Website Terms of Use

You are about to enter the Muzinich & Co. website (the “Site”) for professional, institutional or qualified clients. This Site is not suitable for retail clients. If you are a retail client, please leave this Site immediately.

The use of this Site is subject to the following terms and conditions which contain important legal, regulatory, and risk information about material contained on this Site (the “Terms”).

After you have read and understood these Terms, you may click “I Agree” to confirm you agree to the Terms. If you do not agree to the below Terms, you must refrain from using this Site and you will be redirected to the homepage.

In these Terms, references to “you” and “your” are references to any person using or accessing (or attempting to use or access) this Site.

About Muzinich

The information on this Site is communicated and issued by Muzinich & Co. Limited (“Muzinich”). Muzinich is authorised and regulated by the Financial Conduct Authority (“FCA”) (registration number 19226). Muzinich is incorporated in England and Wales (company number 03852444) with its registered office at 8 Hanover Street, London, W1S 1YQ, United Kingdom.

The products and services referred to on this Site may not be suitable investments for you and you should seek professional investment advice before making a decision to invest in any of the products or services mentioned on this Site.

Access to this Site

In order to use this Site you have been asked to indicate your location. Your selection will be used to determine the information and documentation you will be able to access on this Site. Failure to provide us with accurate information will be treated as a material breach of these Terms.

This Site is not aimed at any US Person (as defined by Regulations S of the US Securities Act 1933) and is not for distribution and does not constitute an offer to or solicitation to buy any securities in the USA.

Certain products and services may not be available in all jurisdictions and may be restricted by law in certain jurisdictions. Information and documentation about certain products and services may not be available to all users of this Site. You must not attempt to gain access to areas of this Site other than those made available to investors in your country of residence. This Site, and the information and documentation on it, is not addressed to any person resident in a territory or country or jurisdiction where such distribution would be contrary to local law or regulation. Please click here to check whether the products and services have been registered.

If your country of residence changes, you must access this Site selecting your new country of residence. You should be aware that this may result in you not being able to access (i) information in relation to the same products and services as previously, or (ii) any information at all. Please note that the fact of selecting your country of residence does not mean that all or any of the funds in relation to which information is made available on this Site, have been deemed suitable for you.

When using this Site you must comply with all applicable local, national and international laws including those relating to data privacy, international communications and exportation of technical or personal data. It may be unlawful to access or download the information contained on this Site in certain countries and Muzinich and its directors, officers, employees and agents disclaim all responsibility if you access or download any information from this Site in breach of any law or regulation of the country in which you are residing or domiciled.

Muzinich reserves the right to suspend or withdraw access to any page(s) included on this Site without notice at any time and accepts no liability if, for any reason, these pages are unavailable at any time or for any period.

No Advice

The information on this Site is provided for information only and does not constitute, and should not be construed as, investment advice or a recommendation to buy, sell, or otherwise transact in any investment including any products or services or an invitation, offer or solicitation to engage in any investment activity.

The information on this Site is provided solely on the basis that you will make your own investment decisions and Muzinich does not take account of any investor’s investment objectives, particular needs, or financial situation. In addition, nothing on this Site shall, or is intended to, constitute financial, legal, accounting or tax advice.

It is strongly recommended that you seek professional investment advice before making any investment decision. Any investment decision that you make should be based on an assessment of your risks in consultation with your investment adviser.

Past Performance

To the extent that this Site contains any information regarding the past performance of products, such information is not a reliable indicator of future performance and should not be relied upon as a basis for an investment decision. To the extent that this Site contains any information regarding simulated past performance, such information is not a reliable indicator of future performance and should not be relied on as a basis for an investment decision. Past performance does not guarantee future performance and the value of investments and the income from them can fall as well as rise. No investment strategy is without risk and markets influence investment performance. Investment markets and conditions can change rapidly and investors may not get back the amount originally invested and may lose all of their investment.

Risk Warnings

There are significant risks associated with an investment in any products or services provided by Muzinich. Investment in the products and services is intended only for those investors who can accept the risks associated with such an investment (including the risk of a complete loss of investment) and you should ensure you have fully understood such risks before taking any decision to invest.

These Terms do not represent a complete statement of risk factors associated with an investment in any of the products. The offering documentation contain risk warnings which are specific to the relevant products. You should consider these risk warnings carefully and take appropriate investment advice before taking any decision to invest.

Offering Documents

The terms of any investment in any fund are governed by the relevant fund’s offering documents containing such terms. An application for interests in any fund should only be made having fully and carefully read the relevant prospectus, key investor information document (where applicable), the latest financial reports and other offering documents for the relevant fund. Further, such documents may differ by jurisdiction as required by law in those jurisdictions.

FOR AUSTRALIAN WHOLESALE CLIENTS ONLY: Any fund-specific information you access through this website is not a prospectus or product disclosure statement under the Corporations Act 2001 (Cth) (Corporations Act) and does not constitute a recommendation to acquire, an invitation to apply for, an offer to apply for or buy, an offer to arrange the issue or sale of, or an offer for issue or sale of, any securities in Australia, except as set out below. No Muzinich fund has authorised or taken any action to prepare or lodge with the Australian Securities & Investments Commission an Australian law compliant prospectus or product disclosure statement.

Accordingly, any fund-specific information you access through this website may not be issued or distributed in Australia and the related units may not be offered, issued, sold or distributed in Australia other than by way of or pursuant to an offer or invitation that does not need disclosure to investors under Part 6D.2 or Part 7.9 of the Corporations Act, whether by reason of the investor being a ‘wholesale client’ (as defined in section 761G of the Corporations Act and applicable regulations) or otherwise. By clicking “I Agree” below, you are expressly stating that you are a ‘wholesale client’ as previously determined.

Any fund-specific information you access through this website does not constitute or involve a recommendation to acquire, an offer or invitation for issue or sale, an offer or invitation to arrange the issue or sale, or an issue or sale, of units to a ‘retail client’ (as defined in section 761G of the Corporations Act and applicable regulations) in Australia.

Information on this Site

Muzinich has taken reasonable care to ensure that the information on this Site is accurate, current, complete, fit for its intended purpose and compliant with applicable law and regulation as at the date of issue. No warranty or representation of any kind regarding the accuracy, validity or completeness of the information on this Site is given and, to the extent permitted by applicable laws, no liability is accepted for the accuracy or completeness of such information. Any person who acts upon, or changes his or her investment position in reliance on information contained on this Site, does so entirely at his or her own risk. In the event of any inconsistency between the information on this Site and the terms of the relevant offering documents, the terms of the offering documents shall prevail.

Information posted on this Site is current only as at the date it is first posted and may no longer be true or complete when viewed by you. To the extent that any information on this Site relates to a third party, such information has been provided by that third party and is the sole responsibility of such third party and Muzinich accepts no liability for such information. All content on the Site is subject to modification from time to time without notice. Please contact Muzinich using the details set out below for further information regarding the validity of any information contained on this Site.

Limitation of Liability

No warranty is given that the contents of this Site are compatible with all computer systems or browsers or that this Site shall be available on an uninterrupted basis. Muzinich does not accept any liability for any damages or losses arising from changes or alterations made to this Site by unauthorised third parties.

The internet is not a completely reliable transmission medium and neither Muzinich nor any of its affiliates accept any liability for any data transmission errors such as data loss or damage or alteration of any kind or for the security or confidentiality of information transmitted across the internet to or from Muzinich or any of its affiliates. Any such transmission of information is entirely at your own risk and any material downloaded from this Site is downloaded at your own risk.

The information on this Site is provided “as is”. To the extent permitted by law, Muzinich, its affiliates and each of their directors, officers, employees and agents expressly exclude all conditions, warranties, representations and other terms which might otherwise be implied by statute, common law or the law of equity. In no event will Muzinich or any of its affiliates be liable to any person for any indirect, special or consequential damages arising out of any use of, or inability to use, this Site or the information contained on it or on any other hyper-linked site including, without limitation, any lost profits, business interruption, loss of programs or data on your equipment or otherwise, even if Muzinich is expressly advised of the possibility or likelihood of such damages. This does not affect the liability of the Muzinich and its affiliates for any loss or damage which cannot be excluded or limited under applicable law.

Nothing in these Terms is intended to exclude or restrict any duty or liability that Muzinich has to its clients under the “regulatory system” in the United Kingdom (as such terms of defined in the FCA Rules), under applicable local regulatory rules or which may not be excluded or restricted as a matter of applicable law.

Data Protection

By using this Site, you are disclosing to Muzinich your status as a professional client. Muzinich may also record your email address and the IP address of the device you use to access this Site. Any information that that you might provide in registering for access to view restricted portions of the Site will be held confidentially by Muzinich and will not be passed on to other product or service companies, other than service providers to any of the funds or to regulatory or other government agencies as might be required by law. Muzinich will only use information from which you can be identified, such as your name, contact details and ID data (“Personal Information”) which is provided to us, or otherwise obtained by us, as set out in the Muzinich privacy policy which can be found at the following link. Your details may be used by us to send you information on products and services that we offer. Please advise us if you prefer not to receive such information.

Links

The provision of a hyper-link from or to the Site does not provide or imply an endorsement, recommendation or approval of such websites or any material on them. Muzinich accepts no responsibility for information contained on any other websites which can be accessed by hypertext link from this Site or for any of these websites not being available at all times. Muzinich has not reviewed, and will not review or update, such websites or information and any use that you make of such websites and information is at your own risk. No third party link is permitted between the Site and any other website without the express and prior written consent of Muzinich. Please note when you click on any external site hypertext link you will leave this Site.

Cookies

Muzinich may use cookies in some of the pages on this Site. By agreeing to these Terms (i.e. by clicking “I Agree”) you give your consent to the use and placement of cookies in respect of your access to this Site. Please see our Cookie Policy (available here) for more information.

Intellectual Property

The entire content of this Site is subject to copyright with all rights reserved. You may download or print individual sections of this Site for your personal use and information only, provided that you retain all copyright and other proprietary notices. You may not reproduce (in whole or in part), transmit (by electronic means or otherwise), modify, link into or use for any public or commercial purpose this Site without the prior written permission of Muzinich. You must not transmit any virus, “worm”, “Trojan horse”, or other item of a destructive nature to this Site and it is your responsibility to ensure that whatever you download or select for your use from this Site is free from such items.

Nothing on this Site should be construed as granting any licence or right in relation to any of our trademarks or those of our affiliated companies. All trademarks, service marks, company names or logos are the property of their respective holders. The display of any trade names or trademarks on the Site does not imply that any licence has been granted to any third party in respect of the same. Any use by you of these marks, names and/or logos may constitute an infringement of the holders’ rights.

Third Parties

Muzinich and its affiliates shall have the benefit of the rights conferred on them by these Terms but otherwise no person who is not a party to these Terms may enforce its terms under the Contracts (Rights of Third Parties) Act 1999.

Applicable Law & Jurisdiction

These Terms and any non-contractual obligations arising from or connected with them shall be governed by and shall be construed in accordance with the laws of England and Wales.

You agree that the English courts shall have exclusive jurisdiction in relation to any legal action or proceedings arising out of or in connection with these Terms (whether arising out of or in connection with contractual or non-contractual obligations) (“Proceedings”) and waive any objection to Proceedings in such courts on the grounds of venue or on the grounds that Proceedings have been brought in an inappropriate forum. You further agree that this paragraph operates for the benefit of Muzinich and its affiliates and accordingly Muzinich and its affiliates shall be entitled to take Proceedings in any other court or courts having jurisdiction.

Amendment

Muzinich may delete or make changes to these Terms and to the information contained on this Site at any time. Where we make any changes to these Terms, you will be required to accept such changes in order to continue to use the Site. If you do not accept such revised Terms, you may no longer be able to access this Site.

If any provision of these Terms is found by any court or authority of competent jurisdiction to be illegal, void or invalid under the laws of any jurisdiction, the legality, validity or enforceability of the remainder of these Terms in that jurisdiction shall not be affected and the legality, validity and enforceability of the whole of these Terms in any other jurisdiction shall not be affected.

Contact Us

If you have any enquiries in relation to this Site or the information on it, please contact Muzinich at funds@muzinich.com or by calling +44 (0) 207 612 8755.

By clicking “I Agree” you:

(i) expressly acknowledge that you have read and understood the Terms and agree to abide by them;

(ii) represent, warrant and undertake that you are a not resident in the United States of America; and

(iii) confirm that you are accessing this Site in compliance with applicable laws and regulations of the jurisdiction or country in which you are residing.

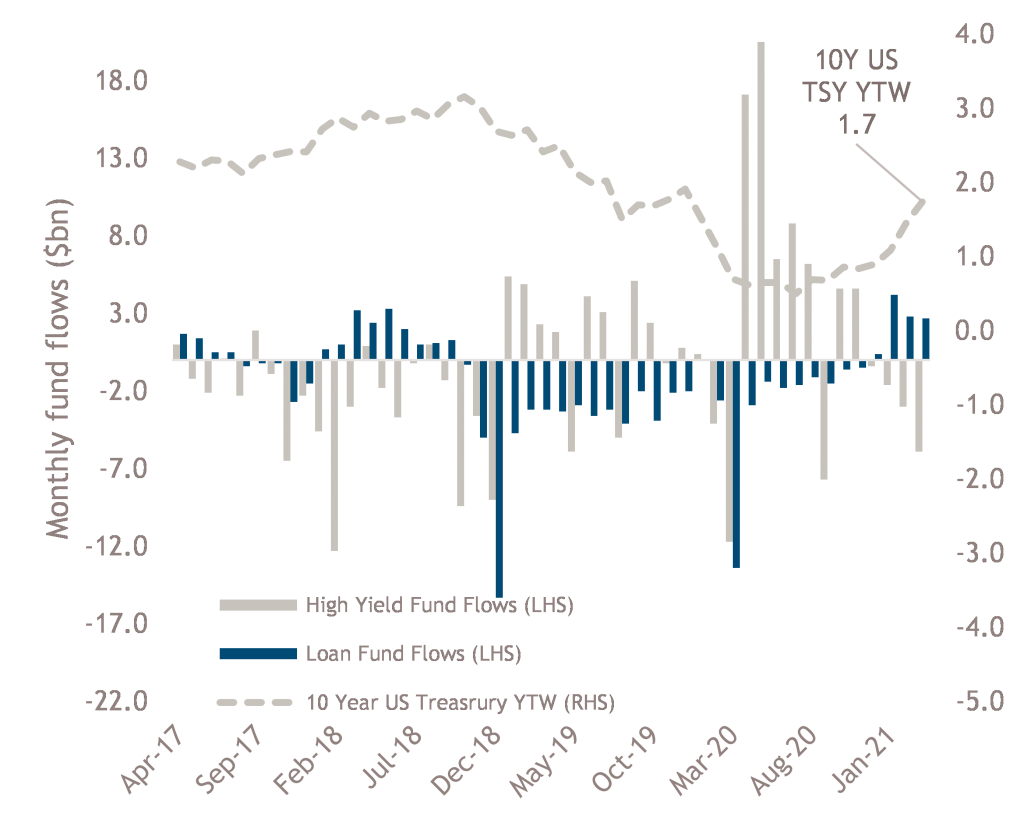

Source: JP Morgan High Yield Bond and Leveraged Loan Market Monitor, ICE BofA ML Current 10-Year US Treasury Index (GA10). As of March 31st, 2021

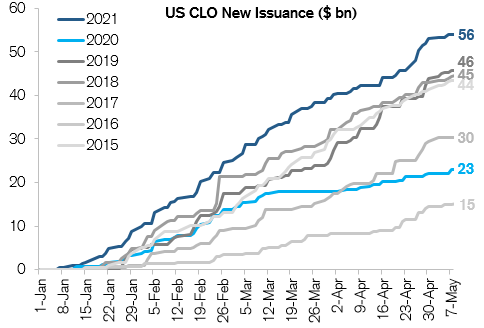

Source: JP Morgan High Yield Bond and Leveraged Loan Market Monitor, ICE BofA ML Current 10-Year US Treasury Index (GA10). As of March 31st, 2021 Source: Credit Suisse, LCD, as of May 12th, 2021

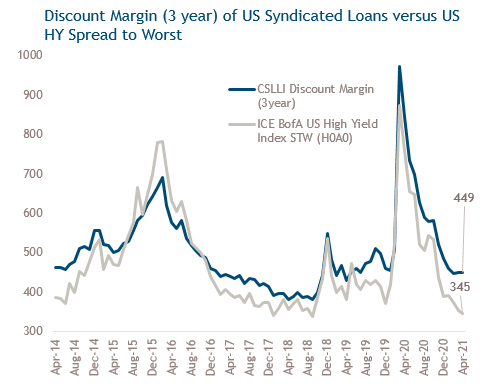

Source: Credit Suisse, LCD, as of May 12th, 2021 Source: Bloomberg and Credit Suisse Leverage Loan Index (CSLLI). Data as of April 30, 2021. ICE BofA ML US Cash Pay High Yield Constrained Index (JUC4).

Source: Bloomberg and Credit Suisse Leverage Loan Index (CSLLI). Data as of April 30, 2021. ICE BofA ML US Cash Pay High Yield Constrained Index (JUC4).