Insight | May 6, 2021

Debt, Digital, Climate - May 2021

Are debt, digital and climate transforming central banking and the broader economy?

Central banking is facing three pressing challenges: debt, digital and climate. We believe the response to these challenges by the major central banks will change the nature of monetary policy and the role of central banking in the economy and society at large.

Debt

Since the 2007/2008 Great Financial Crisis (GFC), central banks have enriched the toolkit of monetary policy by introducing new non-standard instruments and enhancing existing ones. Among these unconventional policies, quantitative easing stands out. As defined by Ben Bernanke, “Quantitative easing involves central bank purchases of securities in the open market, financed by the creation of bank reserves held at the central bank.”1

Major central banks have engaged in quantitative easing (QE) in the years following the GFC and have made further, massive, recourse to this instrument in response to the COVID–19 pandemic. The Federal Reserve (Fed), European Central Bank (ECB), Bank of England and Bank of Japan have all undertaken quantitative easing.

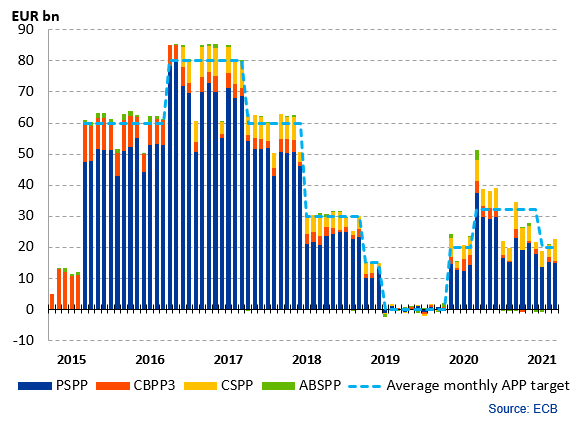

Fig. 1 – European Central Bank Asset Purchase Programmes

Source: ECB, Asset Purchase Programmes, https://www.ecb.europa.eu/mopo/pdf/APP_net_purchases_by_programme.png?hvt. The graph does not include the purchases under the PEPP, the purchase programme specifically established during the pandemic. (PSPP – public sector purchase programme, CBPP3 - third covered bond purchase programme, CSPP – corporate sector purchase programme, ABSPP – asset-backed securities purchase programme, APP – asset purchase programme.) As of 31 March 2021

Source: ECB, Asset Purchase Programmes, https://www.ecb.europa.eu/mopo/pdf/APP_net_purchases_by_programme.png?hvt. The graph does not include the purchases under the PEPP, the purchase programme specifically established during the pandemic. (PSPP – public sector purchase programme, CBPP3 - third covered bond purchase programme, CSPP – corporate sector purchase programme, ABSPP – asset-backed securities purchase programme, APP – asset purchase programme.) As of 31 March 2021

In the last decade, central bank balance sheets have grown dramatically. For example, the amount of bonds bought by the Eurosystem through its different programmes (APP and PEPP) stood at around €4000 billion in mid-April 2021.2

More than 75% of the securities owned by the ECB are government bonds, the purchase of which will continue at a substantive pace until at least the end of March 2022, further swelling its balance sheet.

Equally in April 2021 Fed-owned assets amounted to more than US$7700 billion, with a striking ninefold increase since early 2008.3

The ECB and Fed will end up owning between 25% and 30% of their governments’ debt, and the Bank of Japan over 40%.

Existential questions loom over this debt, well beyond contingent issues about the length of the extension to the current purchase programmes. Will central banks embark on its indefinite roll over, possibly extending the maturity? Will this debt eventually be made perpetual or even cancelled as has been proposed? In the case of the European Union, will the ECB progressively replace national debt with a supranational one issued by the Commission under programmes such as the Next Generation EU?

Each central bank has its own mandate, culture and practices and these questions can, possibly, find narrow, technical answers according to each jurisdiction.

However, there is a general interrogative on the long-term role that central banks will play vis-à-vis the increasing levels of government indebtedness and the rising amount of national debt which they own.

Perhaps we have not yet reached a time to fully answer these questions.

Digital

In recent years, we have seen an acceleration in the pace of digitalisation in all aspects of the economy and within society more broadly. A technological revolution is taking place: money could not remain unaffected.

Indeed, it is not the first-time money has undergone a radical technological transformation and each transformation, such as from gold coins to banknotes, has had its own challenges.

There is much confusion around the exact definition of the digitalisation of money. It is a notion that includes different phenomena such as electronic payment systems, the most successful being the digital wallets of China’s WeChat and Alipay; the emerging array of fiat cryptocurrencies, such as the popular bitcoin and “stablecoins” on blockchain; and the possibility of central banks issuing digital currencies.

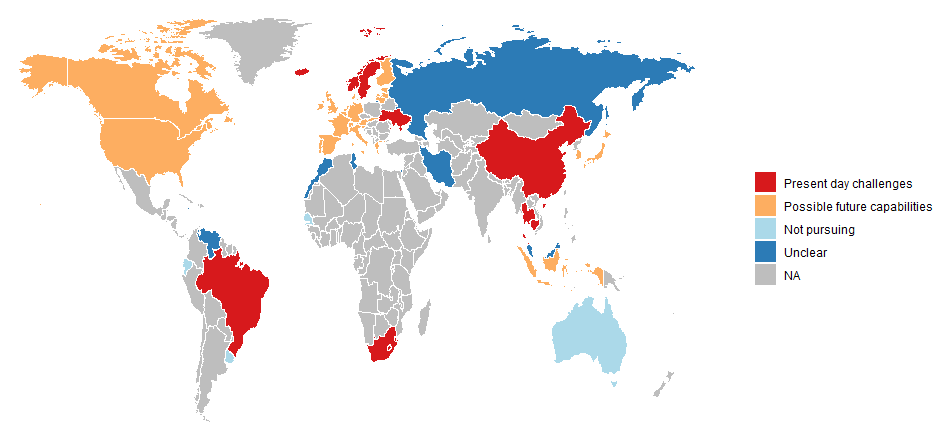

Central banks and governments globally are considering introducing central bank digital currencies (CBDCs), as shown in Fig. 2:4

Fig. 2 – Central Banks Considering Digital Currencies

Countries have been assigned one of five categories: (1) addressing a present day challenge, (2) exploring possible future capabilities, (3) not pursuing research and experimentation, (4) unclear motivations, and (5) not available.

Countries have been assigned one of five categories: (1) addressing a present day challenge, (2) exploring possible future capabilities, (3) not pursuing research and experimentation, (4) unclear motivations, and (5) not available.

Source: Jess Cheng, Angela N Lawson, and Paul Wong, Preconditions for a general-purpose central bank digital currency, Feds notes, 24 February 2021

https://www.federalreserve.gov/econres/notes/feds-notes/preconditions-for-a-general-purpose-central-bank-digital-currency-20210224.htm#fig1

For some time, the Bank of International Settlement (BIS) has been trying to find clarity and provide some early taxonomy.5

Central bankers are eager to stress the difference between CBDCs and crypto currencies that they prefer to call “crypto assets”. We believe there is an emerging “official” view which broadly sees digital currencies relying on a central authority and being associated with a physical currency, such as the US dollar or the euro. On the contrary, crypto currencies are considered closer to investment than to money and are “mined” or “produced” in a decentralised way by private players.

Reality is more complex. The development of private currencies is possible - bitcoin could soon be accepted as a means of payment by certain businesses. The dystopian risk of fragmentation, multiplication and competition of currencies could soon become real, as is the possibility of the creation of privately sponsored international digital currency areas across national borders.

Facing this threat, but also with the ability to use new tools to fulfil their mandates, central banks are more actively exploring whether and how to create digital currencies. A recent Report on a Digital Euro by the ECB makes a compelling case for its pursuance.6

The challenge for central banks will be to combine the fast-evolving world of digital technologies with the mandate of stability entrusted to them and descending from their mandates. Much preparatory work is necessary and there are numerous issues to be solved, e.g., access, privacy, safety, anti-money laundering, possible restrictions in use, remuneration etc.

The digitalization of the currency opens a realm of possibilities and its introduction could have wide ramifications. Monetary policy could be transformed. Looking into CBDC remuneration, effects could be manifold. For example: i) the transmission of interest rates to household deposit rates could become more direct; ii) the case for negative interest rates, what economists call the “zero low bound problem” could disappear; iii) remuneration could be tiered, with different interest rates applied in different cases. On the latter point, which could open fascinating policy avenues, the ECB writes that CBDC would “allow the Eurosystem to pay less attractive interest rates on large holdings of digital euro or on holdings by foreign investors in order to discourage excessive use of the digital euro as an investment or to mitigate the risk of attracting huge international investment flows”.7

Obviously, the banking system will also be deeply affected, with the possibility of a drastic disintermediation of commercial banks.

At the current stage, no final decision of issuing CBDC has been taken by any major central bank. In this changing and uncertain environment, central banks - and governments - need to act and react fast if they want to retain monetary sovereignty.

Perhaps CBDCs are becoming an inevitable necessity, on top of being useful tools.

Climate

Climate change is a major threat to mankind. Its impact on economic activities cannot be underestimated.

Fighting climate change appears far beyond the remit of central banks. However, climate change has an impact on the economy, including on financial and even price stability.8 There is therefore growing consensus that central banks, without being the main actors, must play a role. This role, which is advocated by many as part of the mobilization of the whole of society against climate change, could cut across monetary policy, financial stability, prudential regulation and supervision.

Central banks are devoting resources to study climate change and its implications for monetary policy. The Swedish Riksbank, the Bank of England, the ECB and more recently the Fed have set up specific processes or working groups to study the matter.9

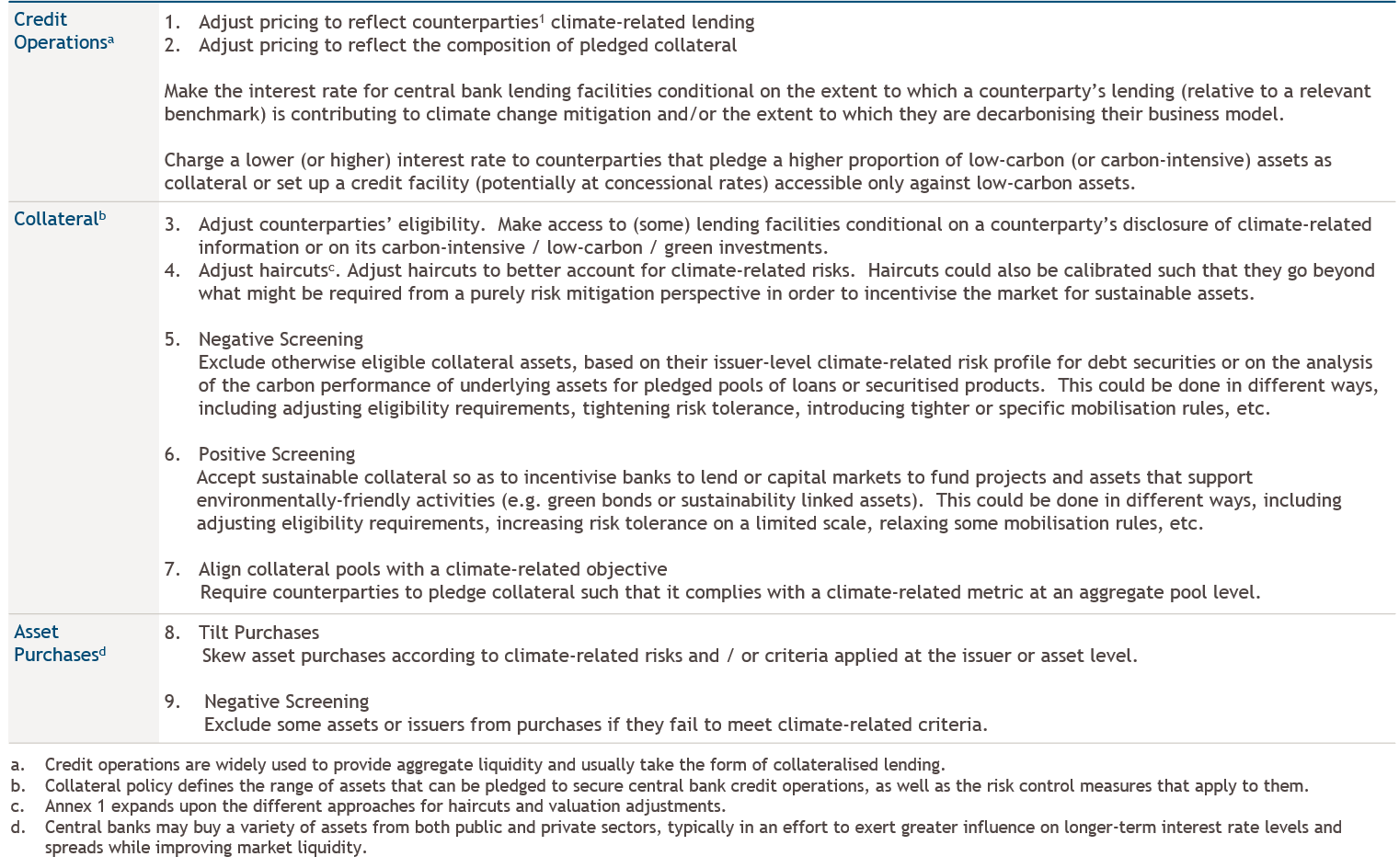

In 2017 the Network for Greening the Financial System (NGFS) was created, which gathers over 80 monetary authorities and financial regulators across the world. The Fed joined in December 2020. The NGFS helps “strengthening the global response required to meet the goals of the Paris agreement and to enhance the role of the financial system to manage risks and to mobilize capital for green and low-carbon investments in the broader context of environmentally sustainable development.”10 A recent NGFS document provides a range of options for central banks’ action around three axis: credit operations, collateral and asset purchase. They are summed up in the following table:11

Selected stylised options for adjusting operational frameworks to climate-related risks

In 2019, the ECB launched a strategy review and put climate change in the list of topics to be addressed. The review has not yet been concluded, but the ECB is already taking some actions on its banking supervision functions, to contain climate-related risk, on the monetary side and on its non-monetary policy portfolio, to facilitate the fight against climate change. In particular, since early 2021, bonds with coupons linked to sustainability performance targets have become eligible as central bank collateral for Eurosystem credit operations and for asset purchase programmes.12 A similar mechanism has also been introduced by the People’s Bank of China.13 A harder stance has been taken by the Swedish Riksbank which, since January 2021, has the option of applying negative screening to its purchases of corporate bonds and excluding bonds from issuers that do not comply with sustainability standards.14

Some key members of the Eurosystem are also backing such initiatives, such as the President of the Bundesbank who recently declared: “In my view, we should consider only purchasing bonds or accepting them as collateral for monetary policy purposes if their issuers meet certain climate-related reporting requirements. In addition, we could examine whether we should use only those ratings that appropriately include climate-related financial risks.”15

Also, in this case, central banks must find new paths which, without compromising their market neutrality or going ultra vires, allow them to take material action against climate change.

Conclusions

As we have highlighted, there are powerful tensions around the traditional mandates of central banks. These tensions run through the unconventional monetary policy instruments in place since the Great Financial Crisis, the fast-paced technology developments that are changing the nature of money and the role society is expecting central banks to play in fighting climate change.

They are somehow testament to the ever-more relevant role that central banking is assuming in our economies. Central bank perspectives are de facto broadening beyond financial markets and banking and societies seem more and more comfortable with this new role. The ultimate challenge will be to reconcile these new functions while retaining full credibility by acting within mandates.

Ultimately, the challenges faced by central banks mirror those of our society.

1.Ben S. Bernanke, Monetary Policy in a new Era, Brookings Institutions, paper prepared for conference on Rethinking Macroeconomic Policy, Peterson Institute, Washington DC, October 12-13, 2017

2.ECB Press Release, Consolidated financial statement of the Eurosystem as at 16 April 2021, https://www.ecb.europa.eu/press/pr/wfs/2021/html/ecb.fs210420.en.html

3.Federal Reserve, Credit and Liquidity Programs and the Balance Sheet,

https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm, as at 20 April 2021

4.A 2021 BIS survey of central banks found that 86% are actively researching the potential for CBDCs, 60% were experimenting with the technology and 14% were deploying pilot projects, https://www.bis.org/about/bisih/topics/cbdc.htm?m=1%7C441%7C714%7C98, as at 29 April 2021

5.For example, Morten Linnemann Bech, Rodney Garratt, Central bank cryptocurrencies, BIS Quarterly Review, September 2017. https://www.bis.org/publ/qtrpdf/r_qt1709.pdf

6.https://www.ecb.europa.eu/pub/pdf/other/Report_on_a_digital_euro~4d7268b458.en.pdf, October 2020. See also Introductory remarks by Fabio Panetta, Member of the Executive Board of the ECB, at the ECON Committee of the European Parliament, 14 April 2021, https://www.ecb.europa.eu/press/key/date/2021/html/ecb.sp210414_1~e76b855b5c.en.html

7.https://www.ecb.europa.eu/pub/pdf/other/Report_on_a_digital_euro~4d7268b458.en.pdf, October 2020

8.FSB, The Implications of Climate Change for Financial Stability, https://www.fsb.orghttps://static.muzinich.com/docs/P231120.pdf 23 November 2020; and Celso Brunetti, Benjamin Dennis, Dylan Gates, Diana Hancock, David Ignell, Elizabeth K. Kiser, Gurubala Kotta, Anna Kovner, Richard J. Rosen, Nicholas K. Tabor, Climate Change and Financial Stability, Feds Notes, 19 March 2021

9.Riksbank Executive Board, Sustainability strategy for the Riksbank, 16 December 2020 https://www.riksbank.se/globalassets/media/riksbanken/hallbarhetsstrategi/engelska/sustainability-strategy-for-the-riksbank.pdf; https://www.bankofengland.co.uk/climate-change; Lael Brainard, Financial Stability Implications of Climate Change, 23 March 2021 https://www.federalreserve.gov/newsevents/speech/brainard20210323a.htm

10.https://www.ngfs.net/en/about-us/governance/origin-and-purpose, 13 September 2019

11.NGFS, Adapting central bank operations to a hotter world. Reviewing some options, March 2021 https://www.ngfs.net/sites/default/files/medias/documents/ngfs_monetary_policy_operations_final.pdf

12.ECB, ECB to accept sustainability-linked bonds as collateral, https://www.ecb.europa.eu/press/pr/date/2020/html/ecb.pr200922~482e4a5a90.en.html

13.NGFS, Adapting central bank operations to a hotter world. Reviewing some options, March 2021, p. 40 https://www.ngfs.net/sites/default/files/medias/documents/ngfs_monetary_policy_operations_final.pdf

14.NGFS, Adapting central bank operations to a hotter world. Reviewing some options, March 2021, p. 45 https://www.ngfs.net/sites/default/files/medias/documents/ngfs_monetary_policy_operations_final.pdf

15.Jens Weidmann, What role should central banks play in combating climate change?, 25 January 2021, https://www.bis.org/review/r210128a.htm

————————————————————————————————————————————-

Important Information

Muzinich & Co. referenced herein is defined as Muzinich & Co., Inc. and its affiliates. This document has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past results do not guarantee future performance. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. This document and the views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity; they are for information purposes only. Opinions and statements of financial market trends that are based on market conditions constitute our judgement as at the date of this document. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Certain information contained in this document constitutes forward-looking statements; due to various risks and uncertainties, actual events may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained in this document may be relied upon as a guarantee, promise, assurance or a representation as to the future. All information contained herein is believed to be accurate as of the date(s) indicated, is not complete, and is subject to change at any time. Certain information contained herein is based on data obtained from third parties and, although believed to be reliable, has not been independently verified by anyone at or affiliated with Muzinich and Co., its accuracy or completeness cannot be guaranteed. Risk management includes an effort to monitor and manage risk but does not imply low or no risk. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability; heightened pricing volatility and reduced market liquidity. In Europe, this material is issued by Muzinich & Co. Limited., which is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ. Muzinich & Co. Limited. is a subsidiary of Muzinich & Co., Inc. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission. Muzinich & Co., Inc.’s being a registered investment adviser with the Securities Exchange Commission (SEC) in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.