Paid to wait: double-digit income at a discount in BDCs

Insight

May 28, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

Market volatility has created a compelling entry point in Business Development Companies (BDCs), where discounted valuations and resilient fundamentals offer liquid access to private credit, although selective, active allocation remains critical argues Ji He.

At a time when investors are seeking both reliable income and flexibility, BDCs offer a distinctive proposition:access to private credit returns without sacrificing liquidity. By combining the income-generating characteristics of private debt with the tradability and transparency of listed equities, BDCs bridge the gap between public and private markets – providing a compelling solution in an uncertain investment landscape.

A liquid approach to private debt

Business Development Companies (BDCs) act as a close-end, regulated vehicle for investors to access the private credit market, often specializing in lending to small and mid-sized US businesses. Public BDCs are publicly listed, closed-end investment vehicles with daily liquidity and no minimum investment requirements. As closed-end structures listed on stock exchanges, they benefit from permanent capital and are not subject to investor redemptions, enabling them to invest in less liquid assets without the risk of forced selling. At the same time, their public listing allows shares to trade on exchanges, offering investors daily liquidity and transparent pricing. This hybrid structure means underlying returns are largely income-driven, while share prices may exhibit equity-like volatility.

Established under US regulation, BDCs operate as Regulated Investment Companies and must distribute at least 90% of their income, resulting in structurally high dividend yields. This allows them to avoid corporate-level taxation, effectively passing income through to investors, although distributions are typically taxed as ordinary income. In addition to providing capital, BDCs often take an active role in supporting portfolio companies through oversight and strategic guidance.

Their investments are typically floating-rate, senior secured loans, positioned at the top of the capital structure. This aims to provide stable income, downside protection and resilience in rising rate environments, supported by strong access to company-level information and robust covenant structures.

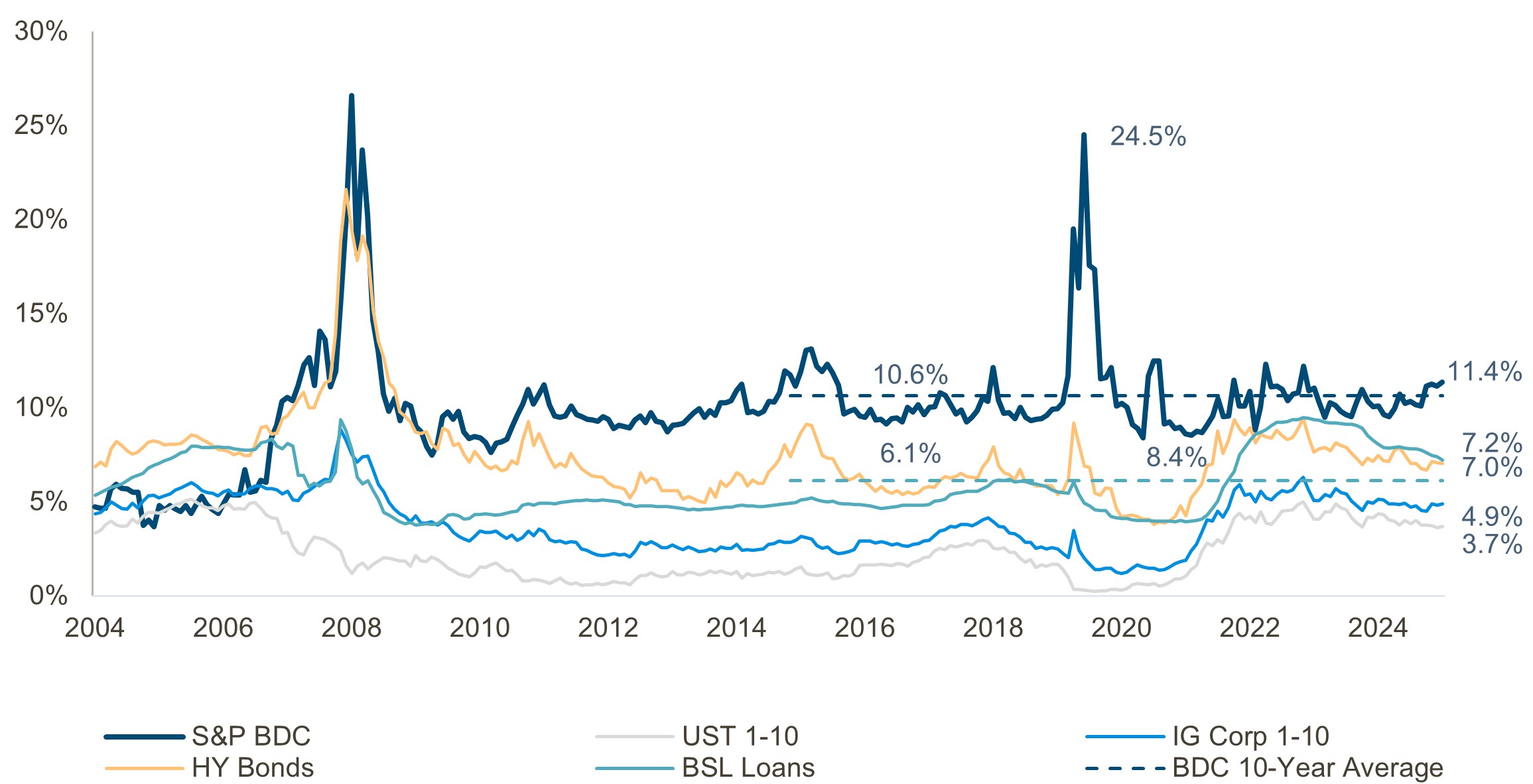

Returns in BDCs are primarily driven by income generation. Investors receive regular dividend distributions supported by contractual interest payments and fee income. As of March 2026, the S&P BDC Index offered a dividend yield of approximately 11.7%,1 significantly higher than broadly syndicated loans at 7.11%.2 Over the past decade, BDCs have consistently delivered high levels of income, with average annual payouts exceeding 10%,3 helping to cushion total returns during periods of market volatility.

BDCs occupy a unique position within the private credit ecosystem, offering liquid access to middle-market lending – a segment that has expanded significantly as banks have retreated and private equity demand has increased. The public BDC market has grown at a compound annual growth rate of over 10% over the past two decades, reflecting sustained investor demand for income-generating assets. 4

Figure 1 – Dividend yield

Information included above does not reflect actual investment results and is not a guarantee of future results. Results may vary with each use and over time.

Source: Muzinich, S&P Capital IQ, Bloomberg, Pitchbook. For illustrative purposes only. Charts generated April 2026, utilizing available data up to March 2026. Indices/Terminology: S&P BDC/BDC (S&P BDC Index), UST 1-10 (G502-ICE BofA U.S. Treasury 1-10), IG Corp 1-10 (C5A0-ICE BofA 1-10 Investment Grade Corporate), HY Bonds/HYB (J0A0-ICE BofA High Yield), Broadly Syndicated Loans/BSL (Pitchbook LCD Leveraged Loan), Horizon: December 2024 to December 2025. The S&P BDC index was launched in 2013 with data available via Bloomberg starting in 2014. Back-tested data based on index methodology from 2004 to 2014 is available via S&P. See p.6 for full index descriptions.

Diversification is another key benefit. A portfolio of BDCs typically include exposure to thousands of underlying borrowers across sectors and industries, with the aim of reducing idiosyncratic risk and enhancing portfolio resilience.

Unlike traditional private credit funds, which often involve long lock-ups and delayed capital deployment, BDCs provide immediate exposure to an established portfolio and generate income from day one. From an investment perspective, they seek to offer attractive yields, floating-rate protection, daily liquidity, and broad diversification across borrowers, sectors and industries, enhancing overall portfolio resilience.

Attractive entry point

We believe the current environment presents a favourable backdrop for BDCs. Valuations have come under pressure, with the S&P BDC Index trading at 0.86x price-to-book and yielding around 11.7%.5 These levels are comparable to those seen during the onset of the Federal Reserve’s tightening cycle in 2022, despite a less severe macroeconomic backdrop today.

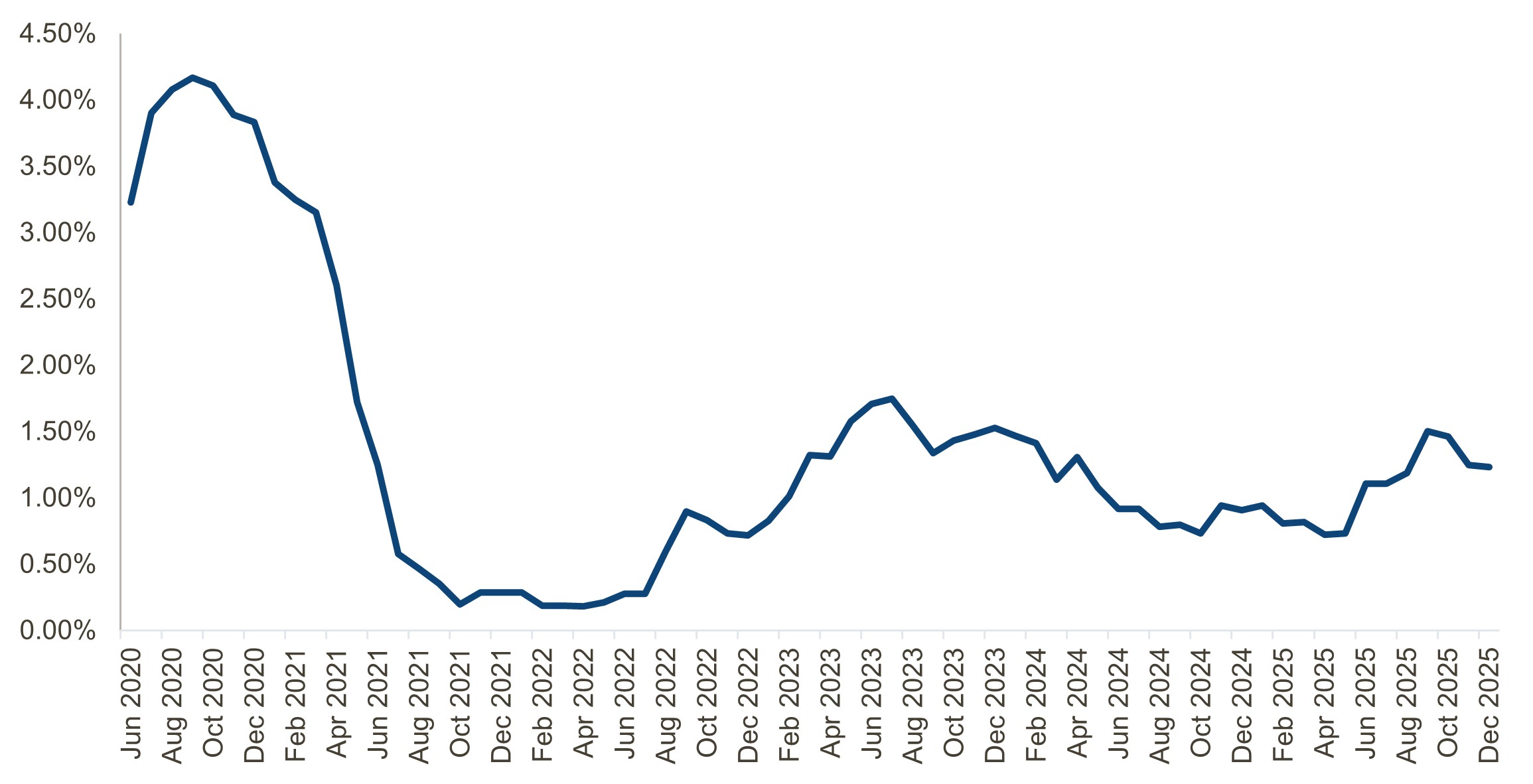

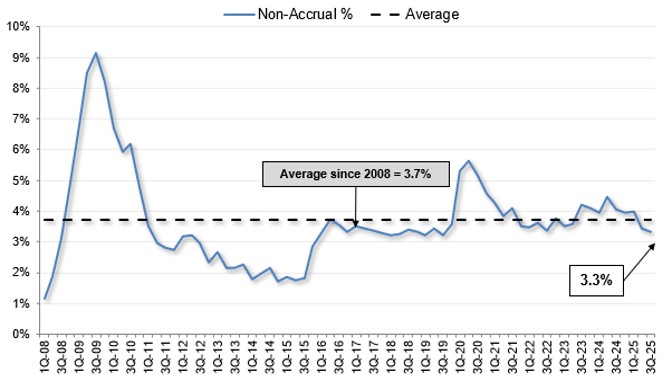

Non-performing loans are ticking upward from cyclical troughs but remain well-contained. Default rates in leveraged loans are low by historical standards,6 and non-accrual levels (loans missing interest payment over 90 days) within BDC portfolios are below long-term averages.7 While earnings have been somewhat pressured by lower rates and isolated credit issues, we believe he overall health of the asset class remains intact.

Figure 2 – US leveraged loan default rates at low levels

Source: Pitchbook S&P LCD, as of December 31st, 2025. For illustrative purposes only.

Source: Pitchbook S&P LCD, as of December 31st, 2025. For illustrative purposes only.

Figure 3 – Low non-BDC accrual rate

Source. KBW research, based on all public BDC company earnings reports in 3Q’25, as of January 6th, 2026. Latest available data used. For illustrative purposes only.

At the same time, performance dispersion across BDCs is increasing. Differences in underwriting standards, sector exposure and portfolio construction are becoming more pronounced, making manager selection a critical driver of returns.

Headlines versus reality

Recent market volatility has been driven by several high-profile concerns, many of which we believe appear overstated. Fraud-related anxieties following isolated incidents in leveraged lending have weighed on sentiment, but these events were confined to bank-originated loans and do not reflect broader trends in private credit. Similarly, concerns about artificial intelligence disrupting the software sector have contributed to equity market volatility, but diversified BDC portfolios mitigate concentration risk.

Liquidity concerns have also been a focus, particularly in relation to semi-liquid private credit vehicles. However, these issues do not apply to publicly listed BDCs, which trade on exchanges and operate with permanent capital structures. Even in private markets, mechanisms such as redemption gates are designed to prevent forced selling and protect investor interests.

Stress testing can further reinforce the resilience of the asset class. Even under extreme assumptions of elevated defaults and zero recovery, the impact on net asset value appears manageable and is largely reflected in current market pricing.

In our view, the risk of a systemic liquidity event driven by BDCs remains low. The sector operates with modest leverage, with regulatory cap at 2x and typically operating at around 1x, significantly below levels seen in banks or CLO structures. We believe this conservative approach provides a buffer against market stress and limits the potential for forced deleveraging.

Building resilient portfolios

Given the increasing dispersion across BDCs, we believe active management is essential. Performance differences are driven by credit quality, portfolio composition, dividend sustainability and management discipline. As a result, a selective approach, focused on downside protection and strong underwriting, is critical.

Diversification plays a central role in risk mitigation. Well-constructed portfolios can achieve exposure to thousands of underlying companies across sectors and geographies, reducing concentration risk. In our view, engagement with management teams and ongoing monitoring of credit conditions further enhance risk management.

Unlocking income and opportunity

Our outlook for BDCs remains constructive. Valuations are attractive, income levels are elevated and underlying credit fundamentals remain broadly stable. While macro uncertainty and geopolitical risks persist, these factors appear largely reflected in current pricing. Potential catalysts for improvement include credit spread widening, a recovery in M&A activity, supporting deal flow and fee income, alongside continued resilience in credit markets.

At the same time, increasing dispersion across the sector is likely to remain a defining feature, reinforcing the importance of selective, actively managed exposure focused on underwriting quality and downside protection.

Within a portfolio, BDCs can serve as a high-income complement to traditional fixed income, offering differentiated return drivers and exposure to private credit in a liquid format. While their listed structure introduces some equity-like volatility, their income profile and diversification across underlying borrowers can enhance overall portfolio resilience. They also offer the liquidity of listed equities, providing investors access to private credit through a transparent, daily traded structure.

In this context, we believe BDCs offer a compelling combination of attractive income, liquidity and access to private markets. Volatility has created an opportunity rather than signalling a structural shift in fundamentals, making the asset class a relevant consideration for investors seeking both income and diversification in today’s environment.

References

1. S&P BDC Index, as of 30th April 2026.

2. Pitchbook Morningstar Leveraged Loan Index, as of 30th April March 2026. Effective yield.

3. S&P BDC Index, as of 31st March 2026, from December 2014 to December 2025.

4. Keefe, Bruyette & Woods (KBW) Research and market data as of 2nd January 2026. Latest available data used.

5. S&P BDC Index, as of 30th April 2026.

6. Pitchbook S&P LCD, as of December 31st, 2025.

7. KBW research, based on all public BDC company earnings reports in 3Q’25, as of January 6th, 2026.

--------

Index description

S&P BDC Total Return Index - The S&P BDC Total Return Index (SPBDCUT) is a float adjusted, capitalization-weighted Index that is intended to measure the performance of all Business Development Companies that are listed on the New York Stock Exchange or NASDAQ and satisfy specified market capitalization and other eligibility requirements.

MSCI Russell 1000 - The Russell 1000 Index is a subset of the Russell 3000 Index that includes approximately 1,000 of the largest companies in the US equity universe. Constructed using a transparent, rules-based methodology, the Russell 1000 Index is designed to provide unbiased representation of the large cap segment of the US equity market.

C5A0 – ICE BofA 1-10 Year US Corporate Index is a subset of ICE BofA US Corporate Index including all securities with a remaining term to final maturity less than 10 years. Additional sub-indices are divided by ratings AAA through BBB. C0A0 – ICE BofA US Corporate Index tracks the performance of US dollar denominated investment grade corporate debt publicly issued in the US domestic market. Qualifying securities must have an investment grade rating (based on an average of Moody’s, S&P and Fitch), at least a year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million.

G5O2 – ICE BofA 1-10 Year US Treasury Index is a subset of ICE BofA US Treasury Index including all securities with a remaining term to final maturity less than 10 years.

J0A0 - The ICE BofA US Cash Pay High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt, currently in a coupon paying period that is publicly issued in the US domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million.

Pitchbook LCD Leveraged Loan - The Pitchbook LCD US Leveraged Loan Index is a market-value weighted index designed to measure the performance of the US leveraged loan market. Additional sub-indices are divided by ratings BBB through CCC.

Important information

Muzinich and/or Muzinich & Co. referenced herein is defined as Muzinich & Co., Inc. and its affiliates. Muzinich views and opinions. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall.

Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only.

This discussion material contains forward-looking statements, which give current expectations of future activities and future performance. Any or all forward-looking statements in this material may turn out to be incorrect. They can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Although the assumptions underlying the forward-looking statements contained herein are believed to be reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurances that the forward-looking statements included in this discussion material will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Further, no person undertakes any obligation to revise such forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

United Arab Emirates (UAE): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the UAE. It is intended solely for Professional Investors and should not be relied upon by any other person. This material has not been reviewed or approved by the UAE Securities and Commodities Authority, the UAE Central Bank or any other relevant authority. Nothing contained herein constitutes investment, legal, tax or other professional advice. Recipients should make their own independent assessment where appropriate.

Abu Dhabi Global Market (ADGM): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the ADGM. It is intended solely for Professional Clients (as defined by the Financial Services Regulatory Authority) and should not be relied upon by any other person. This material has not been reviewed or approved by the Financial Services Regulatory Authority or any other relevant authority in the UAE.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-05-19-18530

By clicking "Submit", I am (i) signing up to receive the Opinion Pieces from the "Opinions" page of the Muzinich & Co website, (ii) representing that the above information is true and accurate and (iii) agreeing to join the Muzinich & Co mailing list. I understand that Muzinich & Co will not add retail investors or individuals with personal email addresses to its mailing list and represent that I am not a retail investor. By providing my personal and professional information I am consenting to its use and disclosure in accordance with the Muzinich & Co. Privacy Policy. I understand that I may withdraw my consent and unsubscribe from receiving future communications by clicking "Unsubscribe" from the emails that are sent to me from Muzinich & Co.