Insight | July 28, 2021

Accessing Opportunities in Asia Pacific Private Debt

While private debt is firmly embedded in the US and Europe, the asset class is playing catch up in the Asia Pacific region, offering a raft of potential opportunities for investors looking for higher yields and protection from interest rate risk.

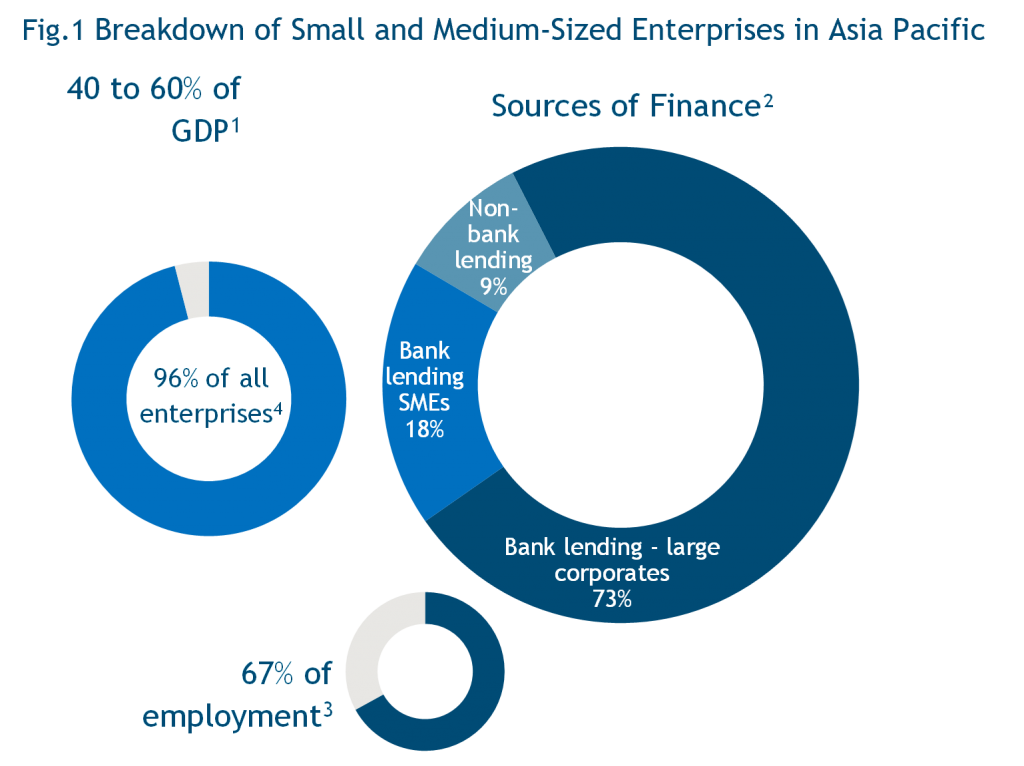

The Asia Pacific region is home to around 150 million small and medium-sized enterprises (SME).1 However, disproportionately, they only benefit from approximately 20% of all bank lending. In a similar vein to the US and Europe, Asia middle-market companies are underserved by lenders due to regulatory changes.

Sources:1 -Asia Pacific Economic Cooperation (APEC) Policy Support Unit Report titled: Overview of the SME Sector in the APEC Region: Key Issues on Market Access and Internationalization as of April 2020. 2 - McKinsey, Asia Pacific Banking Review, 2019. SMEs are those with EBITDA range between USD$5-50 mn. 3 - Asian Development Bank, The Role of SMEs in Asia and their difficulties in accessing finance, December 2018. 4 - Private Credit in Asia Report 2020 by Alternative Credit Council.

Sources:1 -Asia Pacific Economic Cooperation (APEC) Policy Support Unit Report titled: Overview of the SME Sector in the APEC Region: Key Issues on Market Access and Internationalization as of April 2020. 2 - McKinsey, Asia Pacific Banking Review, 2019. SMEs are those with EBITDA range between USD$5-50 mn. 3 - Asian Development Bank, The Role of SMEs in Asia and their difficulties in accessing finance, December 2018. 4 - Private Credit in Asia Report 2020 by Alternative Credit Council.

Post-Pandemic Financing Need

A joint report released in 2017 by the International Finance Corporation (IFC) and SME Finance Forum estimated that SMEs in Asia face a funding gap of around US$2trillion, a sum we believe is likely to increase due to the global pandemic. 2

We are focused on the middle market (i.e., companies with EBITDA of between USD$5-50mn) and where we believe there is less competition with a greater ability to get better deal terms and covenants.

In this segment, we are seeing a reduction of risk appetite by banks to make new loans to middle-market companies along with an increased willingness to dispose of existing non-core, middle-market loans.

We are encountering middle-market companies who are either not able to get bank financing, or only short-term working capital financing from banks. In the case of the latter, such financing is typically only made available when they allow the banks to take security against accounts receivables from their largest, most credit worthy international customers.

These companies are not able to get term financing for growth, capital expenditure, business expansion or acquisition, or even to help turn their business around.

This is where private debt from alternative lenders comes in to fill the lending gap, with the ability to provide term financing in the 2-5 year tenor range to help these companies reach their growth potential.

We believe there is a raft of opportunities for specialist, middle-market lenders. Pipelines appear healthy, and we expect we will continue to see good supply dynamics for new middle-market loans across the region. We are already seeing an increase in companies considering private debt as a financing alternative.

This is not just as an alternative to traditional bank lending, but even as a cheaper alternative to raising equity capital, especially for example with entrepreneurs who might not be as willing to dilute their holding in a company.

There is also the opportunity to replace existing bank lending to SMEs where the banks are looking to exit, not for credit reasons, but due to requirements to reduce risk and increase return on risk weighted assets (RWA).

Middle-market companies tend to take up more regulatory capital and therefore drag down the return on RWA calculations for banks.

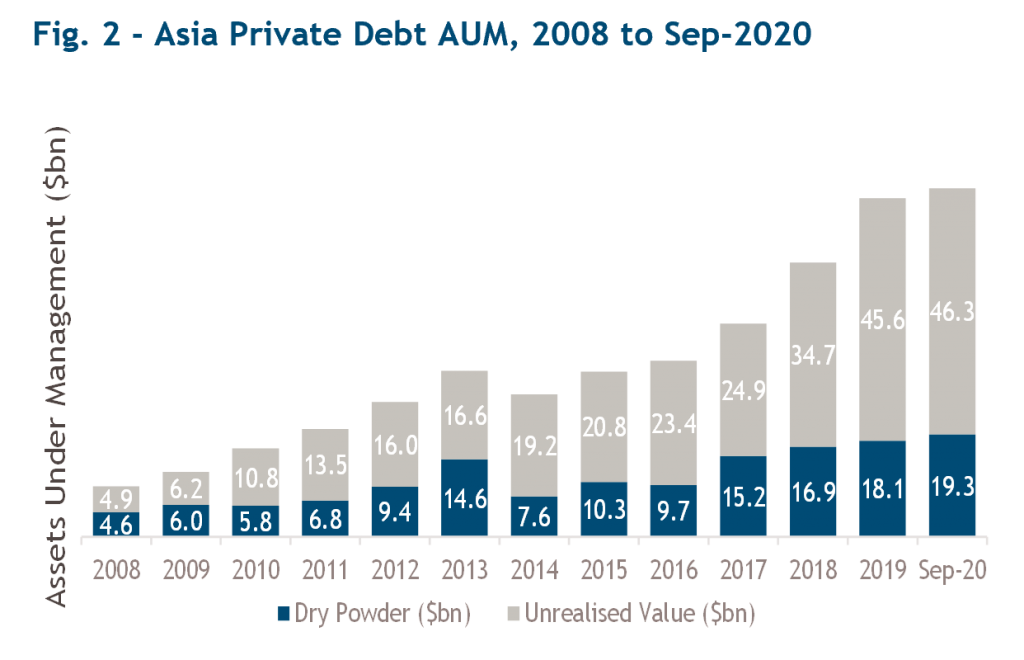

We believe private debt can bridge this funding gap and the asset class is starting to gain traction in the region. In 2020, the Asia Pacific private debt assets under management totaled US$65.6bn versus US$595.6bn in the US and US$289.5bn in Europe.3

Overall, we have seen a 15% per annum growth rate in private debt AUM in the region since 2014. We expect this trend to continue and for growth to pick up further, similar to the experience in Europe and the US.

Source: Preqin, as of May 2021. Reference to $ is USD.

Source: Preqin, as of May 2021. Reference to $ is USD.

Asia Pacific versus US and Europe

There are differences in the Asia Pacific region compared to the US and Europe. Firstly, the Asia Pacific private debt market is still in the early stages of its growth trajectory, therefore, in our opinion, there is less competition, and it is more fragmented.

Local funds are focused on specific markets while international funds, not specialised in Asia, are only looking for larger deals.

In terms of structures, we generally aim for a security package which is a combination of shares and hard assets that are at times complemented by corporate or personal guarantees.

There is also room for collateral top-up mechanisms where lenders require more collateral or cash to maintain a minimum of, for example, 2.5x collateral coverage on our lending.

The overarching theme is to be able to make use of structures to mitigate some of the perceived risk in Asian jurisdictions. In Asia, we have seen covenant discipline, particularly financial covenants.

Covenant-lite transactions are not usual practice. We also typically have review events in place should anything unusual arise such as a potential loss of a major contract or customer, where we can work with the company early on to find a solution.

Net Leverage Ratios tend to be in the 3-5x EBITDA range. The average tenor of the loan is also shorter at around 2-3 years compared to 5-7 years in Europe/US. CAPEX cycles are generally shorter in Asia, allowing us to incorporate principal amortizations into the structures.

In the jurisdictions in which we operate, liens and the enforcement of collateral is possible.

Environmental, Social and Governance Considerations

As lenders, we believe it is critical to have an in-depth understanding of the risks and opportunities facing the businesses to which we lend.

This is as much about the financial circumstances of a business as the way it manages environmental, social and governance (ESG) factors. We believe companies with robust governance structures and policies, with engaged workforces, and the ones which manage their environmental impacts well are more likely to be financially resilient over longer time horizons.

Historically, while a certain degree of ESG consideration has likely been part of most lenders’ due diligence procedures, ESG due diligence and ongoing monitoring is only now coming to the fore as a key element of best practice.

ESG considerations in Asia Pacific middle market companies are not always straight forward to comprehend and are typically context specific.

With patience and careful diligence, we work on applying ESG frameworks such as the Sustainability Accounting Standards Board (SASB) Materiality Map to identify the ESG issues most relevant to financial performance in specific industries.

Questions we ask as part of our diligence for example are: Does the business have good strong financial and operating controls? Will the sponsor be introducing an independent chairman? Does the company have robust backup procedures or disaster recovery plans, and how is the company addressing local environmental laws?

Our findings are summarized into an ESG scorecard to cover ESG considerations that can include transparency and accountability, anti-bribery and corruption, climate change, environmental degradation, employee engagement and welfare, equitable stakeholder interactions, diversity and inclusion and any UN Sustainable Development Goals that would specifically be supported by Company actions/measures.

These findings are incorporated into our investment memorandums and are key items in investment committee decision making in the Asia Pacific.

Conclusion: Financing Gap Creates Opportunities

The Asia Pacific region is home to a large and growing middle market with an estimated US$2 trillion financing gap.4

Private debt is still in its early stages of growth and is therefore less competitive than the US and Europe, offering the opportunity to take advantage of a fragmented and underserved market.

The region can offer good credit quality and collateralised security packages, and we believe we can look to achieve higher, risk-adjusted returns than other regions.

Risks can be mitigated with transactions having good covenant protection and deals being shorter dated. Overall, we believe the private debt opportunity in Asia looks set to continue its growth trajectory and we continue to see a lot of demand from companies and sponsors seeking financing.

All things considered, over a year into the COVID-19 pandemic, we are seeing a number of good opportunities emerge from several themes: the middle-market funding gap, banks de-risking, certain sectors being able to reposition their business in response to COVID-19 conditions, and even some benefiting from this unfortunate event.

We believe that it is a potentially attractive time to start deploying capital into the private debt markets to capture these opportunities that have emerged to achieve what we believe compelling risk-adjusted returns in Asia Pacific.

1. Asia Pacific Economic Cooperation (APEC) Policy Support Unit Report Titled: Overview of the SME Sector in the APEC Region: Key Issues on Market Access and Internationalization as of April 2020.

2. International Finance Corporation (IFC) World Bank Group, Micro, Small and Medium Enterprises (MSME) Finance Gap Report 2017. Most recent data used.

3. Preqin, as of May 2021. Reference to $ is USD.

4. IBID

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co are as of June 2021 and may change without notice.

Important Information

Muzinich & Co. referenced herein is defined as Muzinich & Co., Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. This material and the views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity; they are for information purposes only. Opinions and statements of financial market trends that are based on market conditions constitute our judgement as at the date of this document. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Certain information contained herein is based on data obtained from third parties and, although believed to be reliable, has not been independently verified by anyone at or affiliated with Muzinich and Co., its accuracy or completeness cannot be guaranteed. Risk management includes an effort to monitor and manage risk but does not imply low or no risk. Issued in the European Union by Muzinich & Co. (Dublin) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland No. 625717. Registered address: 16 Fitzwilliam Street Upper, Dublin 2, D02Y221, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2021-06-25-6667