Insight | May 6, 2020

Q&A - COVID-19 Impact on Emerging Markets - April 2020

How Would You Describe This Crisis?

How Would You Describe This Crisis?

The rapid global spread of COVID-19 and the subsequent lockdown measures have resulted in a global humanitarian and working capital crisis rolled into one event. The monetary and fiscal policy measures put in place by central banks and governments have acted to help soften the blow. These measures have been targeted to support businesses and workers, but also to stabilise global financial markets after one of the biggest selloffs since the Great Financial Crisis (GFC) of 2008. In our view, monetary policy is more effective as a tool to support working capital needs (as it can help efficiently to add liquidity into the financial system). While fiscal policy measures, (often seen as a slower-to-implement tool), can help to replace lost income for companies and workers and kick start economic and investment growth. In this crisis, the fiscal measures are more focused on providing income relief to those most affected by the pandemic.

What Are the Differences Between the Current Circumstances When Compared with the Great Financial Crisis (GFC)? Does It Make Sense to Compare Them?

In our view, the GFC was a banking crisis. This is not the case now; the banking system is currently part of the solution to provide businesses with support to sustain the sudden halt to economic activity as a result of the lockdown measures. We believe the banking system is in excellent health; one might even argue that the tighter regulations and restrictions imposed on banks since the GFC has helped strengthen them. In Emerging Markets, the banking system is being used as an important tool for counter cyclical policy, (while historically Emerging Markets would tighten monetary policy to support capital outflows and currency, but this is not the case today); as economic growth weakens monetary policy loosens. Furthermore, with the banking system fully functional, the primary market has already reopened, providing both sovereigns and corporates access to USD funding. This is in contrast with the GFC, during which USD funding was all but closed between September 2008 and January 2009 for EM. Year to date, we have seen a large amount of sovereign issuance from countries including Peru, Indonesia, Israel and Qatar as well as corporate new issuance.

Have We Seen the Lowest Prices Yet?

We do think we have seen the lowest prices yet, both because the speed and size of global support has been unprecedented, and also because we believe the global banking system and the private sector balance sheets are both in good shape. That said, if we attempt to break down the crisis into eight negative headlines, we are only just starting to concentrate on the third headline – the global Gross Domestic Product/earnings collapse. Based on this, it is possible that we are one third of the way through this crisis.

1.COVID-19 global acceleration

2.COVID-19 death count

3.Global GDP/earnings collapse

4.Banking non-performing loans/ defaults acceleration

5.Potential COVID-19 2nd wave

6.“L” shape, no recovery

7.“W” shape, spluttering recovery

8.Debt sustainability in Developed Markets

How Have EM Central Banks Responded to the Crisis?

We believe there has been global coordination to loosen monetary policy. If we look at global average interest rates, they fell from 2.0% in December 2019 to 1.3% at the end of March 2020¹. While, during the same period, Developed Markets (DM) GDP weighted fell from 0.7% to zero, Emerging Markets (EM) GDP weighted fell from 4.1% to 3.4%². However, in our opinion, EM could still have significant room to cut rates further if needed.

In our view, Quantitative Easing (QE) should be used when interest rates hit zero. Therefore, since we believe that EM have further room to cut interest rates (which have so far only been aggressively lowered by DM central banks) and since we know that QE carries the risk of debasing a currency (something EM sovereigns must guard against), it is no surprise that QE has not been the preferred tool to combat the current crisis. Within EM, Brazil is currently reviewing constitutional changes that will enable its Central Bank to buy debt (the combined liquidity measures if they are all sanctioned by the government will be equivalent to 16.7% of Brazil’s GDP³). Meanwhile, Colombia, Hungary and Indonesia have also started QE programmes.

The tools that the vast majority of central banks in EM use include cutting Required Reserve Ratio (RRR) and/or implement capital buffers. We view this as a far more effective tool than QE, as it instantly increases liquidity into the banking system, which can then cascade to the economy via lending to Small and Medium Enterprises (SMEs). Furthermore, to increase USD liquidity, central banks in EM have increased the size and eligibility of repo operations and applied for swap lines with the US and other major funding centres. One of the lessons learnt from the GFC, was the importance of maintaining US dollar liquidity. We believe this could be achieved by a combination of proactive swap line opening and a large accumulation of FX reserves.

In our view, EM central banks have acted decisively in providing support for bank liquidity, US dollar funding, and working capital support for companies. Furthermore, we believe that there is still room to do more if needed.

What Has Been the Fiscal Response In EM?

Firstly, regulation has seen many governments pushing counter cyclical lending and temporary forbearance on loans. This has been very common in Asia including India, China, Philippines, Singapore, Malaysia, and Indonesia, as well as in Russia, Turkey, and Mexico. Secondly, international bodies such the G20 (“Group of Twenty” refers to the international forum for governments and central banks from 19 countries and the European Union) have announced on April 15, 2020 a freeze on bilateral debt (both on principal and interest) servicing for the rest of 2020, beginning May 1. This should free up a significant amount of resources for the world’s least developed countries to fight COVID-19. The International Monetary Fund (IMF) has doubled the access to its emergency facilities (Rapid Credit Facility and Rapid Financing Instrument), which are designed to give access to funds without the need for a fully-fledged program in place, as of April 9, 2020. The IMF’s Executive Board has already approved 20 countries and demand is expected to raise up to $100bn⁴.

Fiscal support by EM sovereigns can be categorised into three groups (Based on Muzinich analysis as of April 27, 2020, supported by IMF Policy Responses to Covid-19 Report):

1.Limited fiscal room/preference for monetary response. Fiscal response 0% -2%; for example, Brazil, Russia, India, and Mexico.

2.Combined monetary and fiscal support. Fiscal response 2% - 6%; for example, Chile, Indonesia, Peru, Hungary and South Korea.

3.Limited monetary room. Fiscal response +10%; for example, Poland, Singapore, Czech Republic, South Africa and Malaysia

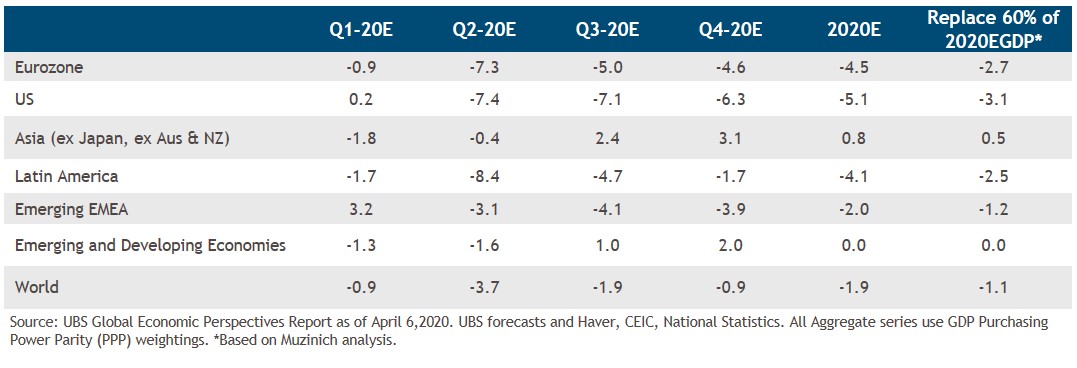

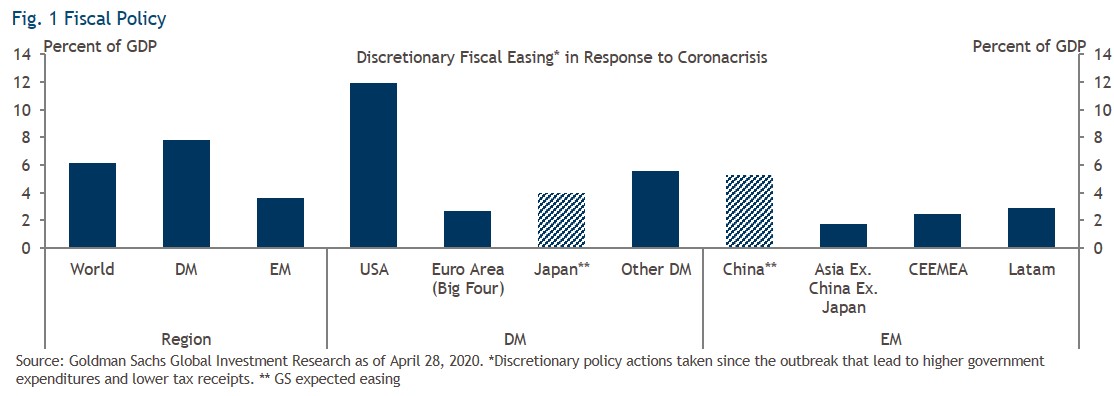

We believe the criticism of EM for its lack of fiscal response seems somehow harsh on an aggregate level. If we make an assumption that 60% of lost GDP for 2020 (as shown on the table on the next page) is private sector income that needs to be replaced by fiscal support, we can see that Latin America will likely be the EM region which needs the greatest support and Asia the least support. We believe the estimates of the amount of fiscal policy provided to cover this income falls short of what is likely to be needed. The US government has been the most aggressive in fiscal support, but we believe that this will come at a cost of a significant raise of debt to GDP (rising from 77% to 97% 2020E) Fig.1

What Type of Shape is EM Corporate Balances Sheets? What Is the Current State of Corporate Balance Sheets in EM?

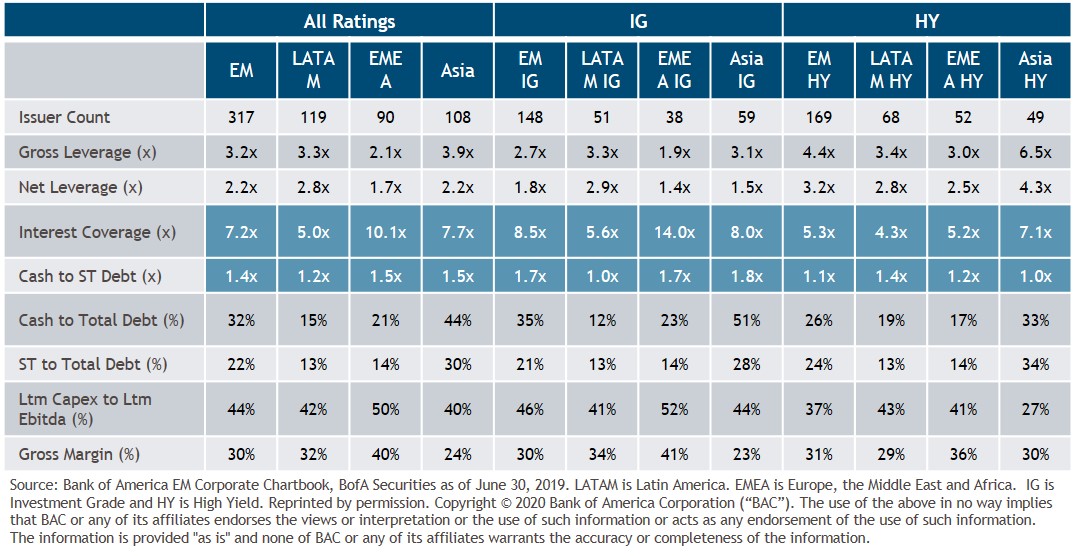

We believe EM corporate balance sheets look healthy. If this is a “working capital crisis”, then, in our view, the two most important ratios that we need to assess are interest cover and cash to short-term debt payments, as highlighted in the table below. No region has an interest rate cover below 2, so this would suggest that paying coupon isn’t really a concern in EM credit markets. If we look at the short-term debt to cash levels, they are tight in Latin America Investment Grade (IG) and Asia High Yield (HY) but do cover the next 12-month payments. In Latin America IG, we believe that one energy company distorted the figures. For Asian HY, the Chinese government has significantly loosened local liquidity and increased counter cyclical funding. In our view, the choice has increased with the dollar new issue market already opened for Asia HY, but believe it’s still cheaper to borrow onshore at present.

Should Investors Be Concerned With Weak Technicals In EM?

Net supply for 2020 is expected to be flat, in our view. If we review all the maturing debt for the next 12 months in the indices ICE BofA Emerging Markets Corporate Bond Index and ICE BofA Emerging Markets External Sovereign Index, we can see that EM corporate totals $161bn and EM sovereign totals $36bn. Year to date (YTD), the issuance of these indices up to April 27, 2020 for corporate and sovereign has been $161bn and $96.4bn respectively⁵. In our view, there really isn’t any great urgency for funding as it was done earlier in the year in EM and the primary market has already reopened.

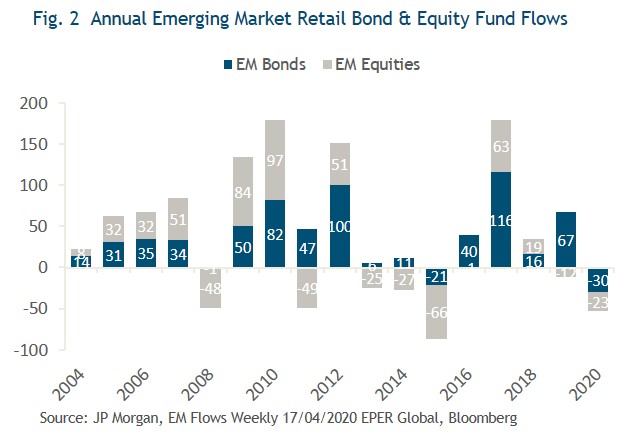

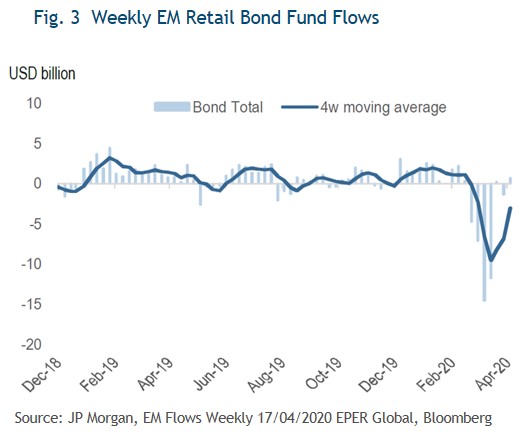

Outflows from EM fixed income assets have reached $30.5bn YTD (Fig.2)--similar to what the asset class experienced during the selloffs in both the 2013 –“Taper Tantrum” and the 2015 “Commodity Crisis”. We believe it is fair to say that “EM tourist” investors (defined as those investors who will leave the market at the first sign of volatility) have sold out at this point. Starting in April, the speed of outflows has significantly slowed down (Fig.3) and even turned positive with inflows.

Are EM Credit Valuations Cheap?

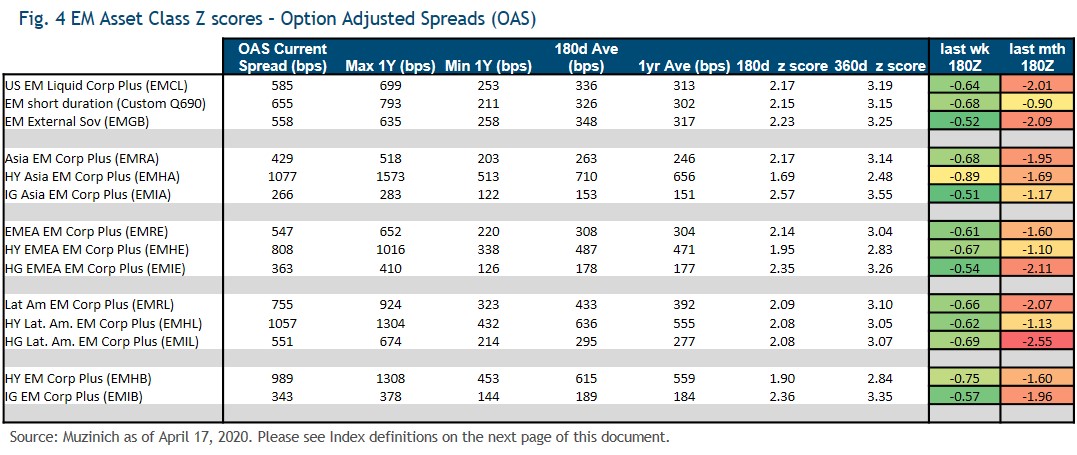

We believe EM valuations were at their widest levels on March 23,2020. Since then spreads have tightened, but still remain 3 on the Zscores (cheap on a 1-year basis) (Fig 4). We believe, EM valuations (spreadwise) have reached bottom. Although it is possible that we could revisit these levels, we have a constructive view of the asset class.

We believe that 2020 will see a recession due to the impact of the COVID-19 pandemic on global economic growth. Our consensus view is that the recession shock will be severe but temporary, and that there will likely be no permanent loss to potential output. Overall, we believe EM corporates look healthy, outflows have improved technical and valuations look attractive.

1.and 2. Source: UBS Global Economic Perspectives Report as of April 6, 2020.

3.Source: Reuters, Update 3-Brazil central bank chief Campos Neto not in favor of money- printing QE as of April 9,2020. https://www.reuters.com/article/brazil-economy-cenbank/update-3-brazil-central-bank-chief-campos-neto-not-in-favor-of-money-printing-qe-idUSL2N2BX1CK

4.Source: IMF Policy Responses to COVID-19 Report. Latest update as of April 24, 2020. https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19.

5. Source: Bank of America Merrill Lynch indices as of April 27,2020. Please see Index definitions on the next page of this document.

----------------------------------------------------------------------------------------------------------------------------------

Index Descriptions:

You cannot invest directly in an index, which also does not take into account trading commissions or costs. The volatility of indices may be materially different from the volatility performance of an account or fund.

EMGB – The ICE BofA Emerging Markets External Sovereign Index tracks the performance of US dollar and euro denominated emerging markets sovereign debt publicly issued in the major domestic and eurobond markets.

EMCL – The ICE BofA US Emerging Markets Liquid Corporate Plus tracks the performance of the U.S. dollar denominated emerging markets non-sovereign debt publicly issued in the major domestic and eurobond markets. Qualifying issuers must have risk exposure to countries other than members of the FX G10, all Western European countries, and territories of the U.S. and Western European countries.

Q690 – The ICE BofA ML Custom Emerging Markets Short Duration Index tracks the performance of short term US dollar and euro denominated emerging markets non-sovereign debt publicly issued in the major domestic and eurobond markets.

EMGB – The ICE BofA Emerging Markets External Sovereign Index Index tracks the performance of US dollar and euro denominated emerging markets sovereign debt publicly issued in the major domestic and eurobond markets. Qualifying securities must have risk exposure to countries other than members of the FX-G10, all Western European countries and territories of the US and Western European countries.

EMRA - ICE BofA Asia Emerging Markets Corporate Plus Index is the subset of the ICE BofAML Emerging Markets Corporate Plus Index, which includes only securities issued by countries associated with the region of Asia, excluding Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan, and Uzbekistan.

EMHA – The ICE BofA High Yield Asia Emerging Markets Corporate Plus Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BB1 and lower with a country of risk within the Asia region.

EMIA - The ICE BofA High Grade Asia Emerging Markets Corporate Plus Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BBB3 and higher with a country of risk within the Asia region.

EMRE - The ICE BofA EMEA Emerging Markets Corporate Plus Index is a subset of The ICE BofA Emerging Markets Corporate Plus Index including all securities issued by countries associated with the geographical region of Europe, the Middle East and Africa including Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan and Uzbekistan.

EMHE – The ICE BofA High Yield EMEA Emerging Markets Corporate Plus Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BBB3 and higher with a country of risk within the Europe, Middle East and Africa regions.

EMIE – The ICE BofA High Grade EMEA Emerging Markets Corporate Plus Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BBB3 and higher with a country of risk within the Europe, Middle East and Africa regions.

EMRL – The ICE BofA Latin America Emerging Markets Corporate Plus Index is a subset of The ICE BofA Emerging Markets Corporate Plus Index including all securities issued by countries associated with the geographical region of Latin America.

EMHL - The ICE BofA High Yield Latin America Emerging Markets Corporate Plus is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated sub-investment grade based on the average of Moody's, S&P and Fitch, and with a country of risk associated with the geographical region of Latin America.

EMIL - The ICE BofA High Grade Latin America Emerging Markets Corporate Index is a subset of ICE BofA Emerging Markets Corporate Plus Index including all securities rated BBB3 and higher with a country of risk within the Latin America region.

EMHB – The ICE BofA High Yield Emerging Markets Corporate Plus Index is a subset of the ICE BofA ML Emerging Markets Corporate Plus Index (EMCB) including all securities rated BB1 or lower.

EMIB – The ICE BofA High Grade Emerging Markets Corporate Plus Index is a subset of the ICE BofA ML Emerging Markets Corporate Plus Index (EMCB) including all securities rated AAA through BBB3, inclusive.

EMCB - The ICE BofA ML Emerging Markets Corporate Plus Index tracks the performance of the US dollar and euro denominated emerging markets non-sovereign debt publicly issued in the major domestic and eurobond markets. Qualifying issuers must have risk exposure to countries other than members of the FX G10, all Western European countries, and territories of the US and Western European countries.

----------------------------------------------------------------------------------------------------------------------------------

Important Information

"Muzinich & Co.", “Muzinich” and/or the "Firm" referenced herein is defined as Muzinich & Co., Inc. and its affiliates. This document is for informational purposes only and does not constitute an offer or solicitation of an offer, or any advice or recommendation, to purchase or sell any securities or other financial instruments and may not be construed as such. Past performance is not indicative of future results. The value of an investment, and income generated (if any) may fall as well as rise and is not guaranteed. All information contained herein is believed to be accurate as of the date(s) indicated, is not complete, and is subject to change at any time. Muzinich hereby disclaims any duty to provide any updates or changes to the analysis contained herein. Certain information contained herein is based on data obtained from third parties and, although believed to be reliable, has not been independently verified by anyone at or affiliated with Muzinich; its accuracy or completeness cannot be guaranteed. This document may contain forward-looking statements and/or forecasts, which give current expectations of the market’s future activities and future performance (“forward-looking statements”). Any or all forward-looking statements in this material may turn out to be incorrect. They can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Forward looking statements are based upon current beliefs and expectations and are for illustrative purposes only. Further, no person undertakes any duty or obligation to revise such forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Opinions and statements of financial market trends that are based on market conditions constitute our judgement and are subject to change without notice. Historic market trends are not reliable indicators of actual future market behavior. The above is not intended to provide a sufficient basis on which to make an investment decision and should not be construed as investment advice or an offer or solicitation of an offer. Investors should confer with their independent financial, legal or tax advisors. The above is neither independent investment research, nor is it an objective or independent explanation of the matters contained herein, and you must not treat it as such. No part of this material may be reproduced in any form or referred to in any other publication without express written permission from Muzinich.

Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability; heightened pricing volatility and reduced market liquidity. Rates of exchange may cause the value of an investment to rise or fall.

You cannot invest directly in an index, which also does not take into account trading commissions or costs. The volatility of indices may be materially different from the volatility performance of an account or fund.

Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a registered investment adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC. Issued by Muzinich & Co. Limited, which is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ.