Insight | February 6, 2020

Part II - Give a Little Credit: Opportunities in Direct Lending - February 2020

Misperceptions about US Market Potential

With the significant growth of Direct Lending1 as an asset class, there is much discussion and increasing investor concern that competition is leading to lower returns (i.e. spreads) and reduced terms (i.e. covenant light).2 Our analysis supports this concern, with over 70% of the capital raised for direct lending focused on private equity (“PE”) backed middle and upper middle market companies.3 Many direct lenders focus exclusively on this market segment because it is large, acquisitive and an efficient segment in which to originate deals. But this focus clearly creates a more competitive dynamic and requires many established direct lenders with increasingly larger fund sizes to adjust their return expectations. An additional element driving competition is newer direct lending entrants, with less established relationships, pressured to compete on economic and structural terms. However, our research has shown that there are multiple segments for deal sourcing that are sometimes overlooked by many direct lenders and consequently, underserved.

Within this paper, we will provide Muzinich’s experienced insight to highlight four less developed markets for direct lending that deliver what we believe to be attractive yields in the less trafficked lower middle market:

1.Family/Founder-Owned Businesses

2.Orphaned Small-Cap Public Companies

3.Independent Sponsors

4.Cross-Border Financing Opportunities

Section 1: Family/Founder-Owned Businesses – The Largest Market in the US

While it is true that family/founder-owned companies are less active from an M&A perspective and typically more conservative (in terms of leverage) than PE-owned companies, this market segment still actively seeks financing to achieve their corporate objectives. What is consistently overlooked is the size of this market potential.

Specifically, the US middle market – lower, middle and upper – is comprised of approximately 170,000 businesses (annual revenues between $10 million to $1 billion), with over 150,000 of these companies in the lower middle market (annual revenues between $10 million and $100 million), shown below in Figure 1.4

The lower middle market is clearly the largest market for direct lending potential, as these companies generate over $4.1 trillion in revenues annually and the segment is over 7.5x larger than the middle and upper middle markets combined in terms of number of companies.4 Importantly, even with the dramatic growth in private equity, we estimate that only 30% of the companies in the lower middle market are owned by PE firms (Figure 2). To ignore family/founder-owned businesses means direct lenders are eliminating almost 70% of the potential middle market.5

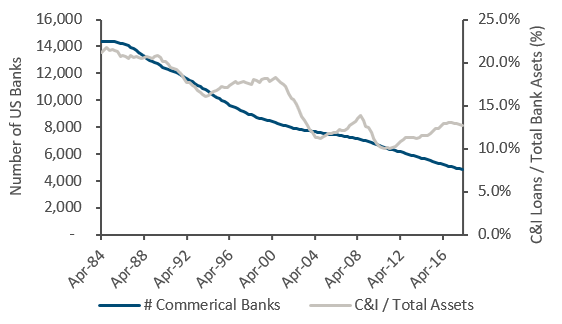

From a supply of capital perspective, there has been consolidation of the banking sector (of approximately 66% since 1984) which has led to a secular decline in C&I lending over the past 30 years (Figure 3). The combination of these two trends leaves approximately 100,000 family/founder firms with fewer financing options and therefore we consider this market underserved.

Fig. 3: US Bank Consolidation

Source: Federal Reserve Bank of St. Louis, FRED Graph Observations through January 2018.

Source: Federal Reserve Bank of St. Louis, FRED Graph Observations through January 2018.

We acknowledge that while this is a large market opportunity, it is highly fragmented and family/founders’ decision making/transaction execution is extremely variable, unlike PE firms. Therefore, direct lenders will need a different deal sourcing strategy to access this market, which can take a significant amount of time. As well, direct lenders may benefit from investment professionals with private equity backgrounds to execute and monitor these investments.

Section 2: Small-Cap Public Companies – Alternative Cost of Capital is Equity

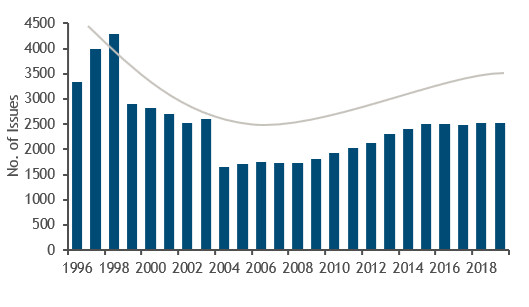

Much has been said about the decline in the number of publicly listed companies, especially small-cap companies (market capitalization of $50 million to $300 million). Following the consolidation of the Tech Boom in the late 1990’s and due to the increased costs of operating a public company in the wake of new regulations, such as The Sarbanes-Oxley Act of 2002, small-cap companies declined by about 30%.6 But interestingly, since December 2004, the number of US small-cap public companies has increased by over 2.5% per annum to 2,500 companies (Figure 4).

Fig. 4: US Small Cap Corporate Businesses (1996-2019)

Source: Bloomberg, as of 12/31/19. ICE BofA ML US Small Cap Corporate Index (Ticker: C0AS).6

Source: Bloomberg, as of 12/31/19. ICE BofA ML US Small Cap Corporate Index (Ticker: C0AS).6

Similar to family/founder companies in the lower middle market, we find that these public companies are situated well below the size demands (at least $250 million of issuance for broadly syndicated loans – “BSL”) of the capital markets (high yield bonds or syndicated loans). Further, the banking industry’s consolidation and retreat from lending, combined with the general lack of focus from the direct lending community has led to a supply imbalance. Therefore, we believe this segment struggles to find debt capital to fund acquisitions and expansions and their only alternative is costly equity issuance.

In our view, direct lenders pursuing this market will require a broader sourcing network and internal professionals with private equity skills to execute and monitor investments, like the family/founder market segment.

Section 3: Independent Sponsors – Back to the Future

Independent sponsors are defined as investors who raise capital for investments on a deal by deal basis (i.e. not a commingled fund). This model may sound familiar – KKR and Carlyle, for example, initially started raising money using this method in the 1980’s. The motivation to start an independent sponsor firm is driven by several key factors: the economic glass ceiling in many PE firms, getting incentive fees on a deal by deal basis (i.e. no netting), eliminating the pressure of a committed fund to deploy money on a consistent basis, and most importantly, the significant increase of available equity capital (Figure 5). In our research, we have found i) family offices have been increasing their desire to invest on a deal by deal basis which has the benefit of reducing their fees vis a vis commingled funds; ii) mezzanine funds, which have been pushed out of traditional LBO financings by uni-tranche structures of direct lenders, have shifted to investing with a minority equity orientation (i.e. mezzanine debt and equity on a 50/50 basis); and iii) larger PE firms, (i.e. fund sizes of $1 billion or more), are increasingly willing to work with independent sponsors as a way to improve deal sourcing and capital deployment rates.

Independent sponsors are estimated to comprise 250 firms in the United States.7 By comparison, our research shows there are approximately 350 PE firms with funds less than $1 billion assets, also targeting the middle market. Therefore, independent sponsors represent approximately 40% of the PE firms active in the lower middle market.

This seems logical to us, as PE firms have raised larger funds, moving upmarket in terms of company size to maintain deployment rates, independent sponsors have gained market share in the lower middle market. In fact, 95% of independent sponsors focus on companies with EBITDA of $15 million and below (Figure 6). These groups are quite active with over 60% reviewing 51 or more transactions on an annual basis (Figure 7).

In our view, the independent sponsor market has a similar lack of focus by banks and most direct lenders.

Section 4: Cross-Border Financing – Complex Capital Structures

Cross-border financing may offer unique opportunities in the direct lending space. In our research, we believe this trend reflects PE firms looking to develop their portfolio companies on a global basis. For the lower middle market, there are few direct lenders with a platform that can execute financings in multiple geographic regions, i.e. US and Europe. However, in the upper middle market, we have found that larger direct lenders demonstrate a capability to provide such financings.

Between 2010 and 2018, there have been over 12,000 annual M&A transactions in the global middle market (Figure 8), over 80% of which had enterprise values less than $100 million.8 The US accounted for 30% of the total volume (Figure 9, below).9, 10

Over the past decade, there has been consistent outbound and inbound global M&A in the US, averaging 4,500 transactions per year (Figure 10). We believe these cross-border financing opportunities will continue the current trajectory of growth.

In Conclusion

We believe that the fundamental, secular needs of financing, particularly for the lower middle market, are still quite strong, but direct lenders need to expand their sourcing models and operating platforms to develop these market opportunities.

————————————————————————————————————————————-

Footnotes

- Direct Lending is the segment within Private Debt whereby senior secured floating rate loans are directly originated.

2. “Why Direct Lending is a Booming Part of Private Debt” – Bloomberg, March 2019

https://www.bloomberg.com/news/articles/2019-03-06/who-needs-a-bank-why-direct-lending-is-surging-quicktake-q-a

3. Based on Muzinich estimates; funds targeting companies with EBITDA > $25+ million.

4. IRS Data 2015. Returns of Active Corporations, Table 3.1 – Selected Balance Sheet, Income Statement, and Tax Items, by Size of Business Receipts.

https://www.irs.gov/statistics/soi-tax-stats-corporation-complete-report

5. Dun & Bradstreet – 2018 Annual Report. World Economic Forum – April 2018. “Fueling the US Economy’s Middle Market Growth Engine”.

6. COAS – ICE BofA ML US Small Cap Corporate Index. This index is a subset of ICE BofAML US Corporate Index excluding all securities with an outstanding face value greater than or equal to $500 million. You cannot invest directly in an index, which also does not take into account trading commissions or costs. The volatility of indices may be materially different from the volatility or performance of an account or fund.

7. Crain’s New York Business. “Nimble investors are making big deals by outhustling private-equity gains”. April 23, 2019.

8. Dealogic and Robert W. Baird & Co. Incorporated M&A Market Analysis. YTD as of 11/30/19.

9. IMAA Mergers & Acquisitions (M&A), United States. Data as of 12/31/19. https://imaa-institute.org/m-and-a-us-united-states/

10. Preqin Private Debt data for Direct Lending and Mezzanine Funds between 2013-2017.

Important Information

Muzinich & Co" and/or "Muzinich" referenced herein is defined as Muzinich & Co., Inc. and it’s affiliates. This document and the analysis herein has been produced for information purposes only and are not intended to constitute an offering, advice or recommendation to purchase any securities or other financial instruments. The investment strategies and themes discussed herein may not be suitable for investors depending on their specific investment objectives and financial situation. Investors should conduct their own analysis and consult with their own legal, accounting, tax and other advisers in order to independently assess the merits of an investment.

Statements throughout this document are views and opinions of the author and/or Muzinich. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only, are as of the date of publication and are subject to change without reference or notification. Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,”, “likely,” “will,” “should,” “could,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or the actual performance of the securities, investments or strategies discussed may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained in this document may be relied upon as a guarantee, promise, assurance or a representation as to the future.

All information contained herein is only as current as of the date indicated, and may be superseded by subsequent market events or for other reasons. Nothing contained herein is intended to constitute investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. Historic market trends and performance are not reliable indicators of actual future market behavior or performance.

Certain information contained herein is based on data obtained from third parties and, although believed to be reliable, has not been independently verified by anyone at or affiliated with Muzinich & Co.; its accuracy or completeness cannot be guaranteed.

Past performance is not an indication of future performance. The value of an investment, and income generated (if any) may fall as well as rise and is not guaranteed. Investors may not get back the full amount invested and may lose the entire amount invested. You cannot invest directly in an index, which also does not take into account trading commissions or costs. The volatility of indices may be materially different from the volatility or performance of an account or fund.

No part of this material may be reproduced in any form or referred to in any other publication without express written permission from Muzinich & Co.

In Europe, this material is issued by Muzinich & Co. Ltd., which is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ. Muzinich & Co. Ltd. is a subsidiary of Muzinich & Co., Inc. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission.