Muzinich Weekly Market Comment: Micro is Back

Insight

June 22, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

It was an excellent week for micro, bottom-up investors, as the macro clouds that have overshadowed and frustrated our day-to-day work finally began to clear.

US and Iranian leaders signed a Memorandum of Understanding (MOU) at the Palace of Versailles, signalling a potential path toward ending the conflict. It is important to note that an MOU is not a final agreement; rather, it is a non-binding document that outlines the parties' mutual intention to work toward a formal deal. As such, there remains significant scope for negotiations to falter before a definitive agreement is reached.

Nevertheless, the MOU delivers several meaningful near-term positive outcomes. Most importantly, the Strait of Hormuz will reopen, providing much-needed relief to global energy markets. Equally significant is Point 3 of the agreement, which states that if a final deal has not been reached within 60 days, the MOU is “extended by mutual consent”. In effect, this removes the risk of negotiations collapsing against a hard deadline, regardless of the pace of progress toward a permanent settlement.1

Taken together, these developments give us a reasonable degree of confidence that both the military conflict and the closure of the Strait of Hormuz are, in all likelihood, behind us. As a result, the daily macro-driven volatility that has weighed so heavily on markets throughout this episode should begin to fade, allowing investors to refocus on fundamentals.

The second macro uncertainty to lift came from central banks. Eleven committees met this week, all delivering in line with market expectations. Seven held rates steady, among them the Swiss National Bank, which kept its policy rate at zero - the lowest of any major central bank globally – with communications across the on-hold cohort skewed firmly toward anchoring inflation expectations. Three committees hiked by 25 basis points (bps), all from Asia. Brazil stood apart, continuing its gradual normalization from extraordinarily tight monetary conditions and cutting its policy rate by a further 25bps to 14.25%.

In Asia, the Bank of Japan (BoJ) raised its target rate to 1.0% from 0.75%, the highest level since 1995, in a move that passed without drama – a far cry from the extreme volatility that once accompanied BoJ policy shifts. The board voted 7-1 in favour of the increase and signalled a willingness to continue raising rates, with Deputy Governor Uchida noting that "financial conditions remain accommodative", though overall communication maintained its characteristically cautious tone. On the balance sheet, the BoJ confirmed it will continue its existing tapering path, reducing monthly Japanese government bond purchases by ¥200 billion each quarter until the end of Q1 2027, at which point purchases will stabilize at approximately ¥2 trillion per month, down from the current pace of ¥2.7 trillion. 2

In Indonesia, where macro storm clouds had been gathering, Bank Indonesia continued to stand out for both its independence and its commitment to capital market stability. Those qualities have become increasingly valuable amid concerns over the gradual erosion of institutional credibility under President Prabowo Subianto. Against this backdrop, the Bank Indonesia reinforced its credentials by following an earlier inter-meeting 25bps hike with a further 25bps increase to 5.75%,3 helping to restore confidence and steady investor sentiment.4

From Europe, the UK took center stage, though there was very little surprise from the Monetary Policy Committee, which held rates at 3.75% at its June meeting, as widely expected. The Committee stuck with its standing line that it "stands ready to act as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term." Meanwhile, Governor Andrew Bailey noted that he was "content at the present time with holding." 5

Bailey may well have had one eye on the May CPI print, which delivered a welcome downside surprise. Inflation held steady at 2.8% in May, meaningfully below the 3.3% the Bank had forecast in its April Monetary Policy Report. The Office for National Statistics (ONS) attributed the softer reading to falling food costs, particularly meat and dairy products, which more than offset upward pressure from air fares, vehicle taxes, and petrol. 6 The data suggested price pressures across the economy were somewhat weaker than feared.

The primary source of central bank uncertainty over the last few weeks was the change of the guard at the Federal Reserve (Fed), with Kevin Warsh taking the helm after eight years of Jerome Powell's leadership. Warsh wasted no time in putting his stamp on the Federal Open Market Committee (FOMC). In a decisive break from recent practice, he slashed the post-meeting statement to just 130 words, stripped out forward guidance entirely, and declined to submit his own forecasts to the Summary of Economic Projections, signalling a deliberate return to the more opaque communication style used during the Greenspan era.

The overall message was distinctly hawkish. The statement (1) described activity as expanding at a solid pace despite elevated uncertainty, (2) highlighted continued labour market strength, and (3) reiterated that inflation remains above the Fed's 2% target. Crucially, the Committee dropped the previous dovish-leaning guidance and inserted an unambiguous commitment to "deliver price stability". The dot plot reinforced this posture, with nine of eighteen participants now pencilling in at least one rate hike this year. At the same time, inflation forecasts also moved materially higher, with median headline Personal Consumption Expenditures (PCE) for 2026 revised up to 3.6%, and core PCE now projected to remain above target through at least 2028.

At the press conference, Warsh maintained a firmly hawkish tone throughout, pointedly avoiding arguments he has previously entertained including the potentially disinflationary effects of AI, productivity gains, and more benign signals from alternative measures of trend inflation. He also announced the establishment of five task forces covering communications, the balance sheet, data sources, AI and productivity and the Fed's inflation framework, with most expected to conclude their work by year-end. 7

With the US-Iran conflict entering a less disruptive phase for the global economy, Brent spot has fallen below US$80, a level we consider growth neutral. However, the damage the conflict has inflicted is nonetheless visible in the central bank response, with policymakers across the board now firmly determined to anchor inflation expectations leading to a path of least resistance for further policy tightening should inflation fail to recede and trend back toward targets. Investors think central banks have more work to do, pricing a 95% probability of a further 25bps hike from the BoJ in December, while over the next 12 months the European Central Bank, Bank of England and Fed are priced to deliver 1.7, 1.6 and 1.9 additional hikes of 25bps respectively. 8

Bond curves have begun to bear flatten across most major markets with Japan as the exception – a development that might be read as a vote of confidence in central banks' commitment to anchoring inflation. However, this curve movement carries its own warning. Bear flattening most commonly occurs when the economy is in the mid-to-late stages of the cycle, or when overheating risks are present with inflation running above target.

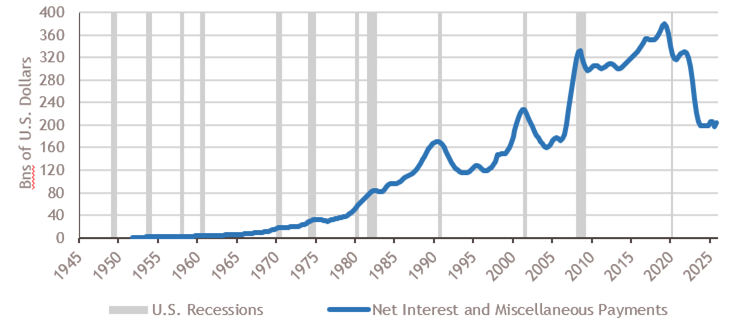

For corporate bond investors, this is precisely the moment for careful and disciplined assessment, where rigorous bottom-up security selection pays its greatest dividend. The standard credit cycle dynamic is well understood; companies lever up as financial conditions ease and the cost of funding remains low, but as interest rates rise, the debt burden grows, margins compress and the pressure to cut costs and reduce headcount intensifies. Left unchecked, this late-cycle deterioration can lead to a slowdown and, in the worst case, recession – with the most vulnerable credits ultimately facing restructuring.

However, there is limited sign of this dynamic taking hold in the US at present. As our Chart of the Week illustrates, net interest and miscellaneous payments by nonfinancial corporates have fallen sharply since their post-Covid peak and currently sit at levels last seen a decade ago. This suggests corporate balance sheets have so far absorbed the higher cost of capital with greater resilience than the late-cycle narrative might imply, a reminder that broad macro warnings do not always translate uniformly into credit stress, and that careful security selection remains the essential tool for navigating what lies ahead.

Chart of the Week: Nonfinancial Corporate Business; Net Interest and Miscellaneous Payments, Transactions

Source: Federal Reserve Bank of St .Louis (FRED), as of June 11, 2026. Muzinich views and opinions are subject to change. For illustrative purposes only, not to be construed as investment advice or an invitation to engage in any investment activity.

Source: Federal Reserve Bank of St .Louis (FRED), as of June 11, 2026. Muzinich views and opinions are subject to change. For illustrative purposes only, not to be construed as investment advice or an invitation to engage in any investment activity.

All sources are Bloomberg unless otherwise stated.

Past performance is not a reliable indicator of current or future results.

References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

References

1. Bloomberg, “Read the 14-Point Draft Memorandum Between the US and Iran,” June 16, 2026

2. Bloomberg, “BoJ REACT: Rate Hike, JGB Taper Halt, Uchida Plays It Cool,” June 16, 2026

3. Bloomberg, “INDONESIA REACT: One More Rate Hike Won’t Restore Confidence,” June 9, 2026

4. Bloomberg, “INDONESIA REACT: Rupiah Remains in Driver’s Seat for Rates,” June 18, 2026

5. Bloomberg, “BOE REACT: Tough Talk For Now, Oil Drop Means No 2026 Hikes,” June 18, 2026

6. Bloomberg, “UK Inflation Unexpectedly Holds Steady Ahead of BOE Decision,” June 17, 2026

7. Deutsche Bank Research, “June FOMC recap: Rock Chalk, Warch-hawk,“ June 17, 2026

8. Bloomberg, as of June 19, 2026

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of June 19, 2026, and may change without notice. All data figures are from Bloomberg, as of June 19, 2026, unless otherwise stated.

--------

Important information

Muzinich & Co., “Muzinich” and/or the “Firm” referenced herein is defined as Muzinich & Co. Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Any forward-looking information or statements expressed in the above may prove to be incorrect. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Muzinich gives no undertaking that it shall update any of the information, data and opinions contained in the above.

United Arab Emirates (UAE): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the UAE. It is intended solely for Professional Investors and should not be relied upon by any other person. This material has not been reviewed or approved by the UAE Securities and Commodities Authority, the UAE Central Bank or any other relevant authority. Nothing contained herein constitutes investment, legal, tax or other professional advice. Recipients should make their own independent assessment where appropriate.

Abu Dhabi Global Market (ADGM): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the ADGM. It is intended solely for Professional Clients (as defined by the Financial Services Regulatory Authority) and should not be relied upon by any other person. This material has not been reviewed or approved by the Financial Services Regulatory Authority or any other relevant authority in the UAE.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-06-22-18799