Defined horizons, compelling income: The appeal of fixed maturity portfolios

Insight

June 9, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

In a world of shifting rate expectations and persistent volatility, fixed maturity portfolios are re-emerging as a compelling way to capture income, improve portfolio resilience and bring greater certainty to fixed income investing as Joseph Galzerano and Richard Smith discuss.

Fixed maturity strategies are for investors seeking greater income visibility and downside discipline in a more uncertain macro environment. With interest rates elevated, geopolitical tensions persisting and central bank paths becoming less predictable, investors are reassessing how fixed income allocations can deliver both stability and attractive returns. Against this backdrop, fixed maturity portfolios offer a differentiated approach by combining attractive yields with a clearly defined investment horizon.

What are fixed maturity portfolios?

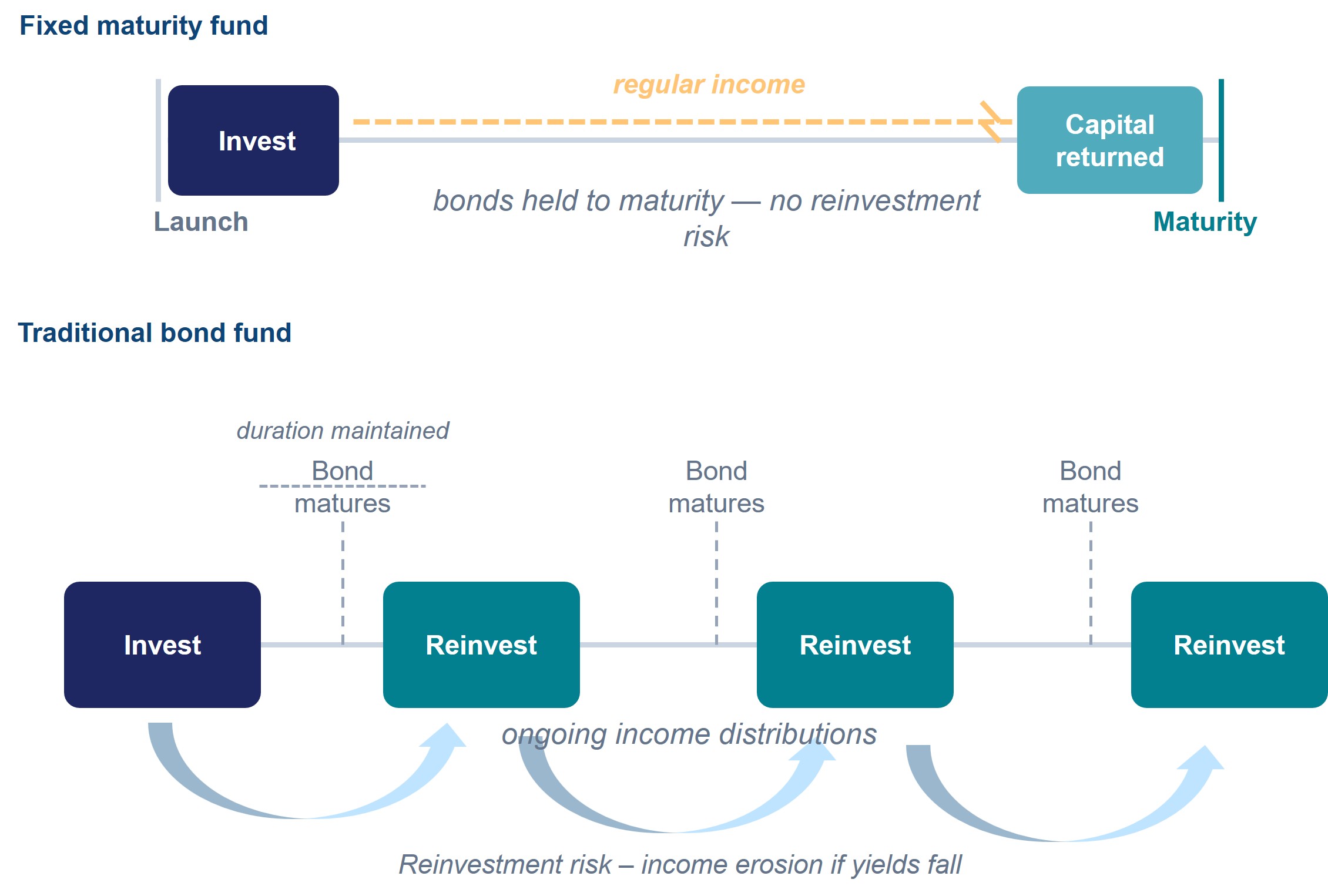

A fixed maturity portfolio is a credit strategy constructed around a predetermined end date. Unlike traditional bond funds, which maintain a constant duration and continuously recycle holdings, fixed maturity portfolios invest primarily in bonds expected to mature close to the strategy’s termination date.

This structure creates greater visibility over the investment journey. Investors know from the outset when the portfolio is expected to mature and can estimate the expected income profile over the life of the strategy, subject to market and credit conditions.

For investors navigating uncertain markets, this defined maturity profile can offer a clearer framework for portfolio planning, liability management and capital allocation.

Why fixed maturity portfolios matter today

We believe the current environment presents a compelling opportunity for fixed maturity strategies. Elevated rate volatility, persistent inflation pressures and ongoing geopolitical uncertainty are increasing demand for investment approaches that provide both compelling income and greater certainty over outcomes. At the same time, credit yields remain materially above levels seen during the ultra-low-rate era and continue to offer attractive premiums over sovereign and traditional investment grade markets.

The opportunity, however, extends beyond carry. If inflation moderates or central banks begin easing policy, lower sovereign yields could support price appreciation across underlying credit holdings. Investors who remain on the sidelines risk redeploying capital later at lower all-in yields should spreads compress or rates decline.

Fixed maturity strategies may also benefit from a supportive backdrop for credit markets. Despite slower growth across developed economies, corporate fundamentals remain broadly resilient and default rates contained. Combined with periods of spread widening driven by uncertainty, this may provide an attractive entry point for investors seeking income within a disciplined portfolio framework.

Key features and benefits

One of the primary attractions of fixed maturity portfolios is outcome visibility. Investors know the intended maturity date at inception, allowing for more precise planning around liabilities, cash flow requirements and investment objectives.

The structure can also help reduce behavioural and reinvestment risk. Traditional bond funds may experience changing duration profiles and require maturing proceeds to be reinvested into prevailing market conditions, which can reduce future income if yields decline. By contrast, fixed maturity portfolios encourage a more disciplined investment approach and allow investors to secure exposure to current yield levels over a defined horizon.

Figure 1 – Fixed maturity vs. traditional bond fund

Source: Muzinich & Co. For illustrative purposes only.

Higher starting yields are another important consideration. Historically, income has represented the majority of long-term fixed income returns, particularly within credit markets, meaning locking in elevated yields can provide a strong foundation for future total returns.

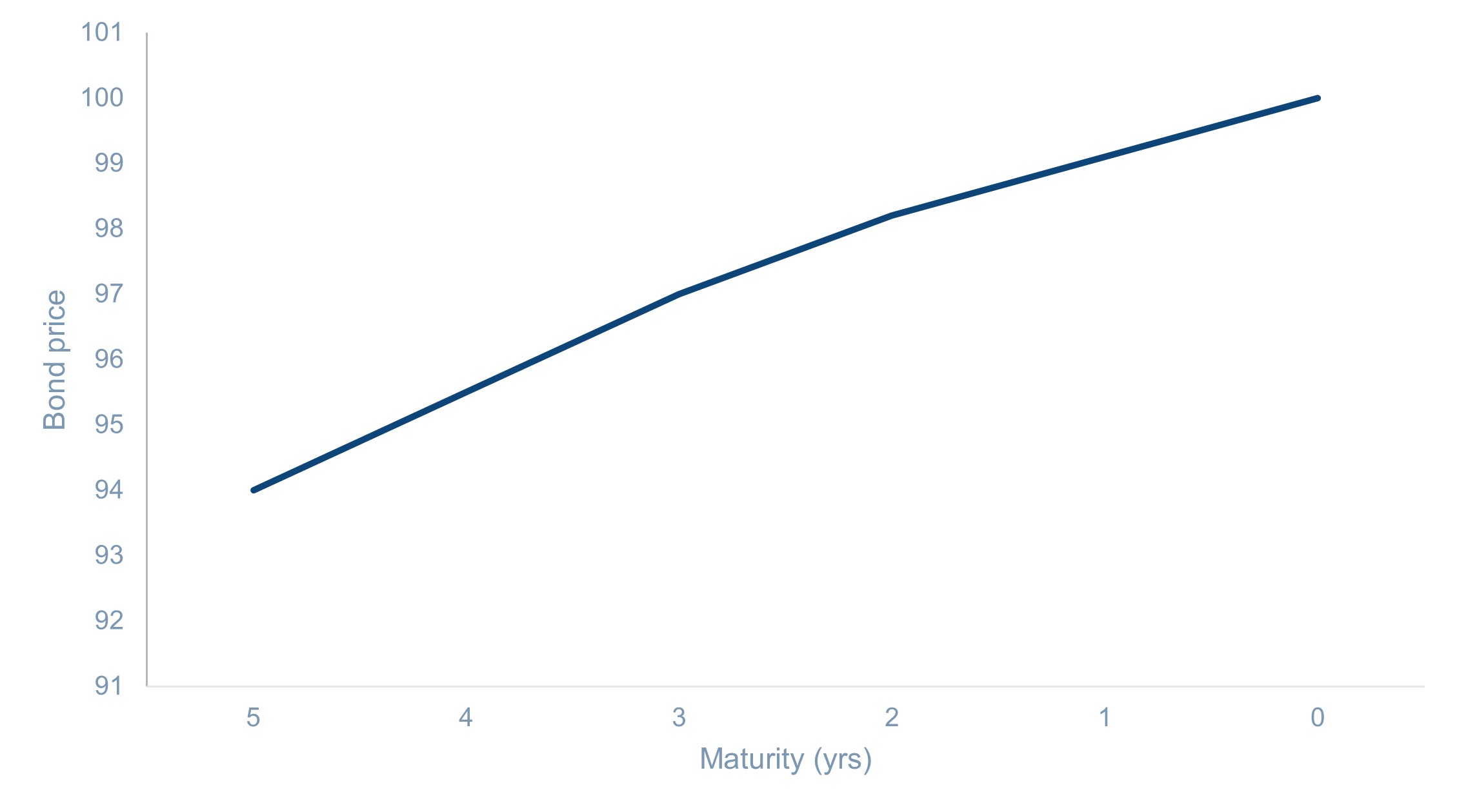

A further structural benefit is the pull-to-par effect. As bonds approach maturity, prices naturally converge toward par value assuming no default, helping to dampen mark-to-market volatility over time while providing an additional source of return alongside coupon income.

Figure 2 Pull to par - an additional source of return

Source: Muzinich & Co. For illustrative purposes only.

Source: Muzinich & Co. For illustrative purposes only.

Modern fixed maturity portfolios also benefit from broad opportunity sets across global credit markets. Flexible mandates can allocate across investment grade, high yield and structured credit, allowing managers to identify relative value opportunities while balancing income generation with downside risk management. For individual investors, this pooled approach offers a significant practical advantage: rather than concentrating exposure in a small number of directly held bonds, a fixed maturity portfolio provides access to a diversified basket of positions across issuers, sectors and geographies. This diversification, combined with the economies of scale available through a fund structure, can meaningfully reduce transaction costs and idiosyncratic credit risk compared to building an equivalent portfolio directly.

Beyond the technical merits, fixed maturity portfolios also address something more fundamental: the need for investors to feel confident that their capital is working toward a specific goal, over a timeframe they understand. The combination of a defined end date, a visible income profile and a disciplined investment process allows investors to align their portfolio with concrete financial objectives – whether that is funding a future liability, supplementing retirement income or preserving capital over a set horizon. This clarity of purpose, and the peace of mind it can provide, is a distinguishing feature of the fixed maturity structure that traditional open-ended bond funds find difficult to replicate.

Risks

While fixed maturity portfolios offer greater visibility and a defined investment horizon, they are not without risk. Investors remain exposed to credit risk, including the possibility of issuer defaults or deteriorating fundamentals, as well as market risk from changes in interest rates and credit spreads that can affect valuations before maturity. Liquidity conditions may also weaken during periods of market stress, particularly in lower-rated or less liquid segments of the market. Although the structure can help reduce reinvestment uncertainty and support investment discipline, outcomes remain dependent on active credit selection, diversification and effective risk management.

A structurally attractive opportunity set

Fixed income markets are entering a structurally different era. After years of suppressed yields and extraordinary monetary policy support, investors can once again access meaningful income across credit markets.

Against this backdrop, fixed maturity portfolios offer a compelling combination of attractive carry, diversification and defined investment horizons. By pairing today’s elevated yields with active management and a disciplined portfolio structure, they may provide a more resilient framework for navigating uncertainty while seeking attractive long-term risk-adjusted returns.

The appeal of this approach is not confined to any single type of investor or geography. Whether the motivation is retirement planning, liability matching or simply the desire for a more predictable fixed income experience, the fixed maturity structure speaks to a common thread: investors across markets increasingly value the ability to plan with confidence. In an environment where the path of rates, growth and geopolitics remains uncertain, a portfolio built around a defined horizon and a transparent income objective offers something that few other structures can – a clear answer to the question of what an investment is expected to deliver, and when.

--------

Important information

Muzinich and/or Muzinich & Co. referenced herein is defined as Muzinich & Co., Inc. and its affiliates. Muzinich views and opinions. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall.

Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only.

This discussion material contains forward-looking statements, which give current expectations of future activities and future performance. Any or all forward-looking statements in this material may turn out to be incorrect. They can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Although the assumptions underlying the forward-looking statements contained herein are believed to be reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurances that the forward-looking statements included in this discussion material will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Further, no person undertakes any obligation to revise such forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

United Arab Emirates (UAE): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the UAE. It is intended solely for Professional Investors and should not be relied upon by any other person. This material has not been reviewed or approved by the UAE Securities and Commodities Authority, the UAE Central Bank or any other relevant authority. Nothing contained herein constitutes investment, legal, tax or other professional advice. Recipients should make their own independent assessment where appropriate.

Abu Dhabi Global Market (ADGM): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the ADGM. It is intended solely for Professional Clients (as defined by the Financial Services Regulatory Authority) and should not be relied upon by any other person. This material has not been reviewed or approved by the Financial Services Regulatory Authority or any other relevant authority in the UAE.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom. 2026-06-01-18594

By clicking "Submit", I am (i) signing up to receive the Opinion Pieces from the "Opinions" page of the Muzinich & Co website, (ii) representing that the above information is true and accurate and (iii) agreeing to join the Muzinich & Co mailing list. I understand that Muzinich & Co will not add retail investors or individuals with personal email addresses to its mailing list and represent that I am not a retail investor. By providing my personal and professional information I am consenting to its use and disclosure in accordance with the Muzinich & Co. Privacy Policy. I understand that I may withdraw my consent and unsubscribe from receiving future communications by clicking "Unsubscribe" from the emails that are sent to me from Muzinich & Co.