Analysis | January 31, 2020

Some Thoughts on Coronavirus (2019-nCov) - January 2020

What impact is the outbreak in China likely to have on the global economy and financial markets?

The World Health Organisation has just declared the coronavirus outbreak in China a global emergency, and the virus is impacting financial markets.1

While financial markets do not reflect the tragic human cost, they are assessing the speed at which the disease is spreading, its impact on the Chinese economy and the possibility of global reach if containment measures fail.

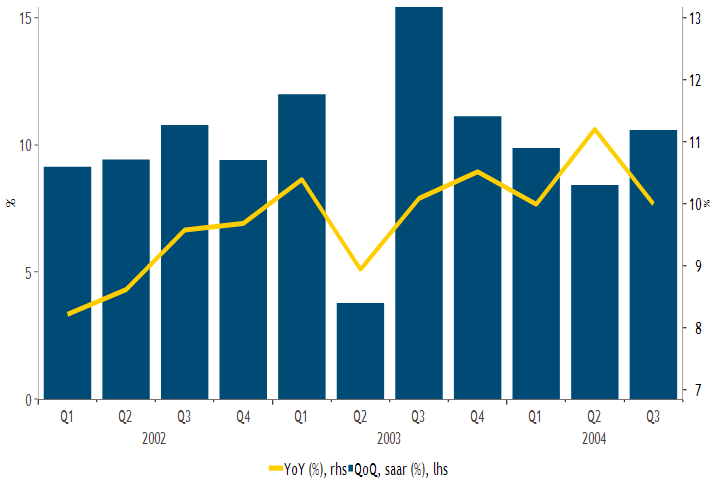

It is difficult to estimate the severity of the economic impact as the disease is still in progress. The first stage of a virus outbreak hits demand. The effect can be rapid, as seen in the 2003 SARS outbreak where GDP was rising at 12% on a quarter-on-quarter annualised basis in Q1 but, during Q2 slowed to 3.7% (Fig. 1).2

Fig 1: China GDP changes, Quarter-on-Quarter Annualized and Year-on-Year

Source: Macrobond, National Bureau of Statistics, as at 30 September 2004 (YoY – Year-on-Year, QoQ – Quarter-on-quarter, seasonally adjusted annual rate)

Source: Macrobond, National Bureau of Statistics, as at 30 September 2004 (YoY – Year-on-Year, QoQ – Quarter-on-quarter, seasonally adjusted annual rate)

In our view, most of this fall was demand driven. However, a demand-driven impact during a short period can have a high probability of a quick recovery. Indeed, by the third quarter of 2003, GDP growth rebounded to 15.5% quarter-on-quarter annualised, thanks to a large recovery in private consumption.3

The transmission to the supply side occurs when containment measures stop workers from working and prevents the transportation of raw materials. This is happening now.4

In our view, the longer restrictions are in place, the greater the chance the impact on demand will transfer to the supply side, reducing the chance of a quick recovery in lost activity.

The Chinese economy looks very different today in terms of growth composition, with the service sector contributing 54% to GDP, more than 10 points higher than 2003.5

However, the government’s response has been much faster than in 2003. President Xi Jinping quickly acknowledged the severity of the issue in public, resulting in the rapid transmission of orders and significant budget spending towards containment measures and medical infrastructure.6

Potential Impact on the Global Economy

The globalisation of an impact on the Chinese economy should not be underestimated. China represents 18% of global GDP, an equivalent share of global exports and is more intertwined with global tourism today than in 2003. 7

The potential sources of transmission into the broader global economy are through a disruption on trade and an impact on financial markets.

In our view, it is reasonable to think that the global impact will likely be modest if the virus is quickly contained, but more difficult to avoid should the situation persist.

Taking SARS as a reference, the economic impact was short lived and most of what was lost in domestic activity recovered quickly as discussed above. In financial terms, risk assets performed well during and after the outbreak, particularly developed markets assets, as outlined below.

US and European equities rose by 30% and 36% respectively between mid-March and September 2003.8 Credit spreads tightened, and the US high yield spread to worst was cut by 260bps in the space of two quarters.9

Government bonds played their safe-haven role; Treasuries fell by almost 100bps between mid-March and Mid-June 2003, and the Bund yield was down by 81bps over the same period.10

Oil fell by more than 30%, despite the second invasion of Iraq in mid-March.11 The US dollar weakened from March to mid-June 2003, participating in the easing of financial conditions.12

Opportunities for Repositioning?

For market participants, the speed of China’s reaction has been considered as positive. In addition, we believe policy responses will be activated once they can be transmitted into the economy (i.e. as travel restrictions are lifted).

The People’s Bank of China could use further interest rate cuts and inject more liquidity with Reserve Requirement Rate cuts, while 2020 funding needs were already well advanced before the disease struck.

From a sector allocation perspective, we believe tourism, transportation, offline retail and offline gambling are likely to suffer, while healthcare, online retailers and online gambling are more likely to hold up under pressure.

The property sector may be affected at the margin, but it benefits from geographic diversification and low exposure to the epicentre of the virus outbreak, in our view.

Taking SARS 2003 as a reference, we believe investors may want to see through the short-term volatility, hedging risk via safe havens such as US Treasuries or gold.

However, the desire to deploy cash when valuations have improved may lead to a “buy the dip” mentality as investors seek a good entry point, which could also prevent credit spreads widening.

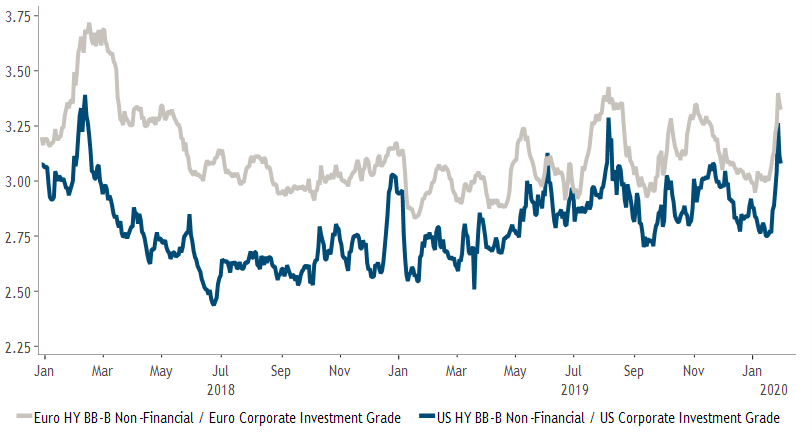

Fig. 2 - Ratio of High Yield/Investment Grade spread-to-worst, US and Euro Corporate Credit

Source: Macrobond, ICE BofA indices (HP4N, HC4N, C0A0, ER00 indices), as at 29th January 2020.

Source: Macrobond, ICE BofA indices (HP4N, HC4N, C0A0, ER00 indices), as at 29th January 2020.

1. S&P 500, Euro Stoxx 50, Generic US 10-Year Government Note, Generic German Government Bond 10-Year, West Texas Intermediate (WTI), as of 30 January 2020

2. Macrobond, National Bureau of Statistics, as at 30th September 2003

3. Macrobond, National Bureau of Statistics, as at 31st December 2003

4. https://www.straitstimes.com/asia/east-asia/wuhan-virus-china-to-extend-lunar-new-year-holidays-state-broadcaster-cctv-says

5. Macrobond, National Bureau of Statistics, JPMorgan report ‘Coronavirus update: Revising China’s growth forecast’, 29th January 2020

6. https://www.telegraph.co.uk/news/2020/01/24/watchchina-hastily-builds-new-1000-bed-hospital-wuhan-tackle/

7. https://www.imf.org/external/datamapper/PPPSH@WEO/OEMDC/ADVEC/WEOWORLD, World Bank, JPMorgan, as of January 29th, 2020

8. S&P 500 Index and Euro Stoxx 50 12th March 2003 - 23rd September 2003

9. ICE BofA US High Yield Index (J0A0) between 12th March - 12th September 2003

10. Generic US 10-Year Government Note, Generic German Government Bund 10-Year, 21st March - 13th June 2003

11. West Texas Intermediate (WTI) 12th March - 29th April 2003

12. US Dollar Index (USDX), as of 16th June 2003

----------------------------------------------------------------------------------------------------------------------------------

Important Information

"Muzinich & Co.", “Muzinich” and/or the "Firm" referenced herein is defined as Muzinich & Co., Inc. and its affiliates. This document has been produced for information purposes only and is not intended to constitute an offering, advice or recommendation to purchase any securities or other financial instruments. The investment strategies and themes discussed herein may not be suitable for investors depending on their specific investment objectives and financial situation. Investors should conduct their own analysis and consult with their own legal, accounting, tax and other advisers in order to independently assess the merits of an investment.

The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only, are as of the date of publication and are subject to change without reference or notification. Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or the actual performance of the securities, investments or strategies discussed may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained in this document may be relied upon as a guarantee, promise, assurance or a representation as to the future.

All information contained herein is only as current as of the date indicated and may be superseded by subsequent market events or for other reasons. Nothing contained herein is intended to constitute investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. Historic market trends and performance are not reliable indicators of actual future market behaviour or performance.

Certain information contained herein is based on data obtained from third parties and, although believed to be reliable, has not been independently verified by anyone at or affiliated with Muzinich & Co., Inc.; its accuracy or completeness cannot be guaranteed.

No part of this material may be reproduced in any form or referred to in any other publication without express written permission from Muzinich.

Issued in Europe by Muzinich & Co. Limited, which is authorised and regulated by the Financial Conduct Authority FRN: 192261. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ. Muzinich & Co. Limited is a subsidiary of Muzinich & Co., Inc. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

Index Descriptions

J0A0 - The ICE BofA ML US Cash Pay High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt, currently in a coupon paying period that is publicly issued in the US domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million.

C0A0 - The ICE BofA ML US Corporate Index tracks the performance of US dollar denominated investment grade corporate debt publicly issued in the US domestic market. Qualifying securities must have an investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million.

HP4N – The ICE BofA ML BB-B European Currency Non-Financial High Yield Constrained Index contains all non-financial securities in The ICE BofA ML European Currency High Yield Index rated BB1 through B3, based on an average of Moody's, S&P and Fitch, but caps issuer exposure at 3%.

ER00 – The ICE BofA ML Euro Corporate Index tracks the performance of EUR denominated investment grade corporate debt publicly issued in the eurobond or Euro member domestic markets. Qualifying securities must have an investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity, a fixed coupon schedule and a minimum amount outstanding of EUR 250 million.

ICE BofA BB-B US Non-Financial High Yield Constrained Index (HC4N) contains all securities in The ICE BofA US High Yield Index that are rated BB1 through B3, inclusive, except those of financial issuers, but caps issuer exposure at 2%.

West Texas Intermediate (WTI) crude oil is the underlying commodity of the New York Mercantile Exchange's oil futures contracts. WTI is an oil benchmark.

The US Dollar Index(USDX) indicates the general international value of the USD. The USDX does this by averaging the exchange rates between the USD and major world currencies. The ICE US computes this by using the rates supplied by some 500 banks.

S&P 500 - The Standard & Poor's 500 Index (S&P 500) is an index of 500 stocks seen as a leading indicator of US equities and a reflection of the performance of the large cap universe, made up of companies selected by economists.

SX5T - The EURO STOXX 50 Index is derived from the 19 EURO STOXX regional Supersector indices and represents the largest super-sector leaders in the Eurozone in terms of free-float market capitalization.

HP4N – The ICE BofA ML BB-B European Currency Non-Financial High Yield Constrained Index contains all non-financial securities in The ICE BofA ML European Currency High Yield Index rated BB1 through B3, based on an average of Moody's, S&P and Fitch, but caps issuer exposure at 3%.