Muzinich Weekly Market Comment: April

Insight

April 13, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

A fragile easing in geopolitical tensions has sparked a broad-based rebound across global markets, with risk assets rallying in line with strong seasonal tailwinds. However, rising inflation pressures and a more cautious central bank outlook suggest investors should remain selective - favouring credit over government bonds as the macro picture evolves. For investors, the fixed income allocation for April looks clear in our view: reduce exposure to government bonds and either rotate into or outright buy short-duration high yield and short-duration EM credit.

April has started on positive footing. The VIX, our preferred measure of risk sentiment, has fallen below 20, suggesting that market uncertainty is easing. Equity markets have rallied broadly, with global indices significantly higher; the Bloomberg World Large & Mid Index is up more than 4%. European markets are leading performance among developed economies, while Asia is outperforming within Emerging Markets (EM).

In commodities, Brent crude has dropped below US$100, while gold has resumed its push back up toward the US$5,000 level. The US dollar has weakened against major global currencies, with the notable exception of the Japanese yen, a traditional risk-off haven currency. Latin American currencies have rallied more than 3% against the dollar, the euro has appreciated by over 1% and bitcoin is up more than 4%.

In fixed income, corporate credit markets are also stronger. High-yield bonds are up over 1.5%, while investment-grade credit has gained more than 0.5%. The US Treasury curve remains broadly stable, whereas the European yield curve has flattened, driven by declining front-end yields.

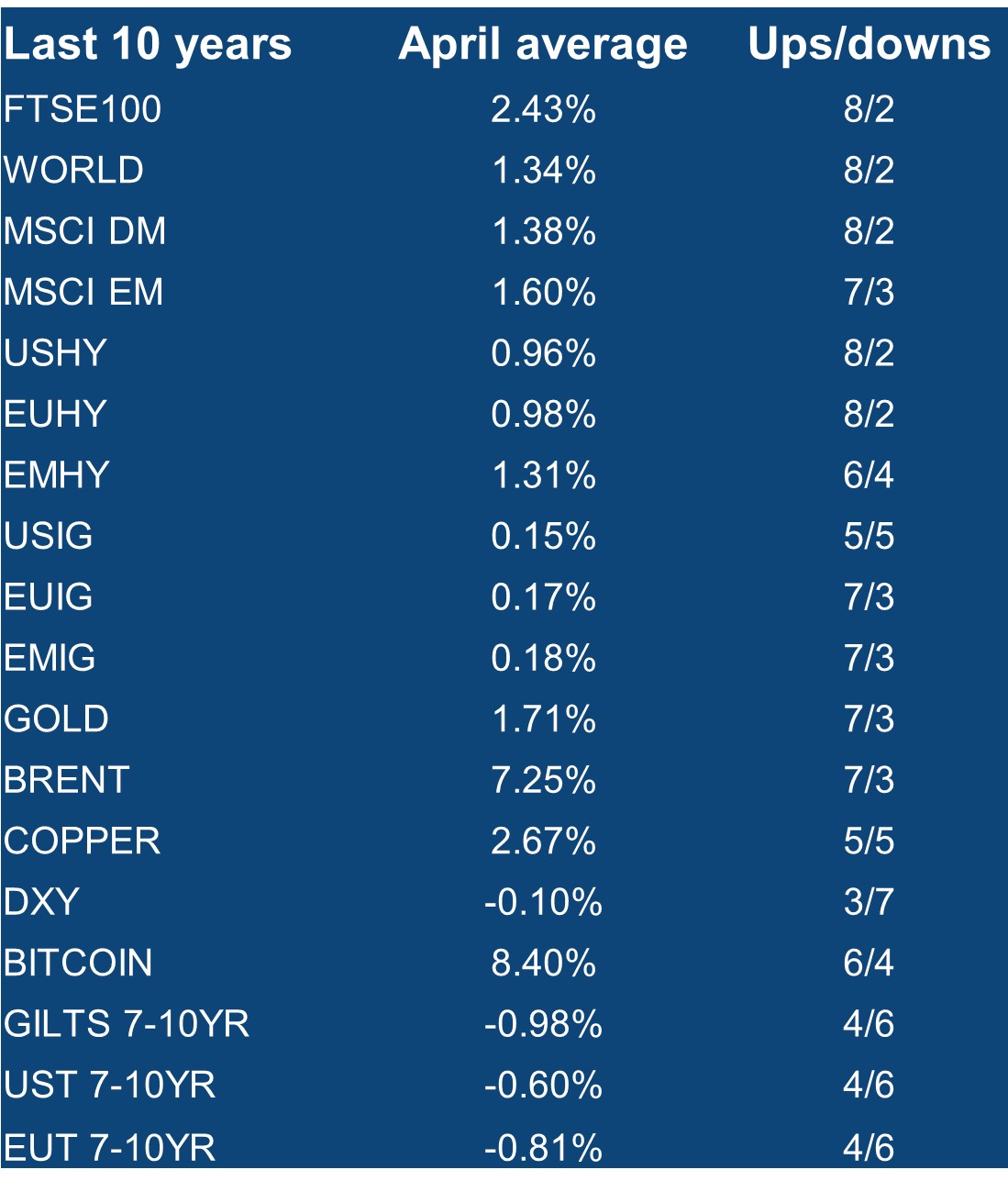

Had one spent March on the dark side of the moon, April's price action would have come as little surprise. The month is historically one of the most favourable in the calendar for investors, and the reasons are structural. April marks the opening of Q1 earnings season, with companies across the US and Europe reporting results that, more often than not, beat tempered consensus estimates. In Japan and parts of Europe, it also coincides with the start of the new fiscal year, bringing fresh institutional mandates and capital deployment. Meanwhile, US investors typically receive tax refunds that find their way back into markets, providing a modest but consistent tailwind. Perhaps most importantly, with the first quarter in the rearview mirror, investors tend to have materially better visibility on the trajectory of central bank policy and global economic conditions, that is, improved macro visibility. From a ten-year perspective, April bears all the hallmarks of a risk-on month across global asset classes (see Chart of the Week below).

In equities, the pattern is consistent and broad-based. Global equity markets have posted positive returns in eight of the last ten Aprils, with EM equities modestly outperforming their developed market peers. The FTSE 100 stands out; April is its single best-performing month of the year on a ten-year average.

Credit markets tell a similar story. High yield outperforms investment-grade, with EM high yield delivering its strongest month of the year on average over the past decade. For investment-grade investors, April often presents a “buy the dip” opportunity, as the second quarter has historically been the strongest period of the year on a ten-year average for both US and EM credit.

In our view, the main area for caution is government bonds. Gilts and European sovereign debt have delivered negative returns in six of the past ten Aprils, and the second quarter has been the weakest period of the year on a ten-year average for both, reflecting the broader rotation into risk assets that typically characterizes this period. Rounding out the picture, the US dollar has tended to soften modestly through April, providing a tailwind for commodity prices, most of which have historically risen over the month.

Returning to April 2026, the primary catalyst behind the reversal in sentiment and the recovery in asset prices has been a fragile but consequential ceasefire between the US and Iran. Iranian Foreign Minister Abbas Araghchi confirmed that safe passage through the Strait of Hormuz would be permitted for a two-week window via coordination, with Iran's Ports and Maritime Organization publishing two safe routes for shipping,1 but as of now, the strait remains virtually closed. President Donald Trump has vowed to keep troops in the Persian Gulf ahead of talks in Pakistan this weekend, where Vice President Vance is set to lead the American delegation. Vance struck a measured tone: "If the Iranians are willing to negotiate in good faith, we're certainly willing to extend the open hand. If they're going to try to play us, then they're going to find the negotiating team is not that receptive".2

A further positive announcement came from Israel, where Israeli Prime Minister Benjamin Netanyahu said he agreed to hold direct talks with Lebanon about the conflict with a focus on disarming Hezbollah. Trump called the Israeli leader and asked him to scale back strikes to ensure the success of negotiations with Iran.3

For investors searching for evidence of the conflict's economic footprint, this week's inflation data provided uncomfortable confirmation. In Asia, China's Producer Price Index (PPI) snapped a remarkable 41-month run of deflation, rising 0.5% year-over-year (yoy) in March after a 0.9% decline in February, a signal that upstream cost pressures are beginning to feed through the supply chain in earnest.4

In Europe, the picture was similarly sobering. German headline inflation accelerated sharply to 2.8%yoy, well above February's 2.0%, with energy costs surging 7.2%, their first annual increase since December 2023.5 Spain told a comparable story, with inflation jumping to 3.3%, its highest reading since June 2024, up from 2.5% in February, but short of the 3.8% economists had anticipated.6

In the US, the conflict's fingerprints were most visible at the petrol pump. Headline Consumer Price Index (CPI) rose 0.87% in March – the largest monthly increase in almost four years – driven by a surge in gasoline prices, compared to a relatively benign 0.27% in February. Core inflation, however, remained contained, with services inflation easing and the core rate edging only marginally higher to 2.6% from 2.5% yoy,7 offering the Federal Open Market Committee (FOMC) a degree of comfort that the pass-through into broader price pressures remains limited for now. Meanwhile, the Committee’s minutes from the March 17–18 FOMC meeting struck a hawkish tone, showing a committee inclined to keep rates on hold. The vast majority of members judged that progress toward the 2% inflation objective could be slower than previously expected, and that the risk of inflation running persistently above target had increased.8

For investors, the fixed income allocation for April looks clear in our view: reduce exposure to government bonds and either rotate into or outright buy short-duration high yield and short-duration EM credit.

Chart of the Week: April seasonals*

Source: Bloomberg as of April 10, 2026. *see index descriptions for full information on all indices used in this table. Index performance is for illustrative purposes only. You cannot invest directly in the index.

Source: Bloomberg as of April 10, 2026. *see index descriptions for full information on all indices used in this table. Index performance is for illustrative purposes only. You cannot invest directly in the index.

References

1.Bloomberg, as of 8th April 2026,“US and Iran Agree to Ceasefire Hours Before Trump Deadline,” April 8, 2026

2. Bloomberg, as of 10th April, “Vance warns Iran not to ‘play’ the US as he departs for negotiations aimed at ending their war”

3. Bloomberg, as of 9th April, 2026“US, Iran Prepare for Talks With Lebanon Conflict Unresolved,”

4. Bloomberg, as of 9th April 2026 “CHINA REACT: War Pushed PPI Back to Inflation as CPI Slowed,”

5. Bloomberg, as of 30th March 2026 “German Inflation Surges to Highest in More Than Year on War,”

6. Bloomberg, as of 27th March 2026 “Spanish Prices Rise at Fastest Pace Since 2024 on Iran War,”

7. Bloomberg, as of 10th April 2026, “US REACT: Gas Drives Up Headline CPI in First Impact of Iran War”

8. Bloomberg, as of 8th April 2026. “US REACT: Hawkish FOMC Minutes Reinforce View of Near-Term Hold”

All sources are Bloomberg unless otherwise stated.

Past performance is not a reliable indicator of current or future results.

References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of April 13 2026 and may change without notice.

--------

Index descriptions

FTSE100 - UKX Index: The FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. The equities us an investibility weighting in the index calculation. The index was developed with a base level of 1000 as of December 30, 1983.

MSCI DM - MXWO Index: The MSCI World Index is a free-float weighted equity index. It was developed with a base value of 100 as of December 31, 1969. MXWO indexed developed world markets and does not include emerging markets. MXWD includes both emerging and developed markets.

MSCI EM - MXEF Index: The MSCI EM Index is a free-float weighted equity index that captures large and mid cap representation across emerging market countries. The index covers approximately 85% of the free float-adjusted market capitalisation in each country

USHY - J0A0: The ICE BofA US Cash Pay High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt, currently in a coupon paying period that is publicly issued in the US domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million.

EUHY - HE00: The ICE BofA Euro High Yield Index tracks the performance of EUR dominated below investment grade corporate debt publicly issued in the euro domestic or eurobond markets. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity, a fixed coupon schedule and a minimum amount outstanding of EUR 250 million.

EMHY – EMHY: The ICE BofA High Yield US Emerging Markets Liquid Corporate Plus Index is a subset of The ICE BofA US Emerging Markets Liquid Corporate Plus Index including all securities rated BB1 or lower. The ICE BofA US Emerging Markets Liquid Corporate Plus Index tracks the performance of U.S. dollar denominated emerging markets non-sovereign debt publicly issued in the major domestic and eurobond markets.

USIG - C0A0: The ICE BofA US Corporate Index tracks the performance of US dollar denominated investment grade corporate debt publicly issued in the US domestic market. Qualifying securities must have an investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of US$250 million.

EUIG - ER00: The ICE BofA Euro Corporate Index tracks the performance of EUR denominated investment grade corporate debt publicly issued in the eurobond or Euro member domestic markets. Qualifying securities must have an investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity, a fixed coupon schedule and a minimum amount outstanding of EUR 250 million.

EMIG – EMIB: The ICE BofA High Grade Emerging Markets Corporate Plus index is a subset of the ICE BofA Emerging Markets Corporate Plus Index (EMCB) including all securities rated AAA through BBB3, inclusive.

GILTS 7-10YR - G4L0: The ICE BofA 7-10 Year UK Gilt Index is a subset of the ICE BofA UK Gilt Index (G0L0) including all securities with a remaining term to final maturity greater than or equal to 7 years and less than 10 years.

WORLD Index – Bloomberg World Large & Mid Cap Price return index is a float market-cap-weighted equity benchmark that covers the top 86% of market cap of the measured market.

GOLD - XAU Curncy – XAUUSD Spot Exchange Rate – price of 1XAU in USD Gold. The gold spot price is quoted as US Dollars per Troy Ounce. Gold Cross rates are available using XAU followed by 3-character ISO code of the cross currency.

BRENT - CO1 Comdty – current pipeline export quality Brent blend as supplied at Sullom Voe. ICE Brent futures is a deliverable contract based on EFP delivery with an option to cash settle. Date of launch: 23rd June 1988.

DXY- DXY Curncy - The US Dollar index (USDX) indicates the general int’l value of the USD. The USDX does this by averaging the exchange rates between the USD and major world currencies. The ICE US computes this by using the rates supplied by some 500 banks.

BITCOIN – Bloomberg Bitcoin index: Bloomberg Bitcoin Index is designed to measure the performance of the digital asset Bitcoin traded in USD. Please note, use as a financial benchmark may be restricted.

UST 7-10YR - ICE U.S. Treasury 7-10 Year Bond Index (IDCOT7)

ICE U.S. Treasury 7-10 Year Bond Index tracks the performance of US dollar denominated sovereign debt publicly issued by the US government in its domestic market. Qualifying securities must have greater than seven years and less than or equal to ten years remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and an adjusted amount outstanding of at least $300 million. The amount outstanding for all qualifying securities is adjusted to reduce by the amounts held by the Federal Reserve’s SOMA account. Bills, inflation-linked debt, original issue zero coupon securities and STRIPs are excluded from the Index; however, the amounts outstanding of qualifying coupon securities are not reduced by any portions that have been stripped. Agency debt with or without a US Government guarantee and securities issued or marketed primarily to retail investors do not qualify for inclusion in the index.

--------

Important Information

Muzinich & Co., “Muzinich” and/or the “Firm” referenced herein is defined as Muzinich & Co. Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Any forward-looking information or statements expressed in the above may prove to be incorrect. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Muzinich gives no undertaking that it shall update any of the information, data and opinions contained in the above.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

In the United Arab Emirates (UAE) (excluding the Dubai International Financial Centre (DIFC) and the Abu Dhabi Global Market (ADGM): This document, and the information contained herein, does not constitute, and is not intended to constitute, a public offer of securities in the United Arab Emirates (“UAE”) and accordingly should not be construed as such. The Units are only being offered to a limited number of exempt Professional Investors in the UAE who fall under one of the following categories: federal or local governments, government institutions and agencies, or companies wholly owned by any of them. The Units have not been approved by or licensed or registered with the UAE Central Bank, the SCA, the Dubai Financial Services Authority, the Financial Services Regulatory Authority or any other relevant licensing authorities or governmental agencies in the UAE (the “Authorities”). The Authorities assume no liability for any investment that the named addressee makes as a Professional Investor. The document is for the use of the named addressee only and should not be given or shown to any other person (other than employees, agents or consultants in connection with the addressee’s consideration thereof).

In the United Arab Emirates (UAE) (including the Dubai International Financial Centre and the Abu Dhabi Global Market): This information does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe for or purchase, any securities or investment products in the UAE and accordingly should not be construed as such. Furthermore, this information is being made available on the basis that the recipient is an entity fully regulated by the ADGM Financial Services Regulatory Authority (FSRA), and acknowledges and understands that the entities and securities to which it may relate have not been approved, licensed by or registered with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority, the Financial Services Regulatory Authority or any other relevant licensing authority or governmental agency in the UAE. The content of this report has not been approved by or filed with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority or the Financial Services Regulatory Authority.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom.