results

Source: ICE Index Platform, 31st December 1999 - 31st December 2025. EUR - ICE BofA 1-3 Year BBB Euro Corporate Index (ER41) USD - ICE BofA 1-3 Year BBB US Corporate Index (C1A4). Indices used represent best proxy to illustrate performance of short-dated EUR and USD credit. Latest available data used. For illustrative purposes only.

Where crossover managers find value

Source: Muzinich & Co. For illustrative purposes only.

Source: Muzinich & Co. For illustrative purposes only.

Finding value in crossover credit

Within investment grade credit, we believe the BBB segment often provides some of the most compelling opportunities. As the lowest rung of the investment grade ladder, BBB-rated issuers typically offer a meaningful yield premium over higher-rated bonds while retaining investment grade characteristics. Many are fundamentally strong businesses that are improving operationally, reducing leverage or strengthening their balance sheets. Many are also new to the bond market, and perhaps less widely covered by the investment community. Through detailed bottom-up analysis, active managers can identify credits whose prospects are stronger than their ratings alone might suggest.

The same philosophy applies within high yield. Rather than seeking the highest yields available, a conservative crossover strategy can focus on the upper tier of the high yield market, particularly BB-rated issuers. These companies often possess many of the characteristics associated with investment grade borrowers. Some may be fallen angels that have been downgraded despite retaining robust fundamentals, while others may be rising stars on a path towards investment grade status. Identifying these opportunities in our opinion can provide multiple sources of return, combining attractive income with the potential for capital appreciation as improving credit fundamentals are rewarded with rating upgrades.

Where active managers find value

Source: Muzinich & Co. For illustrative purposes only.

A compelling alternative to cash

For many investors, a crossover credit strategy can occupy an important position within a broader portfolio. It can serve as an enhanced alternative to cash or short-dated government bonds, offering the potential for higher income while maintaining a conservative risk profile. At the same time, it can complement traditional fixed income allocations by providing exposure to credit markets with lower duration risk.

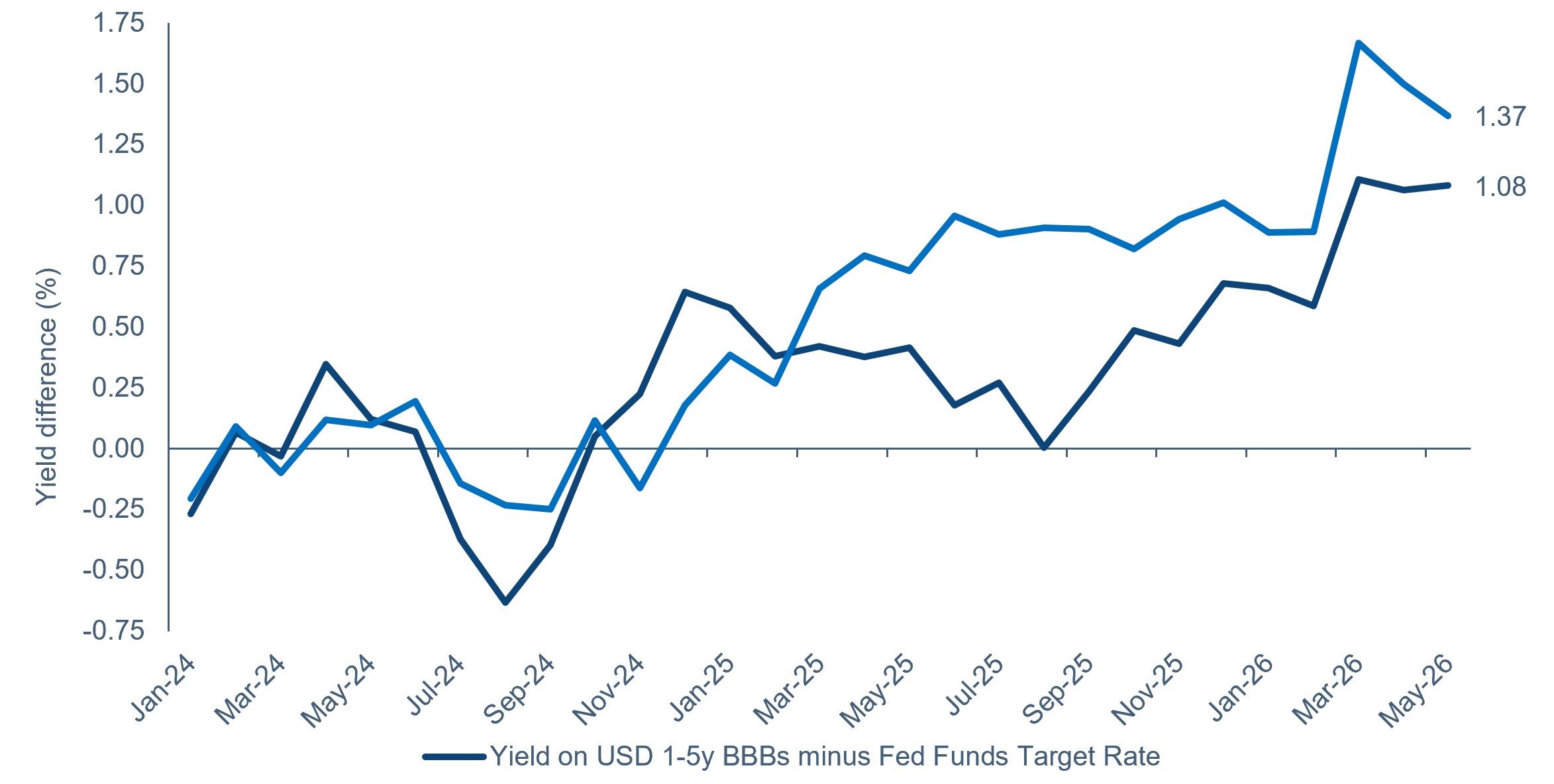

Figure 2 – Yield premium in short-dated credit over policy rates

Source: ICE Data Platform and Bloomberg as of 31st May 2026. ICE BofA 1-3 Year US BBB Corporate Index (CVA4), ICE BofA 1-3 Year Euro BBB Corporate Index (ER4V). Indices selected by Muzinich as best available proxies for the respective markets. For illustrative purposes only.

In a world where investors increasingly seek both resilience and return - and where many are cautious of taking ‘full market’ exposure in either investment grade or high yield – we believe a short-duration crossover strategy offers a compelling proposition.

By combining the flexibility of a global opportunity set, the enhanced income potential of incorporating both investment grade and high yield bonds, and a strong emphasis on capital preservation, a crossover strategy can provide a practical solution for investors seeking to put cash to work without moving too far up the risk spectrum.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of June 2026 and may change without notice.

--------

Index descriptions

CVA4 - ICE BofA 1-3 Year US BBB Corporate Index. is a subset of the ICE BofA US Corporate Index including all securities with a remaining term to final maturity less than 3 years.

ER4V - ICE BofA 1-3 Year Euro BBB Corporate Index is a subset of the ICE BofA Euro Corporate Index (ER00) including all securities rated BBB1 through BBB3, inclusive with a remaining term to final maturity less than 3 years

Important information

Muzinich and/or Muzinich & Co. referenced herein is defined as Muzinich & Co., Inc. and its affiliates. Muzinich views and opinions. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall.

Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only.

This discussion material contains forward-looking statements, which give current expectations of future activities and future performance. Any or all forward-looking statements in this material may turn out to be incorrect. They can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Although the assumptions underlying the forward-looking statements contained herein are believed to be reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurances that the forward-looking statements included in this discussion material will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Further, no person undertakes any obligation to revise such forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

United Arab Emirates (UAE): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the UAE. It is intended solely for Professional Investors and should not be relied upon by any other person. This material has not been reviewed or approved by the UAE Securities and Commodities Authority, the UAE Central Bank or any other relevant authority. Nothing contained herein constitutes investment, legal, tax or other professional advice. Recipients should make their own independent assessment where appropriate.

Abu Dhabi Global Market (ADGM): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the ADGM. It is intended solely for Professional Clients (as defined by the Financial Services Regulatory Authority) and should not be relied upon by any other person. This material has not been reviewed or approved by the Financial Services Regulatory Authority or any other relevant authority in the UAE.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-06-23-18806

Why consider short-duration crossover credit?

By clicking "Submit", I am (i) signing up to receive the Opinion Pieces from the "Opinions" page of the Muzinich & Co website, (ii) representing that the above information is true and accurate and (iii) agreeing to join the Muzinich & Co mailing list. I understand that Muzinich & Co will not add retail investors or individuals with personal email addresses to its mailing list and represent that I am not a retail investor. By providing my personal and professional information I am consenting to its use and disclosure in accordance with the Muzinich & Co. Privacy Policy. I understand that I may withdraw my consent and unsubscribe from receiving future communications by clicking "Unsubscribe" from the emails that are sent to me from Muzinich & Co.