Insight | February 28, 2020

Private Debt – An All-Weather Asset Class - February 2020

Where might investors find yield, protection from volatility and investment opportunities across the credit cycle?

The European private debt market is a relatively new asset class, having evolved as private lenders stepped into the gap left by banks after the great financial crisis.

Today, while banks are still lending, they are becoming increasingly limited by ongoing regulation and capital constraints.1

Meanwhile private debt, or direct lending, is being assisted by a relaxation of lending laws, such as in Germany and Italy, which is enabling non-bank lenders to provide financing solutions.

As a result, direct lenders are now firmly established participants in the market.2

Risk/Return Profile

Falling interest rates in 2019, combined with increasing amounts of negative-yielding debt, reinforced investors’ hunt for yield.3 While some may be willing to move down the risk spectrum to find yield, we believe private debt can offer an alternative likely to weather an ageing credit cycle, particularly when managed as a responsible investment strategy.

In our view, private debt can provide investors the potential for higher yields, via an illiquidity premium, than available in public markets.

The asset class also has a low correlation to public market fixed income and therefore tend to offer a less volatile return profile (the investments are fixed over several years and not publicly traded on open exchanges) as well as protection from duration risk (due to the floating rate nature of the loans).

ESG Enhancements

In addition, we believe systematic review of environmental, social and governance (ESG) factors can enhance the due diligence and ongoing monitoring of private debt details.

Factors such as employee engagement or compliance with relevant environmental regulations, may ultimately impact the financial resilience of a company.

We believe taking a more holistic view on so-called non-financial issues also helps investment managers to protect their reputation and those of their clients.

Opportunities in an Underserved Segment

There are over 100,000 companies in the middle market (€25-250m EBITDA) Europe-wide, which offers a sizeable and diverse opportunity set for investors.4

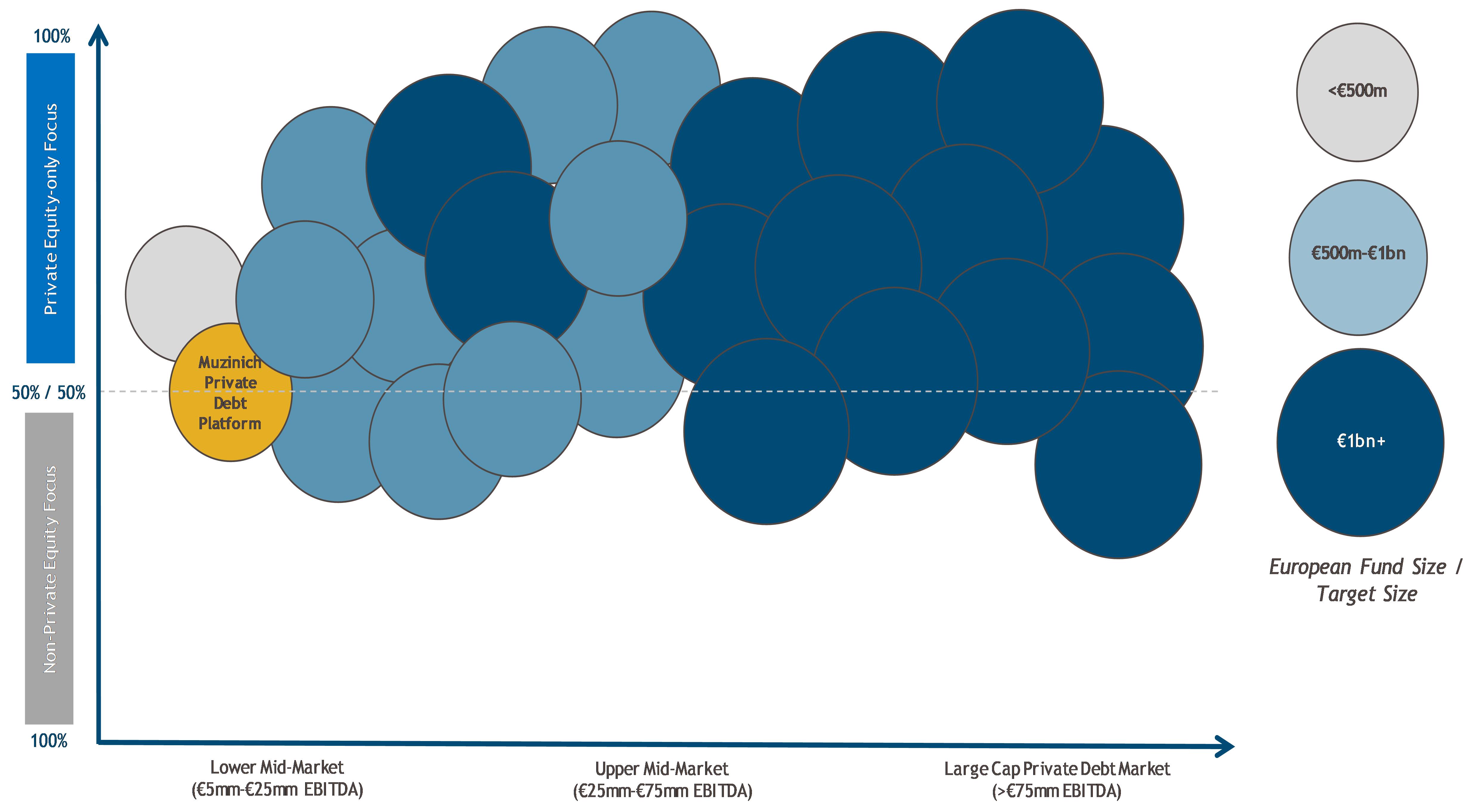

A large proportion of direct lenders tend to be focused on the middle and upper segments of this market (companies with €25->€75m EBTIDA) (Fig. 1).

However, with greater competition comes the potential for increased pressures on pricing, deal sourcing and capital deployment.

Fig. 1 - The Lower Middle Market is Underserved

Note: Muzinich’s opinion of a representative competitive landscape. Analysis based on Muzinich review of publicly available information and institutional insight. Investment strategies of the above referenced firms may change. For illustrative purposes only. As of September 19th, 2019. Investment strategies of firms included in the above analysis may change.

Note: Muzinich’s opinion of a representative competitive landscape. Analysis based on Muzinich review of publicly available information and institutional insight. Investment strategies of the above referenced firms may change. For illustrative purposes only. As of September 19th, 2019. Investment strategies of firms included in the above analysis may change.

In our view, the European lower middle market (companies with €5-25m EBITDA) is underserved from a lending perspective.

Small and medium sized enterprises (SMEs), which broadly comprise this segment, are the growth engine of Europe.5

We believe these companies offer an array of lending opportunities, specifically within family and founder-owned businesses looking for funding solutions.

Significant growth in the European private debt market over the last 10 years has created some concerns that lenders have built large supplies of so-called ‘dry powder’ (capital raised but not deployed).6

However, as Fig. 2 shows, lenders are not experiencing challenges in finding investment opportunities.

Fig. 2 - Capital Continues to be Deployed

Source: Annual Europe-Focused Direct Lending Fundraising and Deployment. Deloitte Alternative Lender Deal Tracker, Autumn 2019. Europe Direct Lending fundraising by quarter. H1 YTD 2019. Muzinich views and opinions for illustrative purposes only, not to be construed as investment advice. https://www2.deloitte.com/content/dam/Deloitte/lu/Documents/private-equity/lu-deloitte-alternative-lender-tracker-autumn-2019.pdf

Source: Annual Europe-Focused Direct Lending Fundraising and Deployment. Deloitte Alternative Lender Deal Tracker, Autumn 2019. Europe Direct Lending fundraising by quarter. H1 YTD 2019. Muzinich views and opinions for illustrative purposes only, not to be construed as investment advice. https://www2.deloitte.com/content/dam/Deloitte/lu/Documents/private-equity/lu-deloitte-alternative-lender-tracker-autumn-2019.pdf

A Local, Flexible Approach

The size of the market and number of jurisdictions does present challenges. We believe accessing this area benefits from specialist local knowledge, and an on-the-ground presence in each of these markets is therefore key for deal sourcing.

In our view, it is important to have a robust investment approach with a deep focus on fundamental analysis, including ESG issues, to identify solid businesses with which a lender can partner and advise on their growth journey.

As each business has different requirements, we believe the flexibility to customise a lending solution specifically for each company is also integral for a successful strategy.

In our experience, as companies look to grow and mature, they typically become more receptive to guidance on both financial and ESG aspects of their business.

While private equity firms provide sponsorship on deals, there are also opportunities for sponsor-less transactions where lenders can work directly with borrowers – again made easier by a local presence, in our view.

Banks are often the first port of call for a company looking for additional funding. However, for smaller businesses who are keen to move quickly, working with a bank can prove a lengthy and restrictive process.

Direct lenders can customise lending solutions to fit the specific needs of each borrower over a shorter time frame; execution may be a short as one month.

We believe ongoing monitoring is also easier for direct lenders who can develop strong relationships through direct dialogue with senior management.

On some occasions it may be appropriate to integrate ESG considerations, such as disclosures on regulatory compliance or governance, into the terms of the loan agreement.

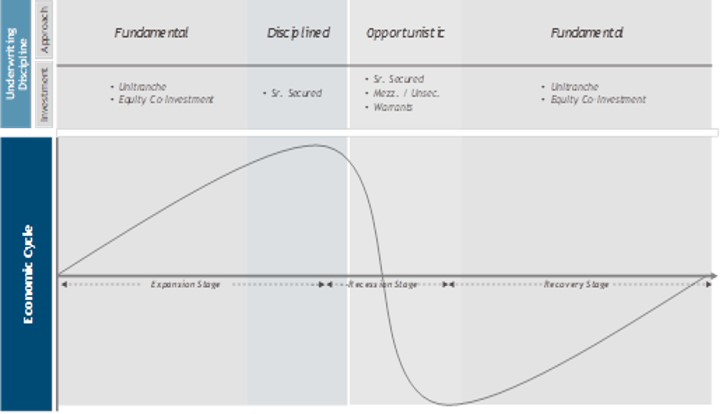

Fig. 3 - Opportunities Across the Cycle

Source: Muzinich & Co. For illustrative purposes only.

Source: Muzinich & Co. For illustrative purposes only.

In our view, the current credit cycle might be nearing its conclusion, having been only marginally extended by looser monetary policy. This is likely to influence investors’ short and medium-term allocation decisions.

Private debt incorporates a range of instruments (from senior to mezzanine through to distressed), making it what we believe is an ‘all weather’ asset class.

Senior debt can offer greater security for late cycle investing. These debt instruments are higher up the capital structure and money will be recovered before subordinated lenders and equity. Senior debt also tends to have stronger documentation and covenants to protect investors in the event of default.

However, as the cycle turns, there tend to be a greater number of distressed opportunities as businesses default; in these instances, lenders can find opportunities to work closely with borrowers and help turn those companies around.

Given where we are in the credit cycle, we believe it makes sense to look for direct lending opportunities in the senior secured segment of the market.

However, as the credit cycle continues to age, lenders could find more attractive opportunities in the subordinated parts of the capital structure.

For fixed income investors, private debt may provide an interesting alternative investment to public market debt by providing yield, but in what we believe is a less risky instrument than private equity for example.

We believe it offers the opportunity for the diversification benefits of higher yields and lower volatility than public debt, as well as the chance to contribute towards economic growth.

While the European private debt market originated from the financial crisis, it has continued to develop due to the demand for alternative risk assets. We believe private debt is an all-weather asset class that is here to stay.

1. https://www.bis.org/bcbs/publ/d424_hlsummary.pdf

2. Preqin, Markets in Focus: Alternative Assets in Europe. As of September 30, 2019. Most recent data available used

3. https://www.federalreserve.gov/monetarypolicy.htm; https://www.ecb.europa.eu/mopo/decisions/html/index.en.html; Barclays Global Aggregate Negative Yielding Debt Market Value (BNYDMVU Index) total of US$13trn, as of January 31, 2019.

4. Amadeus BVD September 14, 2018. Criteria: Excluding UK, last available year, Operating Revenue min = €25m, max = €250m

5. https://ec.europa.eu/growth/smes_en

6. https://www.preqin.com/insights/blogs/alternatives-in-2019-private-capital-dry-powder-reaches-2tn/25289 , as of 28 January 2019

Please click here to download the PDF

Important Information

Muzinich & Co" and/or "Muzinich" referenced herein is defined as Muzinich & Co., Inc. and it’s affiliates. This document and the analysis herein has been produced for information purposes only and are not intended to constitute an offering, advice or recommendation to purchase any securities or other financial instruments. The investment strategies and themes discussed herein may not be suitable for investors depending on their specific investment objectives and financial situation. Investors should conduct their own analysis and consult with their own legal, accounting, tax and other advisers in order to independently assess the merits of an investment.

Statements throughout this document are views and opinions of the author and/or Muzinich. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only, are as of the date of publication and are subject to change without reference or notification. Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,”, “likely,” “will,” “should,” “could,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or the actual performance of the securities, investments or strategies discussed may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained in this document may be relied upon as a guarantee, promise, assurance or a representation as to the future.

All information contained herein is only as current as of the date indicated, and may be superseded by subsequent market events or for other reasons. Nothing contained herein is intended to constitute investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. Historic market trends and performance are not reliable indicators of actual future market behavior or performance.

Certain information contained herein is based on data obtained from third parties and, although believed to be reliable, has not been independently verified by anyone at or affiliated with Muzinich & Co.; its accuracy or completeness cannot be guaranteed.

Past performance is not an indication of future performance. The value of an investment, and income generated (if any) may fall as well as rise and is not guaranteed. Investors may not get back the full amount invested and may lose the entire amount invested. You cannot invest directly in an index, which also does not take into account trading commissions or costs. The volatility of indices may be materially different from the volatility or performance of an account or fund.

Alternative investments can be speculative and are not suitable for all investors. Investing in alternative investments is only intended for experienced and sophisticated investors who are willing and able to bear the high economic risks associated with such an investment. Investors should carefully review and consider potential risks before investing.

No part of this material may be reproduced in any form or referred to in any other publication without express written permission from Muzinich & Co.

Issued by Muzinich & Co. Ltd., which is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ. Muzinich & Co. Ltd. is a subsidiary of Muzinich & Co., Inc. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.