Muzinich Weekly Market Comment: Happy Birthday!

Insight

July 6, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

The first half of the year closed with a powerful reminder of America's enduring influence on global markets. From the dominance of the US dollar to AI-driven economic resilience and diverging central bank paths, US exceptionalism continues to shape the investment landscape.

Happy Birthday! In the very week the US marked the 250th anniversary of the Declaration of Independence, it seems fitting that the US dollar closed out June as the dominant currency, appreciating across the board against both the G10 and emerging-market currencies. The sole exception was the Colombian peso, which outperformed the dollar after right-wing outsider Abelardo de la Espriella – known as "El Tigre" and viewed as the preferred candidate of the Trump administration – pulled off a surprise victory in the presidential runoff, defying most pre-election polls.

For much of the past century – and arguably for much of the past 250 years – the US has played the dominant role in global politics, trade and security, acting at various times as the world's policeman, lender of last resort, and financial anchor. Its success is second to none and can largely be attributed to several enduring factors.

First, its political system and institutional independence have proved remarkably resilient. Few countries can claim that their constitutional framework remains fundamentally recognizable after more than two centuries. This stability, combined with the early establishment of strong property rights and the rule of law, created a fertile environment for sustained economic growth. This week, that institutional resilience was reinforced when the US Supreme Court voted 5-4 to allow Federal Reserve (Fed) Governor Lisa Cook to remain in office while she challenges President Trump's attempt to remove her over allegations of mortgage fraud, ruling that a Fed Governor cannot be dismissed without sufficient legal cause.1

The US has also benefited enormously from its geography and natural resources including vast areas of fertile agricultural land, extensive navigable river systems, abundant energy resources and both access to and insulation by the Atlantic and Pacific Oceans. This is all combined with a huge domestic market now numbering over 349 million people,2 with a common language and no internal barriers to trade. The US has enjoyed advantages of both scale and efficiency that few economies can match.

Another key pillar has been the US dollar's status as the world's reserve currency since the end of the Second World War. Despite periodic predictions of its decline, there remain no credible alternatives. The depth and liquidity of US capital markets are unmatched; dollar invoicing remains deeply embedded in global trade, and the country's legal and institutional framework continues to underpin international investor confidence.

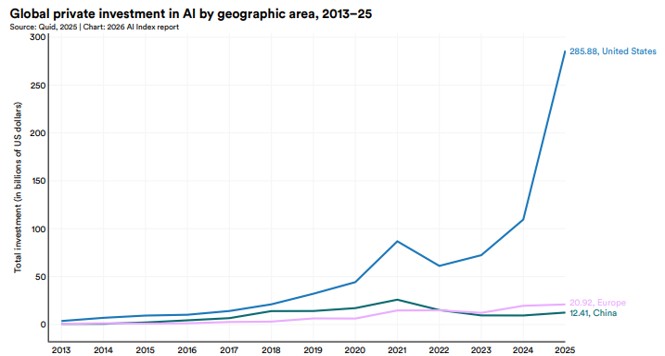

Finally, and perhaps the most important advantage the US has enjoyed over the past 250 years, is its entrepreneurial spirit. This is where America continues to distinguish itself from both its peers and would-be rivals. Its higher education and research ecosystem remains second to none, with seven of the world's top ten universities in the 2026 Times Higher Education World University Rankings located in the United States.3 Perhaps even more importantly, the US has consistently demonstrated an ability to innovate, adapt, and reinvent itself as the global economy evolves. Nowhere is this more evident than in its leadership in artificial intelligence (AI). In 2025, private AI investment in the US reached an estimated US$285 billion – more than twenty-three times the level of its nearest rivals – though this figure, based solely on private investment, likely understates China’s total AI spending). See Charts of the Week.4

As for June, US influence once again dominated financial markets. The defining event was the signing of a Memorandum of Understanding at the Palace of Versailles, which signalled a potential path towards de-escalation in the Middle East and the reopening of the Strait of Hormuz. The agreement triggered a sharp reversal in energy markets, with Brent crude recording its largest quarterly decline since the pandemic. Indeed, the move almost completely unwound the earlier spike that followed the launch of the US military operation against Iran, leaving oil prices broadly back where they had been before the conflict began. More broadly, commodities were the one asset class to avoid in June. The Bloomberg Commodity Index fell more than 14% from its May peak.5

The other notable development in June was the divergence between the US and European government bond markets. The US Treasury curve bear flattened as the newly appointed Fed Chair emphasized that anchoring inflation remains paramount, while the economy streams forward at full throttle.

Economic data released throughout June consistently surprised to the upside, pushing the Citi Economic Surprise Index to historically elevated cyclical levels.6 Growth continues to be supported by a powerful wave of AI driven capital expenditure, resilient consumer spending and a labour market that remains close to full employment. Although last week's non-farm payrolls report came in slightly below market expectations, the report still pointed to a healthy labour market, with unemployment at just 4.2% and the three-month average increase in non-farm payrolls – a measure closely monitored by the Fed – remaining solid at 111,000 jobs.7 Tax rebates have provided an additional tailwind to household spending, reinforcing the resilience of domestic demand.

While the decline in energy prices is clearly a positive development for inflation, particularly across Europe, the inflation story in the United States is far broader. Inflation is no longer being driven by a single factor, but by a combination of resilient consumer demand, firms passing through higher input costs due to tariff related pressures, supply chain constraints and shortages of AI related hardware. Recent price increases across Apple's hardware products provide a timely example of these broader inflationary forces. The company has announced substantial price increases across several product lines, including a 30% increase for the HomePod mini, a 25% increase for Mac Studio models and a 55% increase for Apple TV. These increases reflect the rising cost of semiconductors and illustrate how the investment boom in AI is beginning to feed through to consumer prices.8

In contrast, European government bond curves bull flattened during June, with UK Gilts outperforming the broader region. The combination of lower oil prices, a downside surprise in the UK’s May inflation report and this week's June euro area Harmonised Index of Consumer Prices (HICP) inflation data provided welcome evidence that inflationary pressures may have peaked. In the euro area, headline HICP inflation slowed to 2.8% year-over-year in June from 3.2% in May, while core inflation eased to 2.4% from 2.6%, below the market consensus of 2.5%. Services inflation also moderated, falling to 3.2% from 3.5%, with much of the decline likely driven by the restaurant and hotel category.9

Against this backdrop, the European Central Bank (ECB) may have greater scope to shift its focus towards supporting economic growth than its US counterpart. Unlike the United States, where economic activity continues to surprise to the upside, euro area data have generally remained weak and below economists' expectations. However, the start of July has shown tentative signs of stabilization. The final S&P Global Composite Purchasing Managers' Index was revised up to 50.0 from the preliminary estimate of 49.5, indicating that the euro area economy stagnated, rather than contracted, in June. The improvement was driven primarily by stronger than expected activity in Germany.10 Encouragingly, the easing in the services sector downturn, alongside continued expansion in manufacturing, suggests the broader economy has begun to stabilize after two months of declining output.

At the start of 2026, the debate among investors was not centred on the direction of monetary policy, but rather on how much policy loosening would ultimately be required. As we enter the second half of the year, the focus has shifted to the risk of policy mistakes, and which central bank is most vulnerable to making one. Will the ECB tighten policy too aggressively, or does the greater risk lie with the Fed falling further behind the curve by responding too slowly to persistent inflationary pressures?

As it stands, overnight interest rate markets are pricing an approximately 80% probability that the ECB will raise its policy rate by 25 basis points (bps) during the second half of the year, and a 70% probability of a similar move from the Bank of England's Monetary Policy Committee. Meanwhile markets expect the Federal Open Market Committee to deliver only one 25bps rate increase, currently priced for December.11

Chart of the week: US - Entrepreneurial Spirit and Inflationary?

Source: Stanford University Human-Centered Artificial Intelligence (HAI), AI Index Report 2026. Muzinich views and opinions are subject to change. For illustrative purposes only, not to be construed as investment advice or an invitation to engage in any investment activity.

All sources are Bloomberg unless otherwise stated.

Past performance is not a reliable indicator of current or future results.

References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

References

1. Bloomberg, “Can Trump Fire Lisa Cook After Her Supreme Court Win?” July 2, 2026

2. Worldometer United States Population (LIVE) as of July 2, 2026

3. Times Higher Education, “World University Rankings 2026,” October 9, 2025

4. Stanford University Human-Centered Artificial Intelligence (HAI), AI Index Report 2026

5. Bloomberg, as of July 3, 2026

6. Bloomberg, as of July 3, 2026

7. Bloomberg, “US REACT: Softer June Job Gains to Keep Fed on Hold in July,”

8. Benzinga, "Apple's Aggressive Price Hikes Raise Eyebrows As Wall Street Links AI Chip Shortages To Inflation Pressure Ryan Detrick Says 'This Is the Real World Stuff,'" July 2, 2026

9. Bloomberg, “EURO-AREA REACT: Inflation Drop Weakens Hawks, Hikes Ending,” July 1, 2026

10. Bloomberg, “Euro-Zone Business Activity Revised Up to Stagnation for June,” July 3, 2026

11. Bloomberg as of July 3, 2026

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of June 19, 2026, and may change without notice. All data figures are from Bloomberg, as of July 3, 2026, unless otherwise stated.

--------

Important information

Muzinich & Co., “Muzinich” and/or the “Firm” referenced herein is defined as Muzinich & Co. Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Any forward-looking information or statements expressed in the above may prove to be incorrect. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Muzinich gives no undertaking that it shall update any of the information, data and opinions contained in the above.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

United Arab Emirates (UAE): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the UAE. It is intended solely for Professional Investors and should not be relied upon by any other person. This material has not been reviewed or approved by the UAE Securities and Commodities Authority, the UAE Central Bank or any other relevant authority. Nothing contained herein constitutes investment, legal, tax or other professional advice. Recipients should make their own independent assessment where appropriate.

Abu Dhabi Global Market (ADGM): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the ADGM. It is intended solely for Professional Clients (as defined by the Financial Services Regulatory Authority) and should not be relied upon by any other person. This material has not been reviewed or approved by the Financial Services Regulatory Authority or any other relevant authority in the UAE.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-07-06-18898

By clicking "Submit", I am (i) signing up to receive the Opinion Pieces from the "Opinions" page of the Muzinich & Co website, (ii) representing that the above information is true and accurate and (iii) agreeing to join the Muzinich & Co mailing list. I understand that Muzinich & Co will not add retail investors or individuals with personal email addresses to its mailing list and represent that I am not a retail investor. By providing my personal and professional information I am consenting to its use and disclosure in accordance with the Muzinich & Co. Privacy Policy. I understand that I may withdraw my consent and unsubscribe from receiving future communications by clicking "Unsubscribe" from the emails that are sent to me from Muzinich & Co.