Insight | July 28, 2020

Syndicated Loans in a Recessionary Environment - July 2020

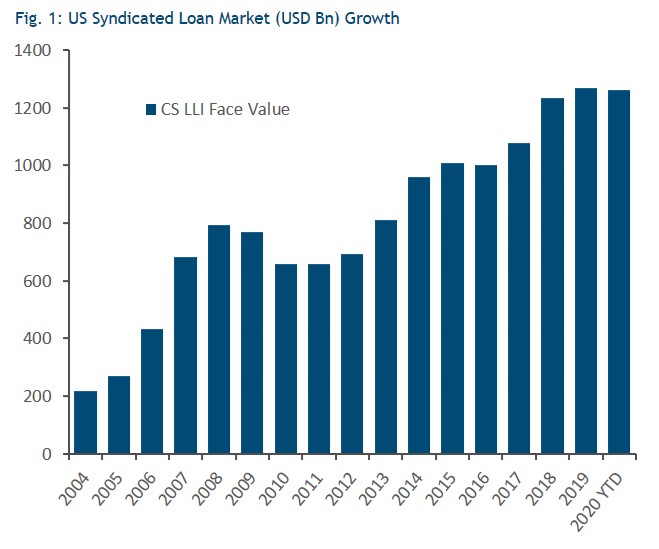

Syndicated Loans in a Recessionary EnvironmentThe US syndicated loan market has grown significantly since the global financial crisis (GFC) and now stands at $1.26 trillion¹, as can be seen in Fig. 1. As we now navigate the first recessionary environment after this period of significant growth, what can we expect of the syndicated loan market, and where do syndicated loans fit in an investor’s portfolio? This note attempts to answer some recent loan questions, starting with the underlying fundamentals.

Source: Credit Suisse Leveraged Loan Index as of June 30th, 2020. For illustrative purposes only, please see index descriptions at the end. You cannot invest in an index.

What Will the Effect of Diminished Lender Protections Be on Default Rates and their Severity?

The Issue

One of the most widespread criticisms of syndicated loans in recent years has been that covenant protections have been eroded through the growth of covenant-lite (or “cov-lite”) loans. The cov-lite concept refers specifically to the removal of a requirement for borrowers to test and sign off their business’s performance quarterly against a series of credit metrics. In the event of a business breaching one of these covenants, lenders could call a default and force the borrower to renegotiate the loan. Various critics have seized upon cov-lite as a symptom of deterioration of underwriting standards in syndicated loans, as documentation became more borrower friendly through the cycle.

Our Opinion

We believe that the reality of whether cov-lite loans will lead to steeper losses for investors is not so clear cut. Maintenance covenants are just one aspect of a loan document (which places many different restrictions on borrowers), and they are still part of current loan structures, if not directly attached to institutional term loans. Maintenance covenants still exist at the revolving credit facilities which sit alongside term loans, and which borrowers have been quick to draw down on during the COVID-19 crisis (usually applying after the drawing down of 35% of a facility). Therefore, in our view, borrowers have effectively opted themselves into maintenance covenant lender protections. While banks rather than institutional term loan lenders control the processes which might be triggered from a breach of one of these covenants, they can help provide downside protection for all creditors in times of stress.

The absence of continually tested maintenance covenants can free management teams to focus on running their business, rather than worrying about time consuming negotiations with lenders. Investors should similarly be focused on management’s ability to navigate a downturn. Credit analysts can follow the trajectory of a business’s credit metrics independently, and portfolio managers can react using the secondary market if there are significant concerns. Much of the value destruction in secondary market pricing occurs long before default, as investors spot looming issues and sell.

We believe that it is likely that those loans which do default will now probably do so because of a missed payment, rather than a breach of covenants. As a result, we could see greater losses on a smaller overall number of defaults in this cycle. Other widespread aspects of documentation, which allow borrowers flexibility with unrestricted subsidiaries, or allow further debt to be raised within existing structures, are also likely to play a part in this cycle’s default landscape as equity investors seek to retain value.

Thorough analysis of documentation has always been an important part of loan investing and will remain so, now more than ever.

The position of senior secured loans at the top of the capital structure (first in line for repayment), will still be important. We believe short term recovery rates are likely to maintain or improve on the current 50% area recently measured by JP Morgan2, and continue to exceed the recovery rates of high yield bonds. Over the longer term, we believe recovery rates are likely to be even higher.

Some commentators have recently pointed out that syndicated loans without junior high yield bonds in their capital structure have tended to have lower recovery rates than those with bonds in the structure, and the numbers (at least when measured 30 days post default) seem to support this. But this does not make loan-only structures un-investable in our opinion. Rather it argues for careful analysis of the risks and rewards with each transaction.

Do Falling Libor Rates Make Syndicated Loans Unattractive in a Low Rate Environment?

The Issue

Loans are a floating rate product and as such, inherently susceptible to the rise and fall of Libor. Loans are therefore an unattractive investment in a low rate environment, where rates could go lower still, and even negative.

Our Opinion

This is true to a point, but in our view that point has long passed. What this statement ignores is that syndicated loans also typically include a feature called a Libor floor, which prevents Libor rates from going below a certain level. Libor floors became commonplace during the financial crisis as base rates dropped to zero or went negative in many economies. Today there are almost no syndicated loans without a Libor floor. 37% of the market carries a Libor floor which is greater than 0%, and 86% of this greater than zero segment carries a Libor floor of 1%¹. This means that the market’s effective Libor floor is approximately 35 basis points, which is higher than where 3-month Libor sits as of June 30th, 2020. This further signifies that the syndicated loan market cannot experience more downside in base rate from this 35 basis points level. Indeed, the presence of this Libor floor could make syndicated loan yields more attractive on a relative basis.

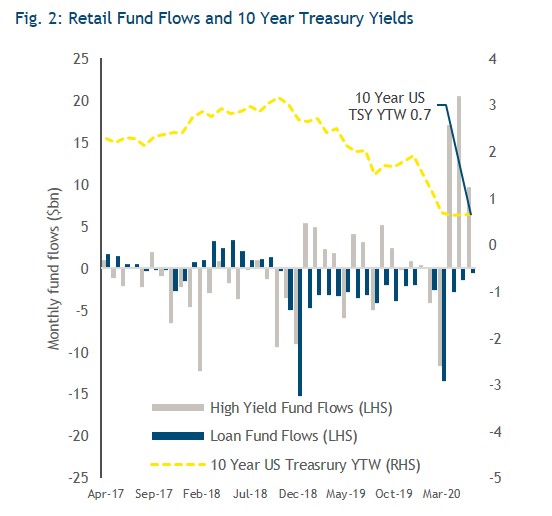

The effect of falling Libor on syndicated loan investor flows has been ongoing for some time. Fig. 2 shows the correlation between retail flows in syndicated loans and ten-year US Treasury yields, with high yield flows included to show how investors have recently preferred the fixed rate asset class. But with Libor where it is now, and retail participation in the loan market reduced to 5%3, this dynamic should have played out. From here we could see retail flows into syndicated loans increase again, as more sophisticated investors take note of the Libor floor dynamic and note the broader sub-investment grade relative value position. With an average index price still just above 901, we believe there is significant upside potential for investors to capture.

Source: J.P. Morgan High Yield Bond and Leveraged Loan Market Monitor as of July 2nd, 2020. ICE BofA ML Current 10-Year US Treasury Index (GA10). For illustrative purposes only.

Source: J.P. Morgan High Yield Bond and Leveraged Loan Market Monitor as of July 2nd, 2020. ICE BofA ML Current 10-Year US Treasury Index (GA10). For illustrative purposes only.

It may also be worth noting that falling interest rates have a simultaneous positive impact on loan fundamentals. While investors may receive less income in the form of a coupon, borrowers have a reduced debt service burden, so debt affordability can improve at a time when it is likely needed the most.

Do Collaterised Loan Obligations (CLOs) Pose a Threat to the Loan Market and the Broader Financial System?

The Issue

Today the CLO market stands at $702 billion and holds 56% of the outstanding institutional syndicated loan market2. Market participants have worried that a) these structures are cousins of the CDOs which caused severe damage during the 2008 crisis and could cause another systemic shock, and b) that CLOs might be overwhelmed by CCC assets which could make them forced sellers of loans. The worries are somewhat separate, but the answers to the criticisms are linked.

Our Opinion

CLOs did not incur losses in the same way as CDOs during the 2008 crisis. A recent Wells Fargo report4 cites Moody’s data showing that no US CLO AAA tranche has ever lost principal, while according to the same report S&P has found a default rate between 1996 and 2018 of 0.2% for single-A tranches and 0.5% for BBB tranches. These investment grade tranches, which make up approximately 85% of the CLO market and have had almost non-existent default rates are those typically held by investors who might be considered systemically important. Submissions to the Federal Reserve as of the end of Q1 2020 show that US banks’ CLO exposure currently stands at $99 billion. This compares with $523 billion of writedowns and losses on AAA CDO investments held by banks before the end of 2008 according to Bloomberg.

Today’s CLOs have evolved by incorporating the lessons of the last crisis into today’s structures. Regulators have looked closely at the CLO market in recent years but have relaxed rather than increased regulation, for example the removal of the requirement for risk retention in US CLOs and the yet more recent relaxation of the Volcker Rule allowing bonds in CLOs. Yes, there will likely be downgrades of CLO tranches in a recession, and this could have an impact on regulatory capital for some investors. It is also true that the lower rated parts of the structure could suffer more significant losses in a downturn than those higher rated at the top of the structure, or at least a temporary diversion of cashflow. However, these riskier parts tend to be held mainly by hedge funds or investors with greater tolerance for potential losses.

As to whether CLOs will be forced sellers of loans, recent months have seen significant downgrades of syndicated loans’ credit ratings. 39% of the market has been downgraded in some way in 2020 according to JP Morgan². The typical 7.5% CCC buckets built into CLOs have indeed been exceeded in many cases. But the idea that this makes CLOs forced sellers of loans is incorrect in our view. Instead the excess CCCs cannot be counted towards the tests which govern the overall structure. When these tests are breached, the structure does not unwind. Rather, cashflows are diverted away from the lower rated tranches to repay the top of the capital structure, starting with the AAA investors.

In reality, CLO managers are incentivized to minimize the amount of CCCs in the structure, to protect their own fees and a CLO’s equity investors, so CCCs become an unloved part of the loan market in these times. However, we believe this creates opportunities for unconstrained investors who can buy these technically oversold assets. Price dispersion and recompression can create equity-like return propositions for loans which can recover in price and remain a top of the corporate capital structure investment.

Where Should Syndicated Loans Sit in Investors’ Portfolios?

Syndicated loans typically compete for shelf space with high yield in investors’ portfolios. While both products are sub-investment grade lending at heart, there are some significant differences between the products. In contrast to high yield bonds, syndicated loans are a floating rate product, callable at any time, and typically exhibit lower volatility due to the almost exclusively institutional nature of the investor base.

Syndicated loans sit higher in the corporate capital structure than high yield bonds, providing different risk considerations. 97% of the syndicated loan market is 1st lien senior secured, compared to 18% of the comparable high yield index5. While both asset classes will suffer defaults in a recession, loan recovery rates should be higher than high yield given their senior secured position in borrowers’ capital structures.

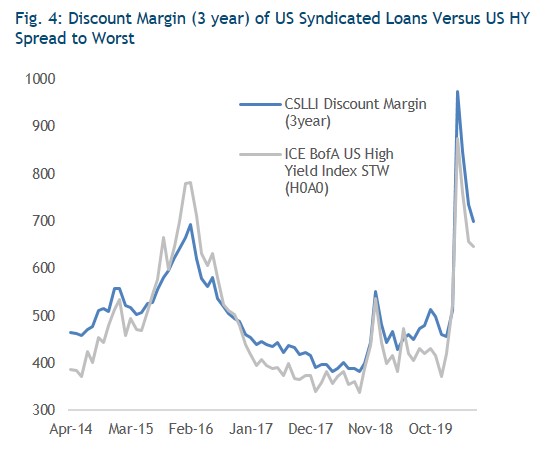

Syndicated loans can provide compelling relative value when compared to high yield. Fig. 3 and 4 show syndicated loan prices and spread equivalents versus the same metrics for high yield. Syndicated loans have a lower average price and a higher spread. In recent times this anomaly can be explained by a) the effect of falling Libor on retail investors’ loan allocations, and b) the recent actions of the Fed underpinning high yield demand, but in our view this gap should at the very least narrow over time.

Source: Bloomberg and Credit Suisse as of June 30th, 2020. ICE BofA US High Yield Index Average Price (H0A0). For illustrative purposes only, please see index descriptions at the end. You cannot invest in an index.

Source: Bloomberg and Credit Suisse as of June 30th, 2020. ICE BofA US High Yield Index Average Price (H0A0). For illustrative purposes only, please see index descriptions at the end. You cannot invest in an index.

Source: Bloomberg and Credit Suisse as of June 30th, 2020. ICE BofA US High Yield Index Average Price (H0A0). For illustrative purposes only, please see index descriptions at the end. You cannot invest in an index.

Source: Bloomberg and Credit Suisse as of June 30th, 2020. ICE BofA US High Yield Index Average Price (H0A0). For illustrative purposes only, please see index descriptions at the end. You cannot invest in an index.

Finally, syndicated loans can offer some additional sectoral diversity. Of particular relevance recently has been the fact that the syndicated loan market had an energy sector exposure of 3% at the end of February 2020, versus 12% for high yield.5

Conclusion

In our view, the loan market today is possibly nearing the trough of an economic cycle and should be well positioned for the recovery, both fundamentally and technically. We believe this should create opportunities for investors who can look beyond the headlines. Rates will rise again and retail investors will most likely return to the market in anticipation of this. CLOs, which paused their issuance at the market wides, are being created again, and in the short term demand for loans is likely to outstrip thin supply.

The convergence of global interest rates around zero once again also removes one of the major obstacles for international investors looking at US syndicated loans as hedging costs for buying USD assets have come down substantially. We can expect to see more international flows into the US syndicated loan market in the coming months to take advantage of the enhanced return opportunity.

We believe loans represent an appealing investment opportunity as a lower volatility source of carry for investors, coupled with some upside potential through the pull to par opportunity in the current market.

1. Credit Suisse Leveraged Loan Index (CSLL) as of June 30th, 2020.

2. J.P. Morgan High-Yield and Leveraged Loan Morning Intelligence, June 30th, 2020.

3. J.P. Morgan Fund Flows as of June 16th, 2020.

4. Wells Fargo Structured Products Research, “CLO Lagniappe: Do CLOs Post Systemic Risk?” June 11th, 2020.

5. Credit Suisse Leveraged Loan Index (CSLL) and the ICE BofA ML US High Yield Index (H0A0) as of June 30th, 2020.

----------------------------------------------------------------------------------------------------------------------------------

Important Information

"Muzinich & Co.", “Muzinich” and/or the "Firm" referenced herein is defined as Muzinich & Co., Inc. and its affiliates. This document is for informational purposes only and does not constitute an offer or solicitation of an offer, or any advice or recommendation, to purchase or sell any securities or other financial instruments and may not be construed as such. Past performance is not indicative of future results. The value of an investment, and income generated (if any) may fall as well as rise and is not guaranteed. All information contained herein is believed to be accurate as of the date(s) indicated, is not complete, and is subject to change at any time. Muzinich hereby disclaims any duty to provide any updates or changes to the analysis contained herein. Certain information contained herein is based on data obtained from third parties and, although believed to be reliable, has not been independently verified by anyone at or affiliated with Muzinich; its accuracy or completeness cannot be guaranteed. This document may contain forward-looking statements, which give current expectations of the market’s future activities and future performance. Further, no person undertakes any duty or obligation to revise such forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events. Any forward looking information or statements expressed in the above may prove to be incorrect. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Opinions and statements of financial market trends that are based on market conditions constitute our judgement and are subject to change without notice. Historic market trends are not reliable indicators of actual future market behavior. The information herein is not intended to provide a sufficient basis on which to make an investment decision and should not be construed as investment advice or an offer or solicitation of an offer. Investors should confer with their independent financial, legal or tax advisors. The above is neither independent investment research, nor is it an objective or independent explanation of the matters contained herein, and you must not treat it as such. No part of this material may be reproduced in any form or referred to in any other publication without express written permission from Muzinich. In Europe, this material is issued by Muzinich & Co. Limited, which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ.

Index descriptions:

CS Leveraged Loan Index – The CS Leveraged Loan Index is designed to mirror the investable universe of US dollar denominated leveraged loan market. The index is rebalanced monthly on the last business day of the month instead of daily.

H0A0 – The ICE BofA ML US High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt publicly issued in the US domestic market.

You cannot invest directly in an index, which also does not take into account trading commissions or costs. The volatility of indices may be materially different from the volatility performance of an account or fund.